Comparative Analysis of Monthly Reports on the Oil Market

1. International Policy and Market Context

IMF sees strongest economic growth in more than 40 years

- The International Monetary Fund lifted its global economic growth forecast for 2021 to 6 percent – the strongest annual growth in more than four decades. IMF's chief economist said, "even with a high uncertainty about the path of the pandemic, a way out of this health and economic crisis is increasingly visible." The rebound comes after a 3.3 percent contraction in 2020.

Suez Canal Blockage Highlights Dredging Industry Vulnerability

- A container ship blocking the Suez Canal did not have a significant impact on oil and gas markets due to swift action. However, dredged shipping channels are critical infrastructure for global energy and wider trade that are more vulnerable now than ever by suspension of public works during the pandemic.

Gulf of Mexico crude oil production will increase with new projects in 2021 and 2022

- EIA forecasts U.S. crude oil production in the US Federal Gulf of Mexico (GOM) to increase in the next two years. By the end of 2022, 13 new projects could account for about 12 percent of total GOM crude oil production, or about 200 kb/d. The GOM accounts for 15–16 percent of US crude oil production.

15th OPEC and non-OPEC Ministerial Meeting agrees to gradual production increase

- OPEC and non-OPEC Ministers agreed to adjust production of world oil supplies from May to July on 1 April 2021. The group will boost production by 350 kb/d in May, add the same volume again in June and increase by 440 kb/d barrels in July. Saudi Arabia will begin rolling back its voluntary 1 mb/d adjustment, adding 250 kb/d in May, 350 kb/d in June, and 400 kb/d in July.

