")

Comparative Analysis of Monthly Reports on the Oil Market

Friday 15 March 2024

Oil Market Context

A subset of OPEC+ members extend ~2.2 mb/d in voluntary cuts through end-June

On March 3rd, several OPEC+ members announced an extension of ~2.2 mb/d in voluntary cuts through 2Q24. The extended cuts include volumes from Saudi Arabia (1.0 mb/d); Russia (0.4 mb/d); Iraq (0.22 mb/d); UAE (0.16 mb/d); Kuwait (0.14 mb/d); Kazakhstan (0.08 mb/d); Algeria (0.05 mb/d); and Oman (0.04 mb/d).

The next OPEC JMMC meeting is scheduled for April 3 and the next OPEC/OPEC+ ministerial meeting is scheduled for June 1. The JMMC meeting will review member's compliance to pledged production cuts and review current market fundamentals. While the JMMC can make recommendations for changes to production levels, any formal changes to production quotas will made during the full OPEC/OPEC+ ministerial.

Global onshore inventories continue to fall

Global onshore inventories fell for a seventh consecutive month in February to their lowest level since at least 2016, according to IEA. Observed onshore inventories fell by 38 mb in February and are down 180 mb since last July. OECD commercial inventories fell counter-seasonally in January and ended the month at 2,759 mb, which is 109 mb below the five-year average.

The drawdown of onshore inventories has been partially offset by a surge of oil in transit as more cargos divert from the Red Sea.

EIA's updated balance warned that 2Q24 could see global inventories draw by 0.9 mb/d (or 83 mb) following OPEC+ announcement of extending cuts through end-June. For the year, EIA expects global stocks to draw by 0.3 mb/d.

Additionally, IEA noted that if OPEC+ members extend their voluntary cuts through end-2024, they also see global inventories drawing by ~0.3 mb/d (or 110 mb), with the steepest draws expected in 3Q24.

