")

Comparative Analysis of Monthly Reports on the Oil Market

1. International Policy and Market Context

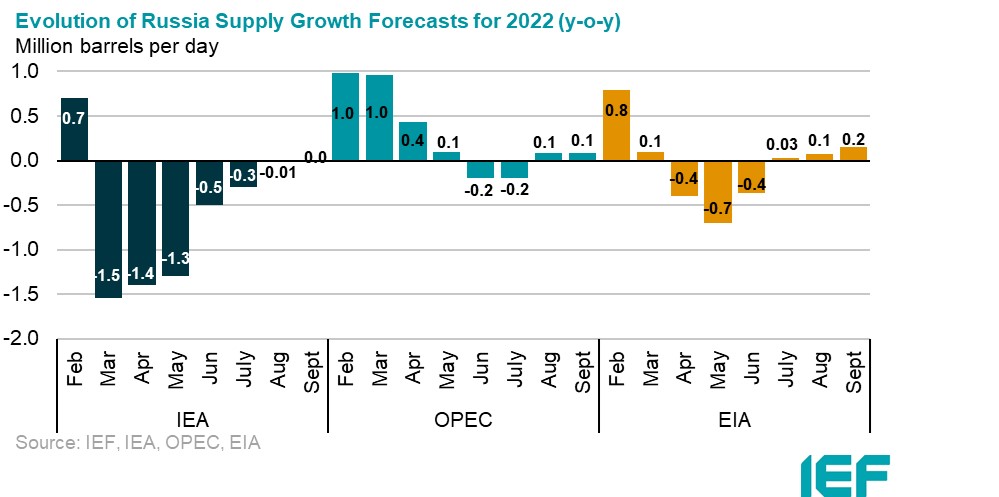

Russia cuts off gas exports via Nord Stream indefinitely

- On 2 September, Gazprom, the Russian state energy company, said it would not resume flows through the Nord Stream pipeline after routine maintenance on 31 August because it had detected an oil leak. Before this, Gazprom restored supply to only a fifth of its capacity after a previous shutoff for maintenance. The Nord Stream 1 pipeline is a key pipeline carrying Russia's vast gas supplies to Europe accounting for about 35 percent of Europe's total Russian gas imports last year. Russian gas shipments to Europe have fallen almost 90 percent from a year ago.

G7 countries agree to cap price of Russian oil

- On 2 September 2022, members of the G7 agreed to impose a price cap on Russian oil. The policy will be based on an incentive system where importers seeking insurance cover and shipping services from companies based in G7 and EU countries to transport Russian oil would need to observe the price ceiling. The aim is to allow Russian shipments to continue if sold below the cap when the EU insurance ban comes into effect in December. The oil cap plans will be implemented at the same time as the EU embargo on Russian oil takes effect. There will be two price caps, one for crude and one for refined products which will go into effect 5 December and 5 February 2023, respectively.

EU ministers endorse emergency measures to curb soaring energy prices

- On 7 September, Ursula von der Leyen, EU Commission President, outlined five steps to mitigate the energy crisis four of which received ministerial support. This includes an EU-wide plan to reduce electricity consumption during peak hours, a price cap on the excess revenues made by renewables and nuclear energy, a solidarity contribution by fossil fuel companies to support vulnerable households, and a state aid program to inject extra liquidity into struggling utility businesses. The fifth proposal, a price cap just on Russian pipeline gas, did not receive enough support to move forward. Instead, most member states are pushing for a wider cap on all gas imports entering the EU, irrespective of their geographical origin.

OPEC+ countries decrease production amid economic slow down

- On 5 September, OPEC and non-OPEC countries agreed to adjust downward by 100 kb/d the monthly overall production for the month of October 2022 due to concerns of an economic slowdown. The meeting noted that the prior upward adjustment of 100 kb/d was intended only for September 2022. While reconfirming the production adjustment plan and the monthly production adjustment mechanism approved at the 19th and 29th OPEC and non-OPEC Ministerial Meetings, OPEC and non-OPEC countries will consider calling a meeting at any time to address market developments if necessary. The 33rd OPEC and non-OPEC Ministerial Meeting is scheduled for 5 October 2022.