2. Key Points

2.1 Demand

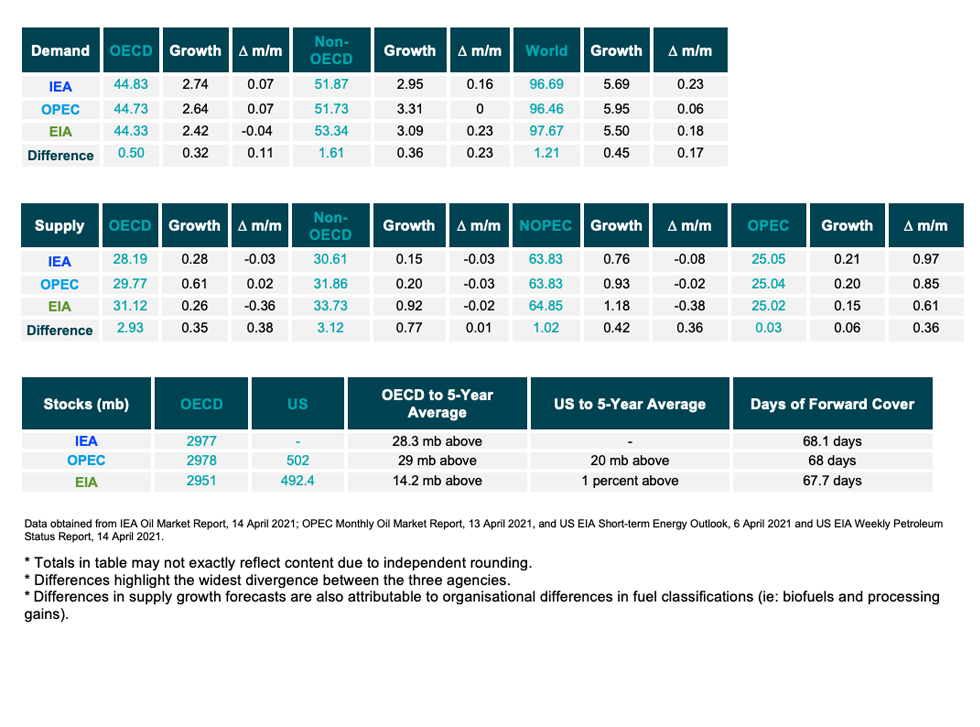

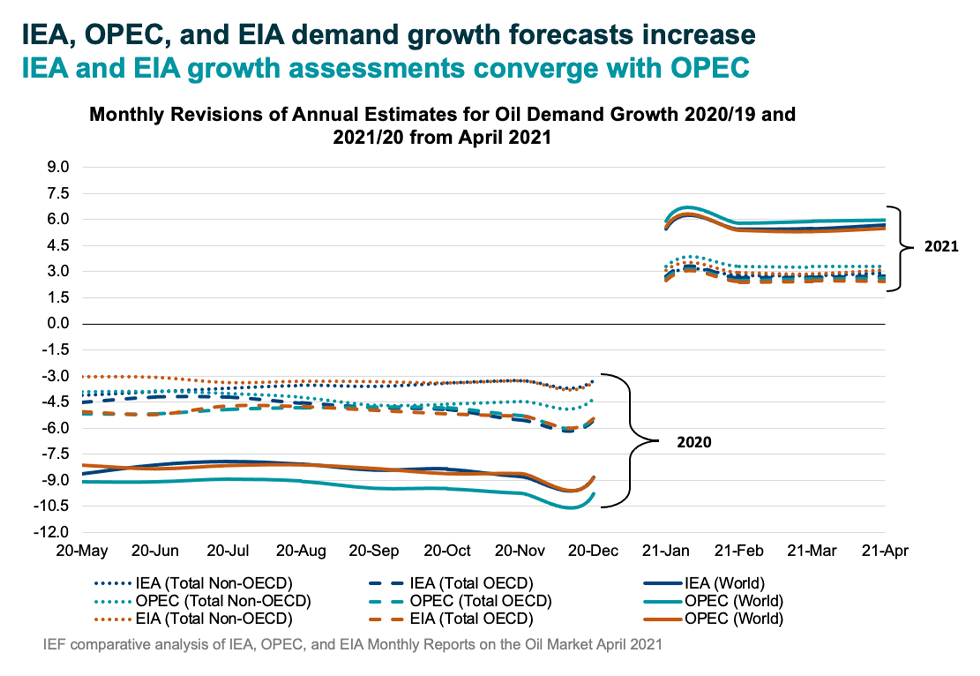

The IEA, OPEC, and EIA demand growth assessments increase.

- The IEA increased its assessment by 230 kb/d for a year-on-year (y-o-y) demand growth of 5.69 mb/d driven by the continued vaccine rollout, demand recovery in the US, and strong consumption in China and Japan.

- OPEC's forecasts a y-o-y demand growth of 5.95 mb/d, an increase of 60 kb/d from last month.

- EIA's assessment increased by 180 kb/d for a demand growth of 5.50 mb/d in 2021. The IEA, OPEC, and EIA estimates for absolute world demand are now 96.69 mb/d, 96.46 mb/d, and 97.67 mb/d for 2021, respectively.

The IEA, OPEC, and EIA align on OECD and non-OECD demand growth.

- The IEA's non-OECD demand assessment increases by 160 kb/d to a demand growth of 2.95 mb/d, while OPEC growth remains at 3.31 mb/d. The EIA's assessment increases by 230 kb/d for non-OECD demand growth of 3.09 mb/d y-o-y.

- The IEA's estimate for OECD demand increased by 70 kb/d for demand growth at 2.74 mb/d for 2021. OPEC's estimate also increased by 70 kb/d for a demand growth at 2.64 mb/d while EIA's assessment sees growth at 2.42 mb/d y-o-y, a decrease of 40 kb/d.

- The IEA and EIA assessments differ by 0.32 mb/d and EIA and OPEC assessments differ by 0.36 mb/d on OECD and non-OECD demand growth, respectively.