Summary of 2023-2025 Balances

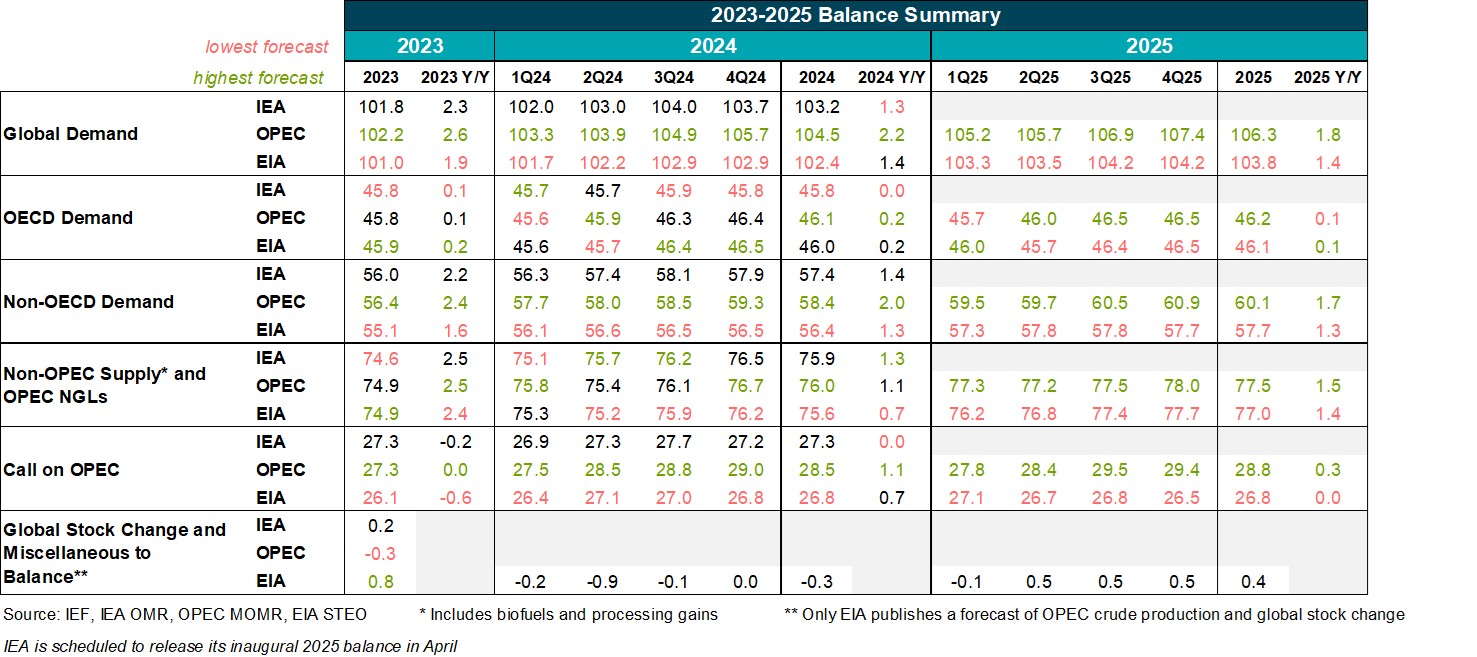

- Demand growth forecasts diverge by 0.9 mb/d in 2024 and 0.4 mb/d in 2025. The divergence has narrowed slightly over the last few months as IEA had revised up its 2024 demand growth steadily over the past 5 months and OPEC's forecast has remained unchanged. OPEC and EIA's 2025 global demand levels diverge by 2.5 mb/d.

- Non-OPEC supply growth is expected to slow from ~2.5 mb/d in 2023 to 0.7-1.3 mb/d this year. IEA sees nearly twice as much 2024 non-OPEC supply growth vs. EIA largely due to a higher US and Russia forecast.

- Baseline 2023 balances still diverge by 1.1 mb/d with EIA estimating a 0.8 mb/d global inventory build for the year, IEA estimating a 0.2 mb/d build and OPEC estimating a 0.3 mb/d draw.

Summary of 2024 Balances and Revisions

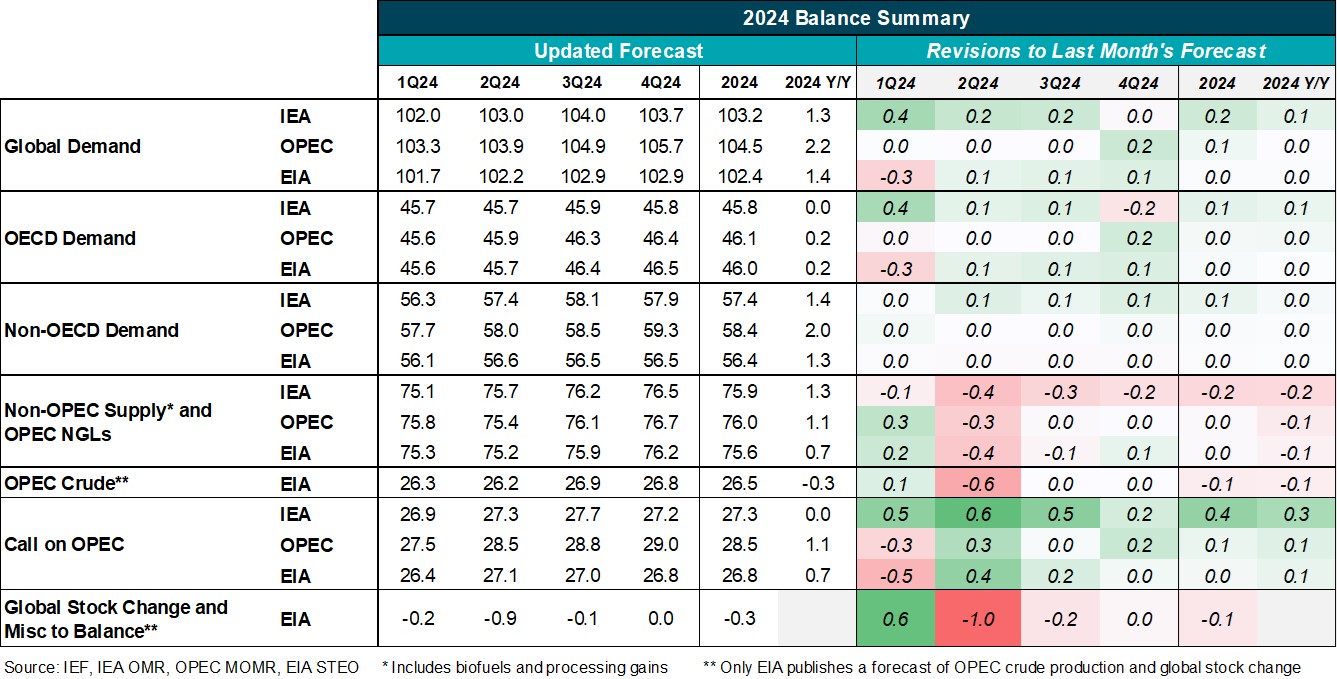

- Global demand forecasts for 2024 were revised marginally higher this month. IEA's forecast remains 0.9 mb/d lower than OPEC's, driven by a 0.6 mb/d lower non-OECD outlook.