Price volatility impedes energy security for non-OECD countries

- High energy prices triggered by the war in Ukraine and the partial European embargo on Russian crude are impacting non-OECD countries. With traditional supply of refined products being diverted to European markets, countries such as Nigeria, Angola, and South Africa are facing gasoline and diesel shortages, rising inflation, and potential of food shortages due to a concurrent rise in fertilizer prices. In South Asia, countries such as Pakistan, Bangladesh, and Sri Lanka continue to be hard hit by natural gas shortages as gas deliveries that were scheduled for South Asia are being redirected to Europe, where buyers can afford higher prices. Governments across Latin America are also responding by ramping up subsidies and cutting taxes on gasoline and diesel to protect consumers.

2. KEY POINTS

2.1 DEMAND

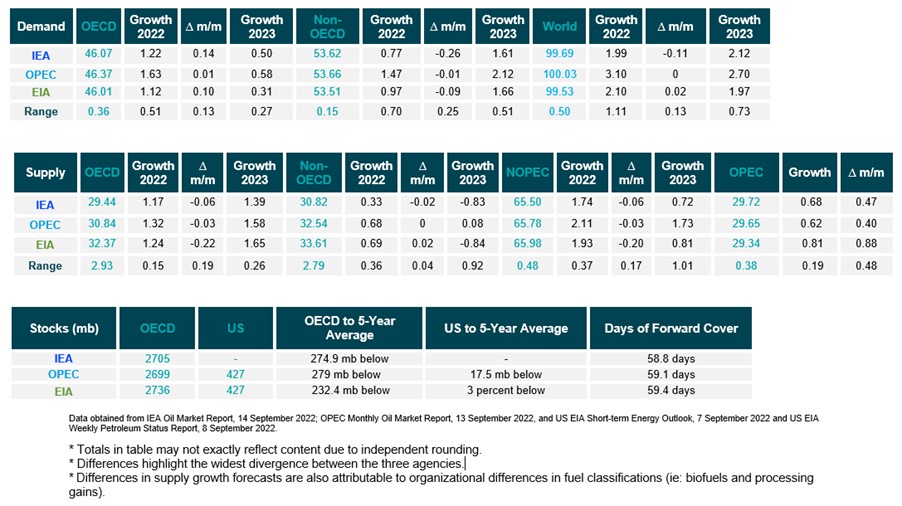

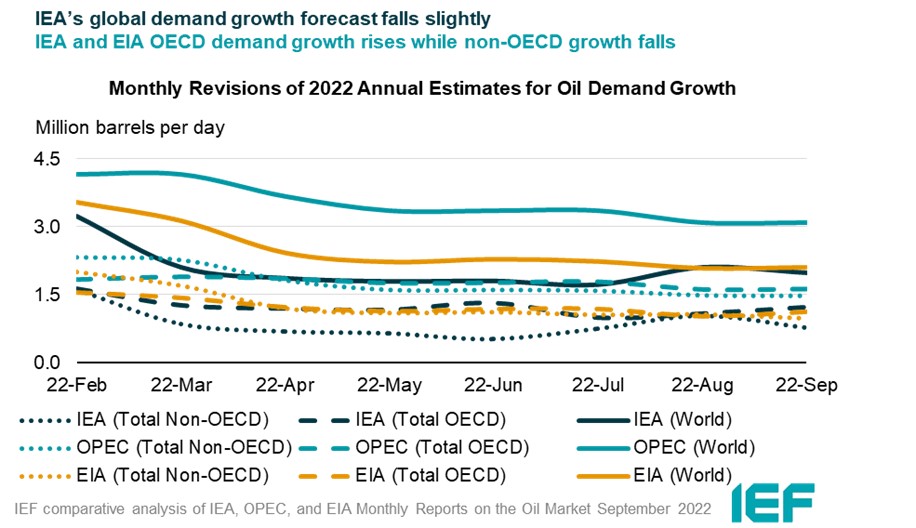

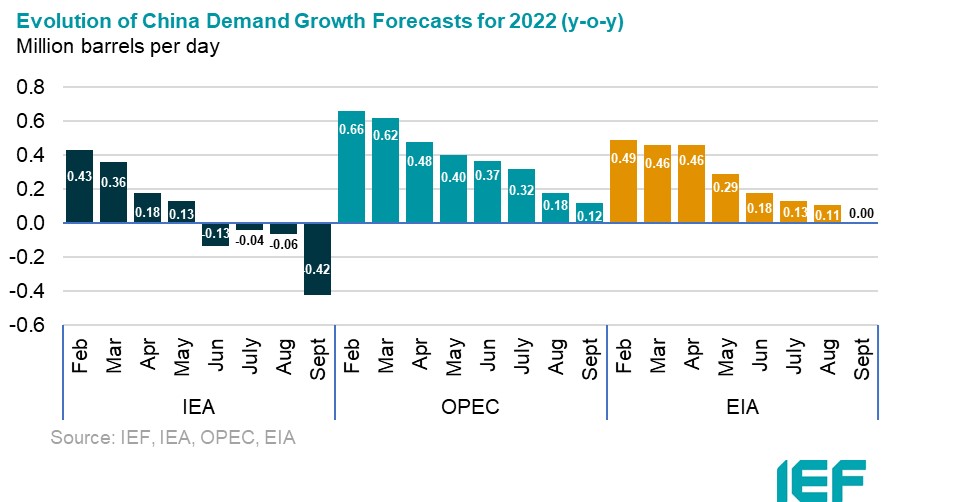

The IEA and EIA expect similar demand growth while OPEC growth remains higher.