2.2 Supply

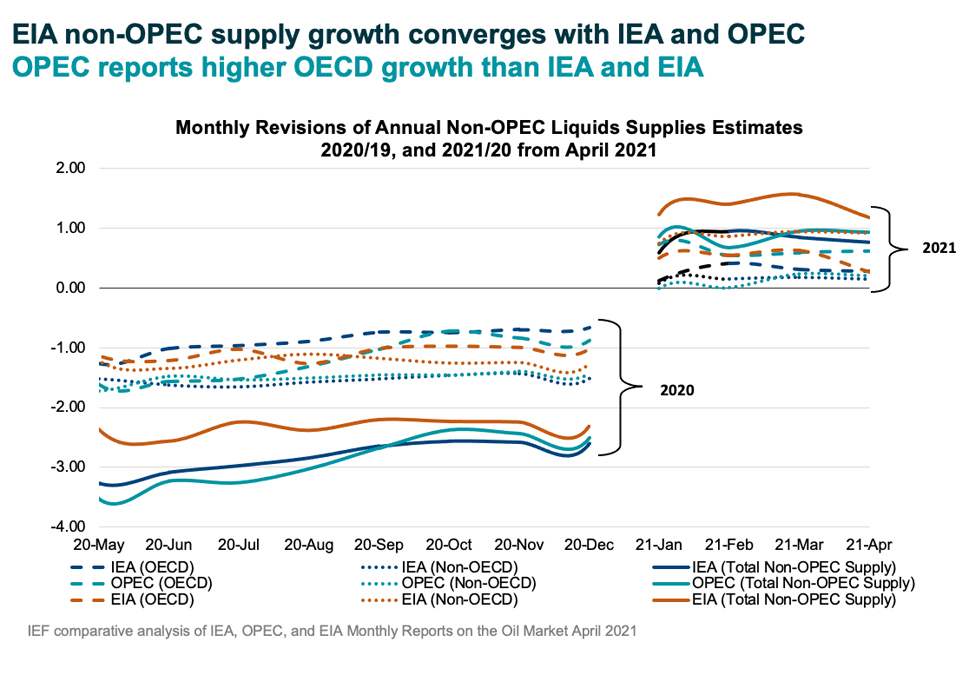

The IEA, OPEC, and EIA non-OPEC supply growth assessments converge.

- The IEA's April assessment for non-OPEC supply decreases by 80 kb/d for a total growth of 0.76 mb/d while OPEC reports total growth of 0.93 mb/d, a decrease of 20 kb/d. The EIA reports a higher overall supply growth of 1.18 mb/d y-o-y, a decrease of 380 kb/d from last month's assessment. In absolute values, the IEA, OPEC, and EIA estimate non-OPEC supply at 63.83 mb/d, 63.83 mb/d, and 64.85 mb/d, respectively for 2021.

- The IEA reports OECD supply growth at 0.28 mb/d while OPEC records OECD growth at 0.61 mb/d, a decrease and increase of 30 kb/d and 20 kb/d, respectively. The EIA also records a growth of 0.26 mb/d, a decrease of 360 kb/d. In absolute values, the IEA and OPEC, and EIA estimate OECD supply at 28.19 mb/d, 29.77 mb/d, and 31.12 mb/d, respectively for 2021. Divergence on OECD supply growth is the largest between OPEC and EIA differing by 350 kb/d.

The EIA reports higher non-OECD supply growth than the IEA and OPEC.

- The IEA's supply assessment reaches total supply growth of 0.15 mb/d, a decrease of 30 kb/d from last month. OPEC's forecast reports a growth of 0.20 mb/d, a decrease of 30 kb/d from last month. The EIA is substantially more optimistic showing non-OECD supply growth of 0.92 mb/d, a decrease of 20 kb/d from last month. In absolute values, the IEA, OPEC, and EIA non-OECD supply estimates are 30.61 mb/d and 31.86 mb/d, and 33.73 mb/d, respectively for 2021. Divergence on total non-OECD supply growth is widest between the IEA and EIA that differ by 770 kb/d.

The IEA, OPEC, and EIA all report decreases in OPEC production in March.