- Non-OPEC supply forecasts for 2024 were revised marginally lower this month driven by downwardly revised Russian production forecasts. IEA sees 0.6 mb/d higher non-OPEC supply growth versus EIA due to a higher US and Russian outlook.

- EIA is the only one of the three agencies that provides an OPEC crude and global stock change forecast. EIA tightened its 2Q24 balance by 1 mb/d due to the extension of OPEC+ cuts and now sees a 0.9 mb/d global stock draw next quarter

Evolution of 2024 Annual Demand Growth Forecasts

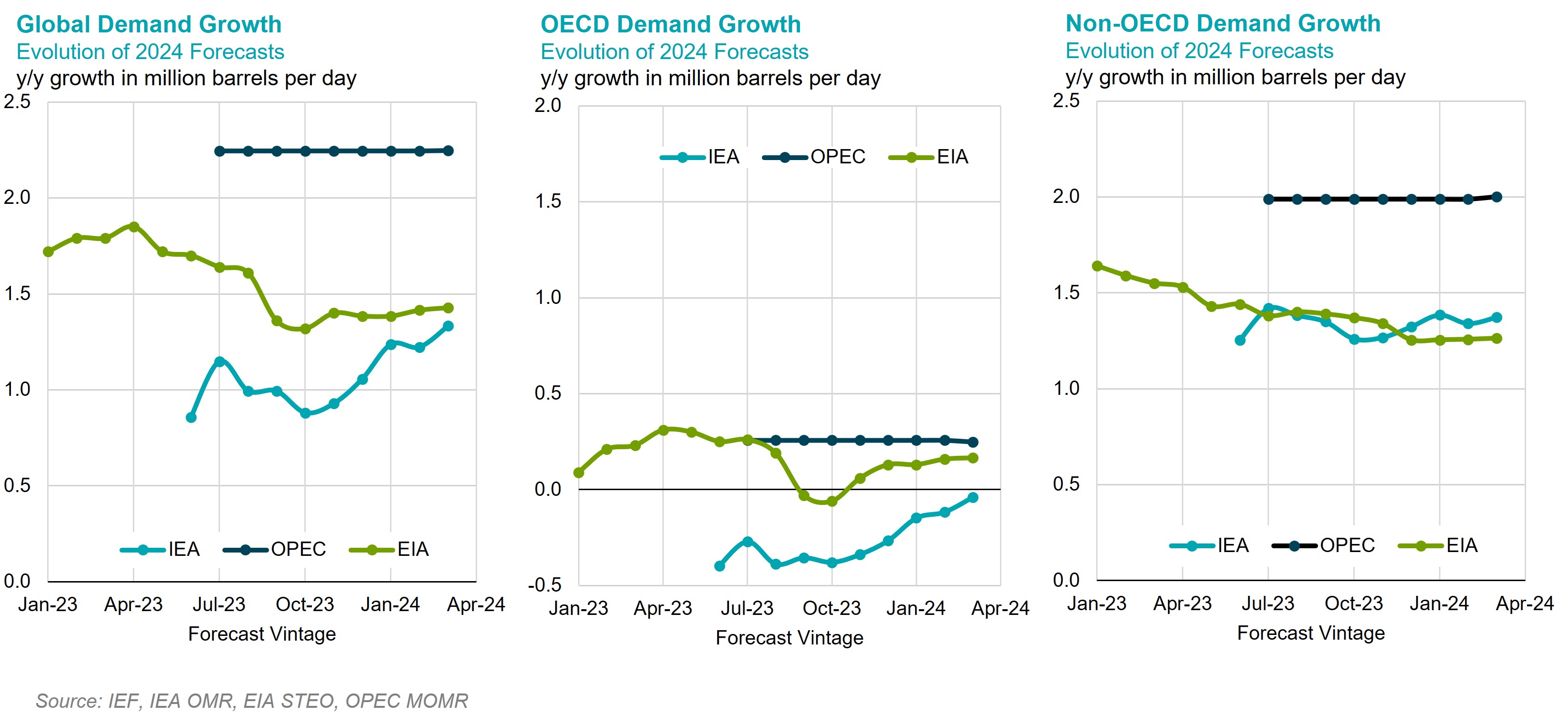

- OPEC's 2024 global demand growth forecast is 0.9 mb/d higher than IEA's due to higher Middle East, Russian, other non-OECD and OECD Americas projections.