- IEA’s demand growth assessment for this year falls by 110 kb/d to 1.99 mb/d year-on-year (y-o-y) due to reduced Chinese demand. Growth rises to 2.12 mb/d in 2023.

- OPEC’s y-o-y forecast remains the same at 3.10 mb/d.

- EIA’s assessment rises by 20 kb/d for a growth of 2.10 mb/d this year. The IEA, OPEC, and EIA estimates for absolute world demand are now 99.69 mb/d, 100.03 mb/d, and 99.53 mb/d for 2022, respectively.

OPEC reports greater OECD and non-OECD demand growth compared to the IEA and EIA.

- The IEA's assessment of y-o-y non-OECD demand growth falls by 260 kb/d to 0.77 mb/d, while OPEC’s estimate falls by 10 kb/d to 1.47 mb/d. EIA non-OECD demand growth falls by 90 kb/d to 0.97 mb/d.

- The IEA's estimate for OECD demand growth rises by 140 kb/d to 1.22 mb/d for 2022 while OPEC’s projection rises by 10 kb/d for a growth of 1.63 mb/d. EIA demand growth also rises by 100 kb/d for a growth of 1.12 mb/d.

- The largest divergence in OECD and non-OECD demand growth estimates are between EIA and OPEC at 0.51 mb/d and between IEA and OPEC at 0.70 mb/d, respectively.

2.2 SUPPLY

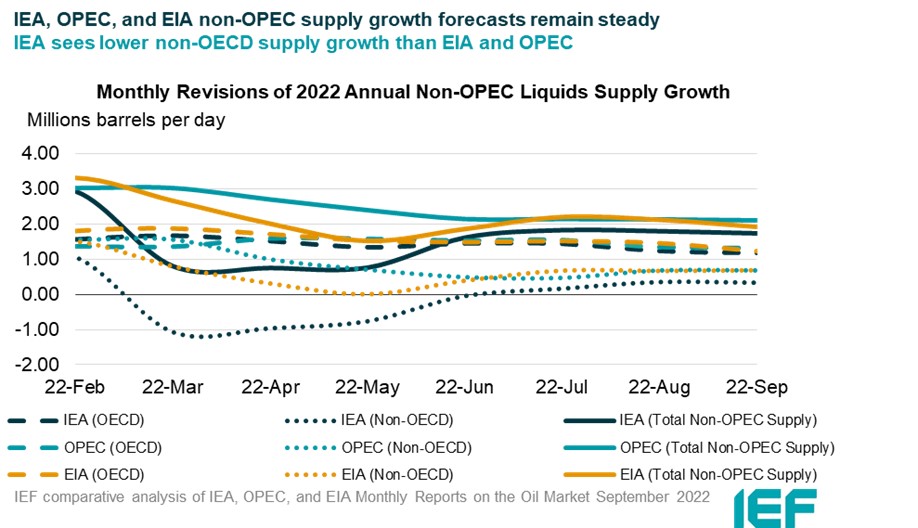

The IEA, OPEC, and the EIA report similar growth in non-OPEC supply.