- The IEA revised its OPEC production estimate upward by 970 kb/d month-on-month (m-o-m) in March to reach total production of 25.05 mb/d. OPEC also reported an increase by 850 kb/d m-o-m for total production of 25.04 mb/d in March. The EIA increased its assessment by 610 kb/d for total OPEC crude production of 25.02 mb/d.

2.3 Stocks

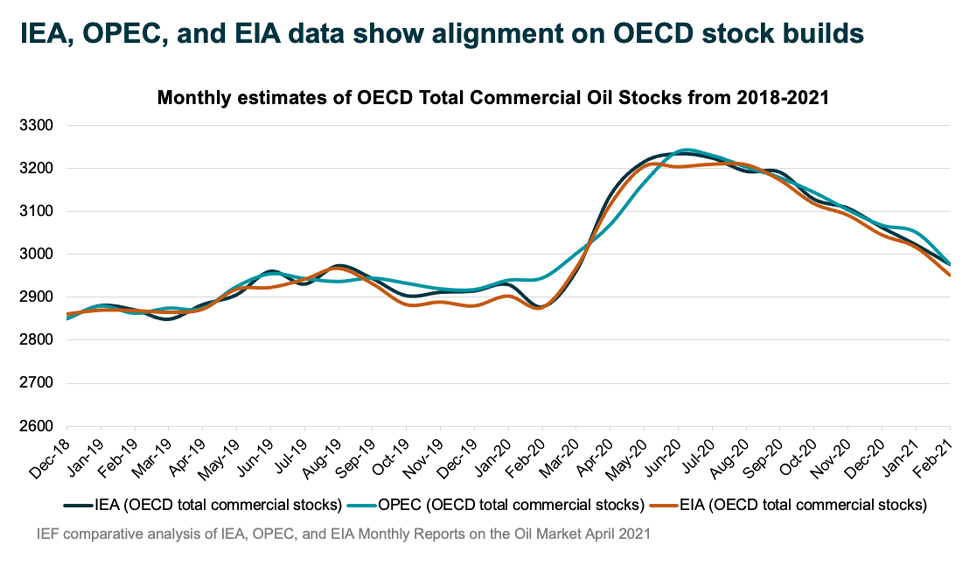

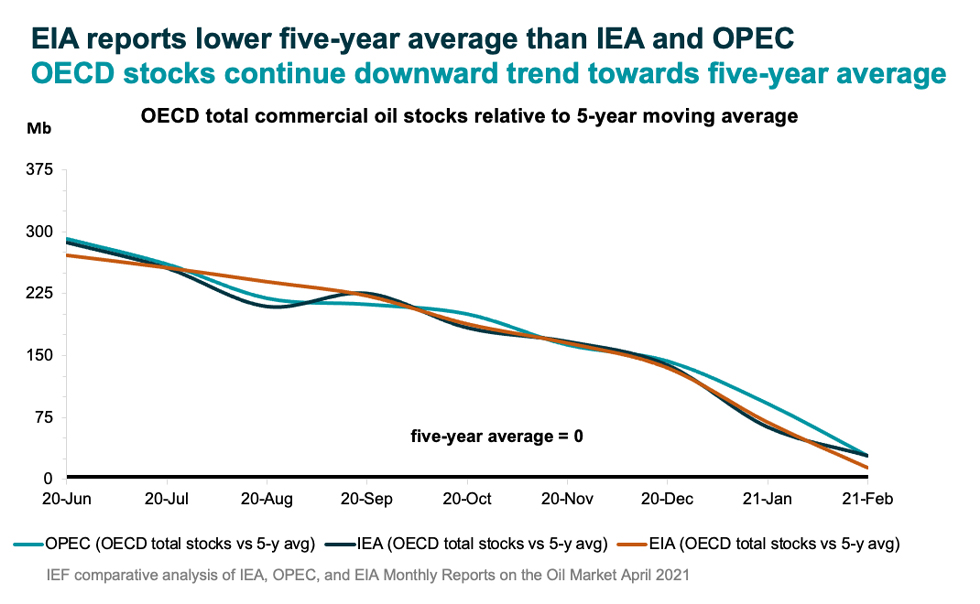

The IEA, OPEC, and EIA continue to report strong alignment on stock figures.