- IEA revised up OECD demand growth for a 5th consecutive month, but it still sees a slight contraction this year while OPEC and EIA see growth.

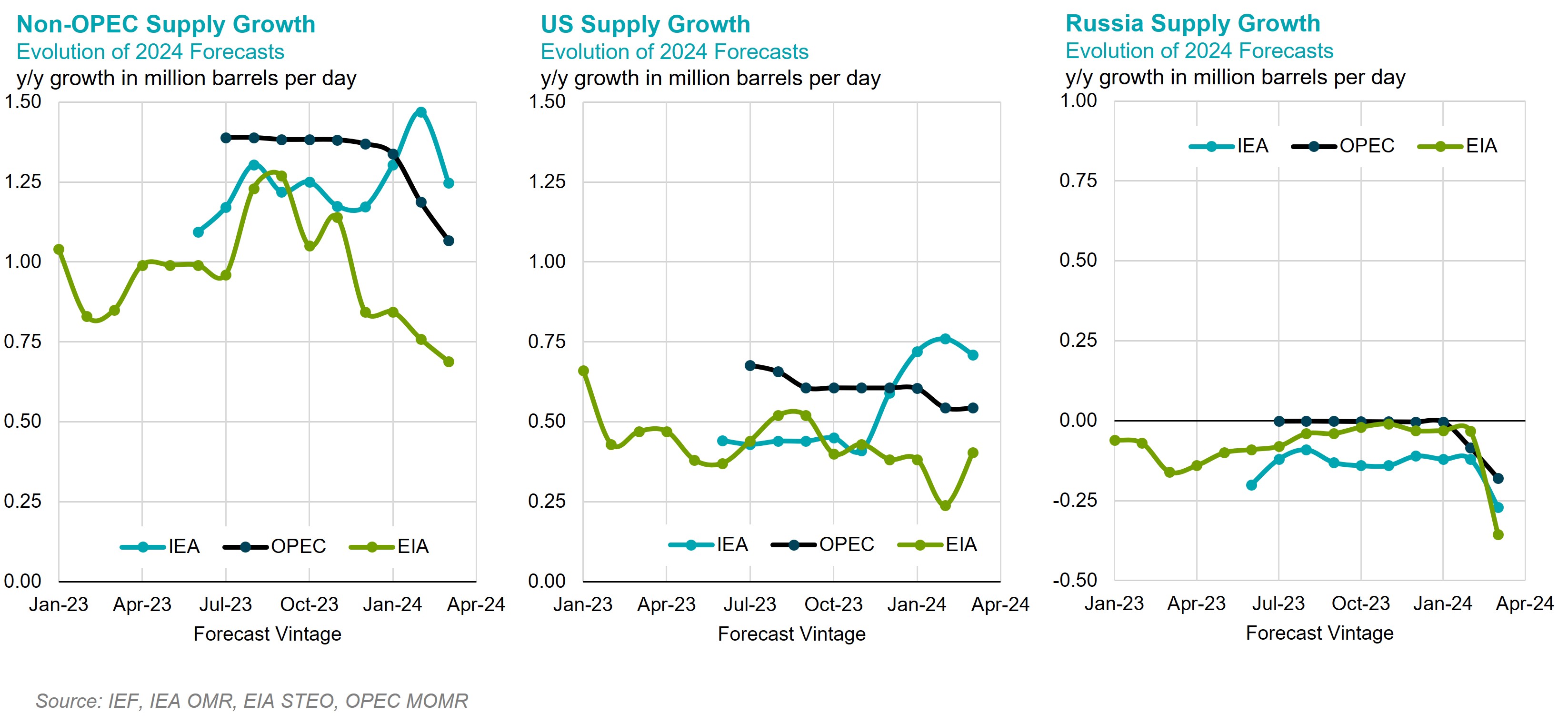

Evolution of 2024 Annual Non-OPEC Supply Growth Forecasts

- EIA continues to see lower non-OPEC supply growth than IEA and OPEC due primarily to a weaker US and Russia forecast.

- All three agencies revised their 2024 Russian supply forecasts lower due to the extension and deepening of cuts in coordination with a sub-set of OPEC+ producers in 2Q24.