- The IEA’s September assessment for non-OPEC supply falls by 60 kb/d to reach a growth of 1.74 mb/d while OPEC’s estimate falls by 30 kb/d for a growth of 2.11 mb/d. The EIA’s assessment falls by 200 kb/d for an overall growth of 1.93 mb/d. In absolute values, the IEA, OPEC, and the EIA estimate non-OPEC supply at 65.50 mb/d, 65.78 mb/d, and 65.98 mb/d, respectively for 2022.

- The IEA estimates OECD oil supply growth this year at 1.17 mb/d, OPEC pegs it at 1.32 mb/d, and EIA reports growth at 1.24 mb/d, a decrease of 60 kb/d, 30 kb/d, and 220 kb/d, respectively. In absolute terms, the IEA, OPEC, and the EIA estimate OECD oil supply at 29.44 mb/d, 30.84 mb/d, and 32.37 mb/d, respectively for 2022. The largest divergence of OECD supply growth estimates is between IEA and OPEC at 150 kb/d.

The IEA forecasts substantially less non-OECD supply growth compared to OPEC and EIA in 2022.

- The IEA’s assessment for non-OECD supply falls by 20 kb/d to a total growth of 0.33 mb/d in 2022.

- OPEC’s forecast remains the same at 0.68 mb/d while the EIA revised its non-OECD growth forecast up by 20 kb/d to a growth of 0.69 mb/d.

- In absolute values, the IEA, OPEC, and the EIA non-OECD supply estimates are 30.82 mb/d, 32.54 mb/d, and 33.61 mb/d, respectively for 2022 with the largest divergence in growth estimates between the IEA and EIA at 0.36 mb/d.

The IEA, EIA, and OPEC revise OPEC production estimates.

- The IEA increased its OPEC production estimate for August by 680 kb/d month-on-month (m-o-m) to reach total production of 29.72 mb/d.

- OPEC also revised its assessment of OPEC production upward by 620 kb/d to 29.65 mb/d.

- The EIA revised its assessment upward by 810 kb/d with total OPEC crude production reaching 29.34 mb/d.