- The IEA reports OECD stock levels at 2977 mb, which is close to OPEC's assessment of 2978 mb and EIA's assessment of 2951 mb, or for OECD stock that is 28.3 mb, 29 mb, and 14.2 mb above the five-year average, respectively.

- According to the IEA, crude oil inventories built by 7.4 mb while product stocks fell by about 67 mb. Other oils, including NGLs and feedstocks built by 3.6 mb. According to OPEC, crude oil stocks built by around 6 mb while products fell by 51 mb.

- EIA estimates OECD inventories dropped by 67 mb in February to 2951 mb – 14.2 mb above the five-year average.

- The widest divergence between OPEC, and the EIA stands at 27 mb. Total US crude inventories (excluding SPR) amount to about 492 mb according to the EIA which are 1 percent above the five-year average for this time of year. OPEC reports US commercial crude oil stocks at about 485 mb and around 15 mb above the five-year average.

2.4 Snapshot (mb/d)

3. Global Analysis

3.1 Demand Data

Figure 1

3.2 Supply Data

Figure 2

3.3 Stock Data

Figure 3

Figure 4

JODI Data:

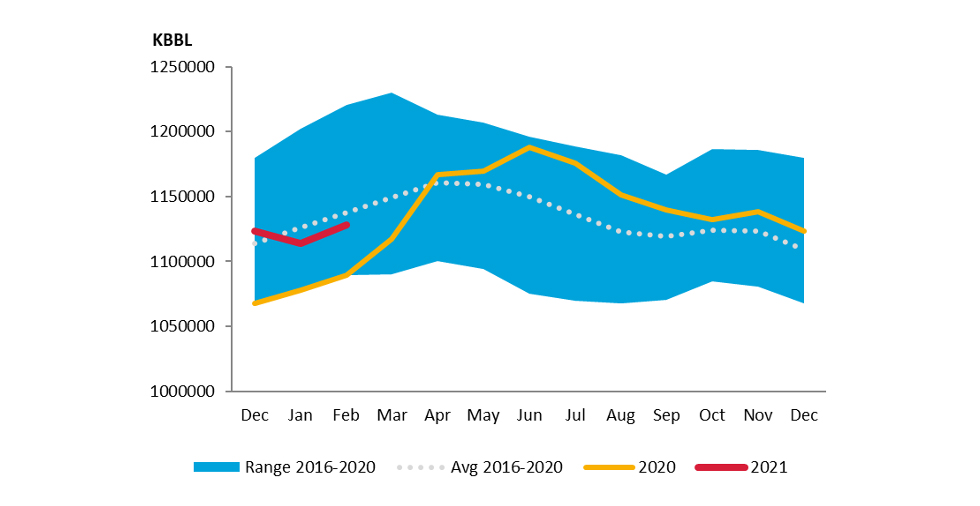

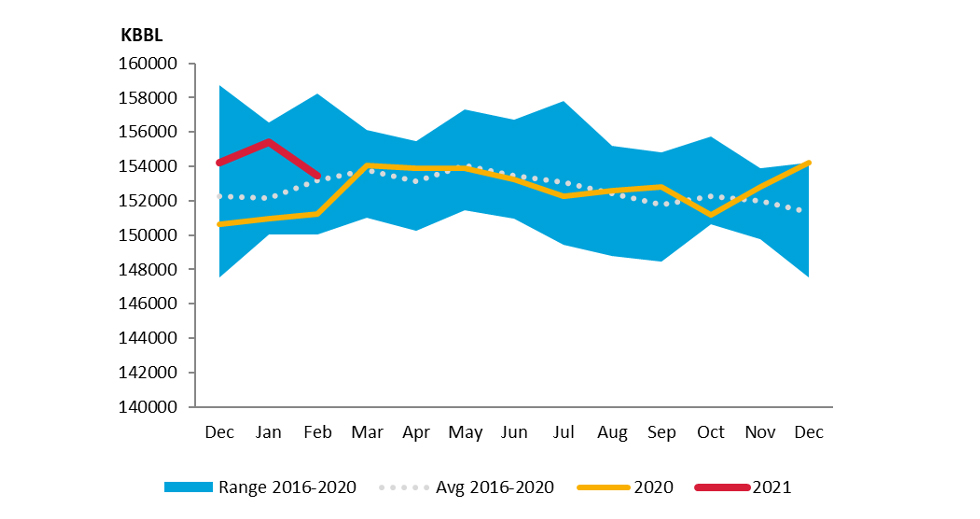

Figure 5 - US Crude Oil Closing Stocks

US crude oil closing stock levels rose by 14.35 mb m-o-m in February to 1128.29 mb.

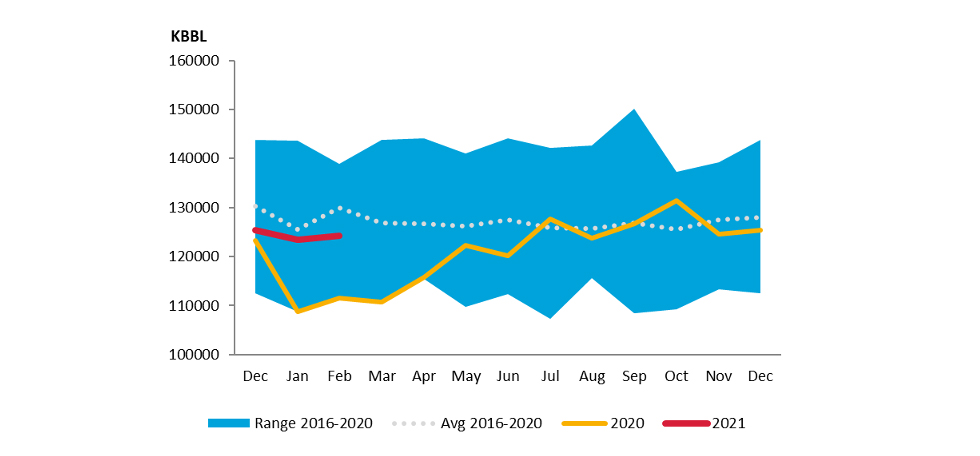

Figure 6 - Korea Crude Oil Closing Stocks

Korean crude oil closing stock levels rose by 744 kb m-o-m in February to 124.18 mb.

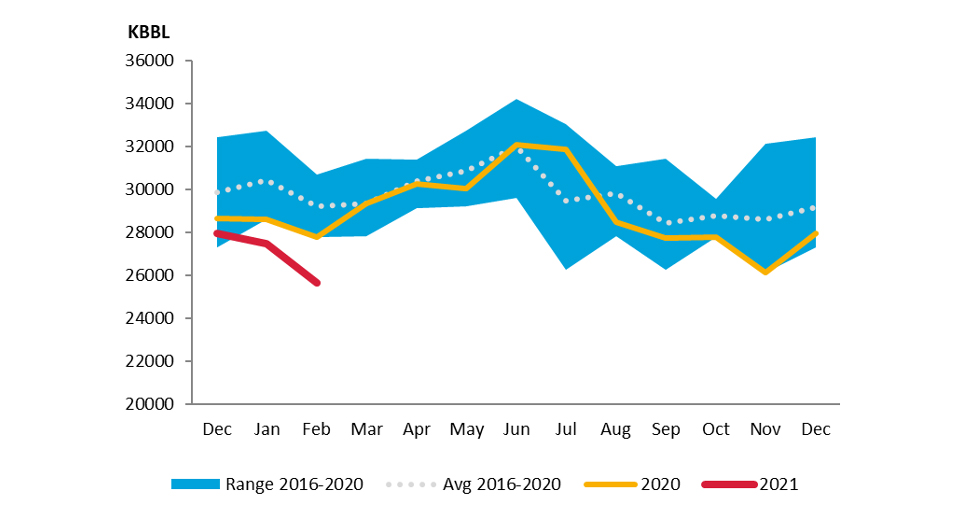

Figure 7 - UK Crude Oil Closing Stocks

UK crude oil closing stock levels in February fell m-o-m again by 1.81 mb to 25.65 mb – the lowest since monitoring began in 2002.

Figure 8 - Germany Crude Oil Closing Stocks

German crude oil closing stock levels in February fell m-o-m by 1.98 kb to 153.44 mb.

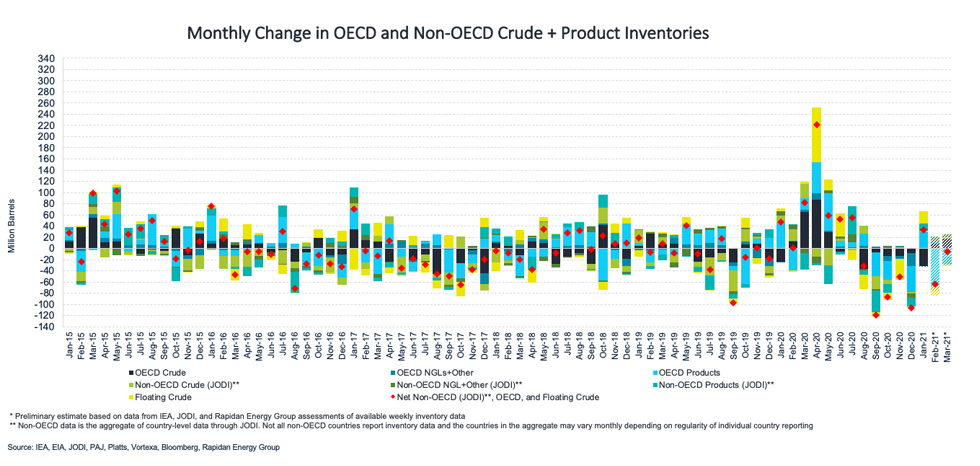

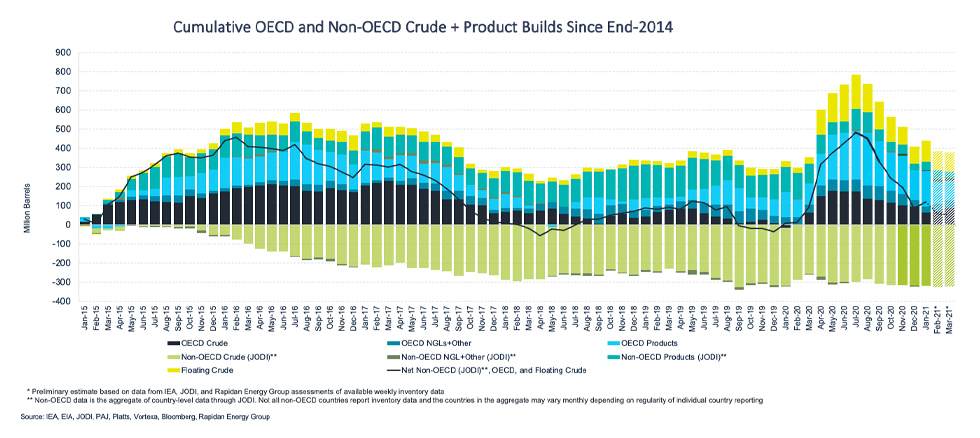

While both the IEA and OPEC report closely aligned data on OECD stocks due to a continuous and reliable data stream and data harmonisation efforts, comprehensive data on stock developments for non-OECD countries is still work in progress as large differences in assessments show.