2.3 STOCKS

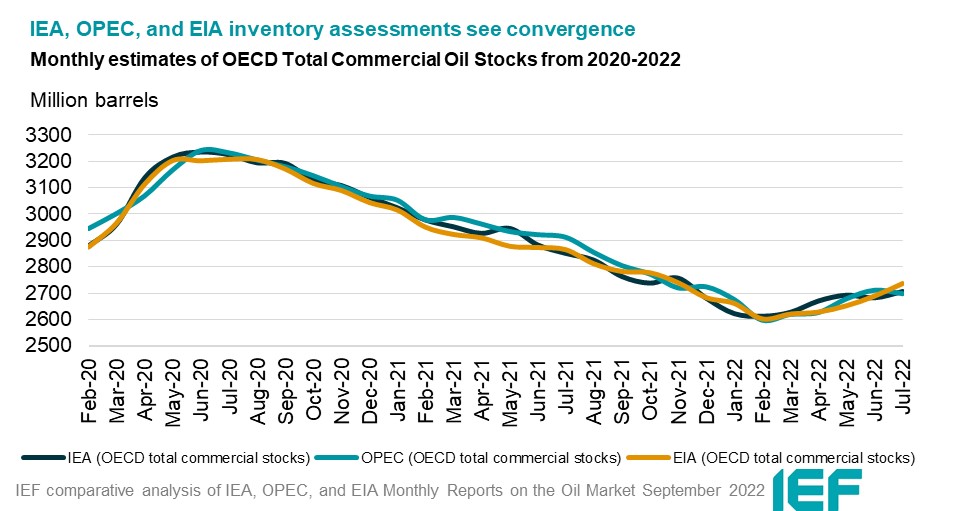

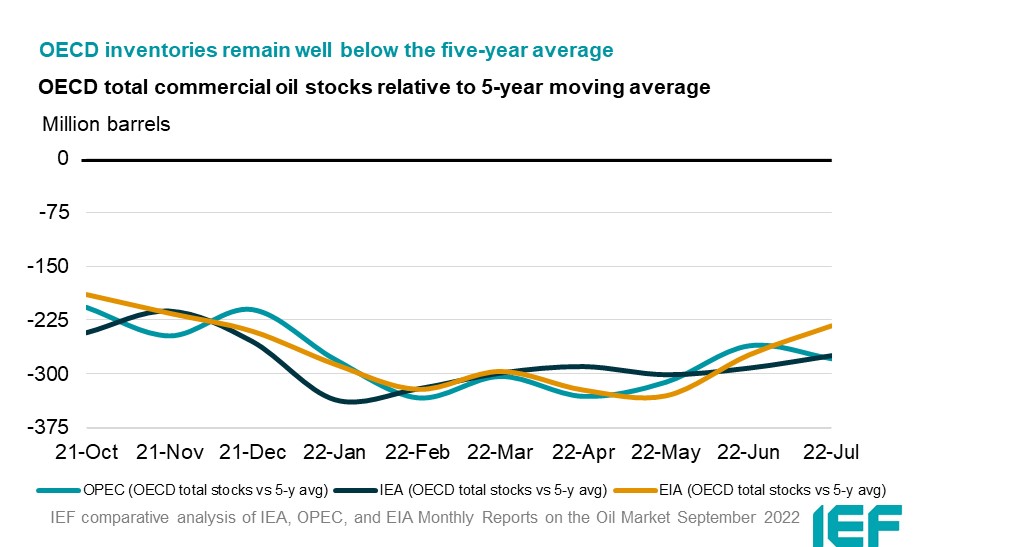

The IEA, OPEC, and EIA continue to display strong alignment on stock figures which are below the five-year average and now below 60 days forward cover.

- The IEA reports OECD stock levels at 2705 mb, which is close to OPEC’s assessment of 2699 mb and EIA’s assessment of 2736 mb. These are around 275 mb, 279 mb, and 232 mb below the five-year average, respectively.

- According to the IEA, crude oil inventories built by 14.8 mb while product stocks built by 29.2 mb. Other oils, including NGLs and feedstocks drew by 0.9 mb. According to OPEC, crude oil stocks built by 6.4 mb while products built by 11.7 mb.

- The EIA estimates OECD inventories rose by 47 mb in July to 2736 mb – 232 mb below the five-year average.

- The widest divergence in inventories is between the EIA and OPEC at 37 mb. Total US crude inventories (excluding SPR) amount to about 427 mb, according to the EIA, which is 3 percent below the five-year average for this time of year.

2.4 Snapshot (mb/d)

3. Global Analysis

Explanatory Note

The IEF conducts a comprehensive comparative analysis of the short-, medium-, and long-term energy outlooks of the IEA, OPEC, and the EIA to inform the IEA-IEF-OPEC Symposium on Energy Outlooks that the IEF hosts in Riyadh as part of the trilateral work programme on a yearly basis.

To inform IEF stakeholders on how perspectives on the oil market of both organisations evolve over time regularly, this monthly summary provides:

- An overview of key events and initiatives in the international policy and market context.

- Key findings and a snapshot overview of data points gained from comparing basic historical data and short-term forecasts of the IEA Oil Market Report, the OPEC Monthly Oil Market Report, and the EIA Short-term Energy Outlook.

- A comparative analysis of oil inventory data reported by the IEA, OPEC, and EIA, and secondary sources in collaboration with Kayrros (added in an updated report on the IEF website).

The International Energy Forum

The International Energy Forum is the leading global facilitator of dialogue between sovereign energy market participants. It incorporates members of International Energy Agency and the Organization of the Petroleum Exporting Countries, and also key players including China, India, Russia and South Africa. The forum's biennial ministerial meetings are the world's largest gathering of energy ministers, where discussions focus on global energy security and the transition towards a sustainable and inclusive energy future. The forum has a permanent secretariat of international staff based in the Diplomatic Quarter of Riyadh, Saudi Arabia. For more information visit www.ief.org.