3.3.1 Global Stock Analysis

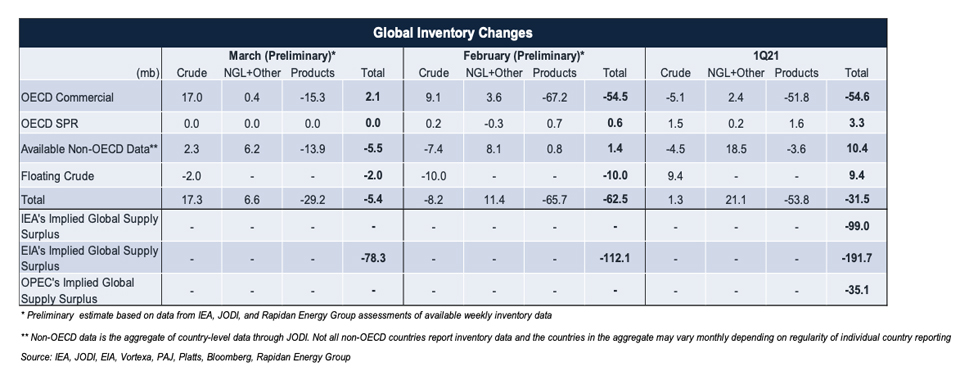

IEA, JODI, and available weekly inventory data for February imply crude, NGL, and product stocks drew by ~62.5 mb

- JODI non-OECD data for February shows inventories increased by 1.4 mb after a 7.4 mb draw in crude was largely offset by an 8.1 mb build in NGL + Other. Crude stocks drew in Brazil (4.2 mb), Saudi Arabia (2.6 mb) and Chinese Taipei (3.4 mb).

- Floating crude inventories fell by 10.0 mb in February and by 2.0 mb in March. They are now 122.2 mb below their June peak.

- Rapidan Energy Group's preliminary global inventory estimate for March shows slight draws with visible inventories falling by 5.4 mb. Early data shows OECD commercial increased by 2.1 after a 17.0 mb build in crude was nearly offset by a 15.3 mb draw in products. If the numbers stand, the slight build for March would break seven consecutive months of OECD total stock draws.

- Stock data shows global inventories drew by ~31.5 mb in 1Q21, led by a 51.8 mb drop in OECD product stocks, but partially offset by a 10.4 mb build in the non-OECD data. Notably, our estimation for the quarter so far (which includes preliminary data for both February and March) came in below the stock levels implied by IEA, EIA, and OPEC's balances.

* Non-OECD data is the aggregate of country-level data through JODI. Not all non-OECD countries report inventory data and the countries in the aggregate may vary monthly depending on regularity of individual country reporting.

Table 1

Figure 9

Figure 10

Explanatory Note

The IEF conducts a comprehensive comparative analysis of the short-, medium-, and long-term energy outlooks of the IEA OPEC, and the EIA to inform the IEA-IEF-OPEC Symposium on Energy Outlooks that the IEF hosts in Riyadh as part of the trilateral work programme on a yearly basis.

To inform IEF stakeholders on how perspectives on the oil market of both organisations evolve over time regularly, this monthly summary provides:

- An overview of key events and initiatives in the international policy and market context.

- Key findings and a snapshot overview of data points gained from comparing basic historical data and short-term forecasts of the IEA Oil Market Report and the OPEC Monthly Oil Market Report.

- A comparative analysis of oil inventory data reported by JODI, the IEA, OPEC, and the US EIA, and secondary sources in collaboration with the Rapidan Energy Group.

The International Energy Forum

The International Energy Forum is the leading global facilitator of dialogue between sovereign energy market participants. It incorporates members of International Energy Agency and the Organization of the Petroleum Exporting Countries, and also key players including China, India, Russia and South Africa. The forum's biennial ministerial meetings are the world's largest gathering of energy ministers, where discussions focus on global energy security and the transition towards a sustainable and inclusive energy future. The forum has a permanent secretariat of international staff based in the Diplomatic Quarter of Riyadh, Saudi Arabia. For more information visit www.ief.org.