")

Comparative Analysis of Monthly Reports on the Oil Market

Thursday 22 January 2026

Summary

Demand

OPEC: Global oil demand is projected to rise by around 1.4 mb/d in 2026, with growth in non-OECD economies (approximately 1.2 mb/d) accounting for the bulk of the increase, while OECD demand expands more modestly, by about 0.15 mb/d. In 2027, demand growth remains robust at around 1.3 mb/d year-on-year, again driven predominantly by non-OECD countries (around 1.2 mb/d), with OECD demand rising by roughly 0.1 mb/d. Developing Asia, led by China and India, underpins global economic expansion, alongside steady growth in major emerging economies such as Brazil and Russia. Easing inflationary pressures and the associated normalization of monetary policy support macroeconomic conditions.

EIA: Global liquid fuels consumption rises by about 1.1 mb/d in 2026 and 1.3 mb/d in 2027, supported by strengthening global economic activity. World GDP growth averages around 3.1% in 2026 and 3.3% in 2027. Non-OECD countries account for the bulk of demand growth, with increases of roughly 1.1 mb/d in 2026 and 1.2 mb/d in 2027. The expansion is concentrated mainly in Asia, led by India, where consumption rises by close to 0.3 mb/d in both 2026 and 2027, while China’s demand increases by just over 0.2 mb/d in each year.

IEA: Global oil demand growth rises by about 0.9 mb/d year-on-year in 2025, following an increase of around 0.8 mb/d in the previous year. Non-OECD economies, led by China and India, are the main drivers, contributing roughly 0.9 mb/d in 2025 and around 1.0 mb/d in 2026, while OECD demand declines by about 0.1 mb/d year-on-year in 2025 and remains broadly flat in 2026. The IEA expects oil demand growth in 2026 to be held back by weaker-than-average global economic growth, ongoing improvements in energy efficiency, and strong electric-vehicle sales in some markets

Differences across agency outlooks remain evident, with global oil demand projections diverging by around 0.5 mb/d in 2026, while growth projections for 2027 are more closely aligned at around 1.3 mb/d year-on-year between OPEC and the EIA.

Supply

OPEC: Non-DoC liquids supply increases by around 0.6 mb/d year-on-year in 2026, with Brazil, Canada, the United States and Argentina leading the growth. A similar expansion is seen in 2027, driven mainly by Brazil, Canada, Qatar and Argentina. DoC NGLs and non-conventional liquids rise by about 0.1 mb/d in 2026 to average around 8.8 mb/d, with a further increase of roughly 0.1 mb/d in 2027, lifting the average to about 8.9 mb/d.

EIA: Global liquid fuels production is projected to increase by around 1.4 mb/d in 2026, with growth driven primarily by higher crude oil output from OPEC+ producers and non-OPEC+ production. In 2027, supply growth moderates to about 0.5 mb/d year-on-year and is led mainly by non-OPEC+ countries. In other words, the supply profile indicates a shift in growth momentum toward non-OPEC+ producers in 2027, following a year in which OPEC+ accounts for the bulk of the increase.

IEA: Global oil supply increases by around 3.0 mb/d in 2025 and is expected to rise by a further 2.5 mb/d in 2026, reaching an annual average of about 108.7 mb/d. Non-OPEC+ producers account for a large share of this growth, contributing around 1.8 mb/d (about 60%) of the 2025 increase and approximately 1.3 mb/d (around 50%) of the 2026 expansion. IEA projects non-DoC liquids supply and DoC NGLs to increase by around 1.5 mb/d year-on-year in 2026.

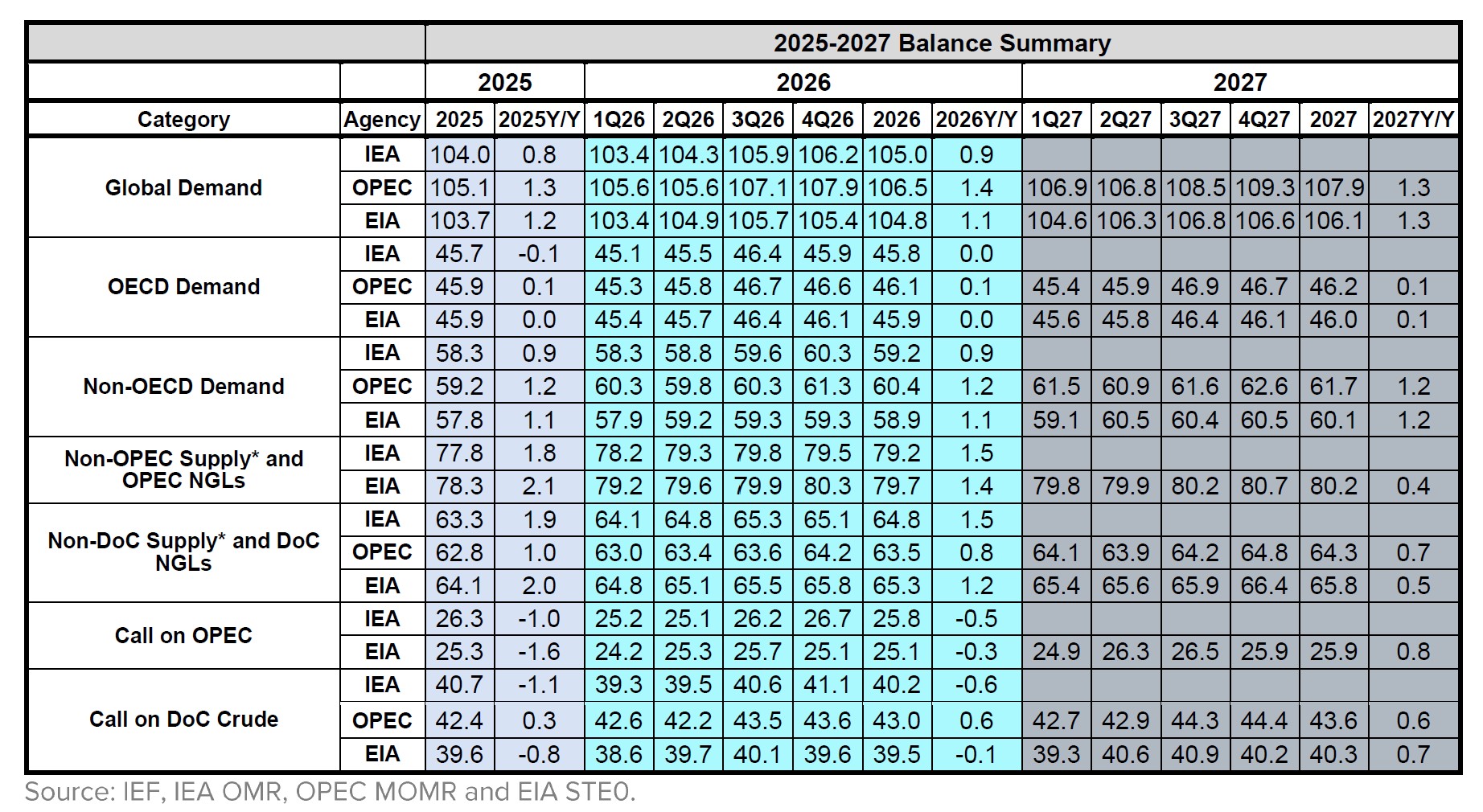

2025-2027 Balance Summary

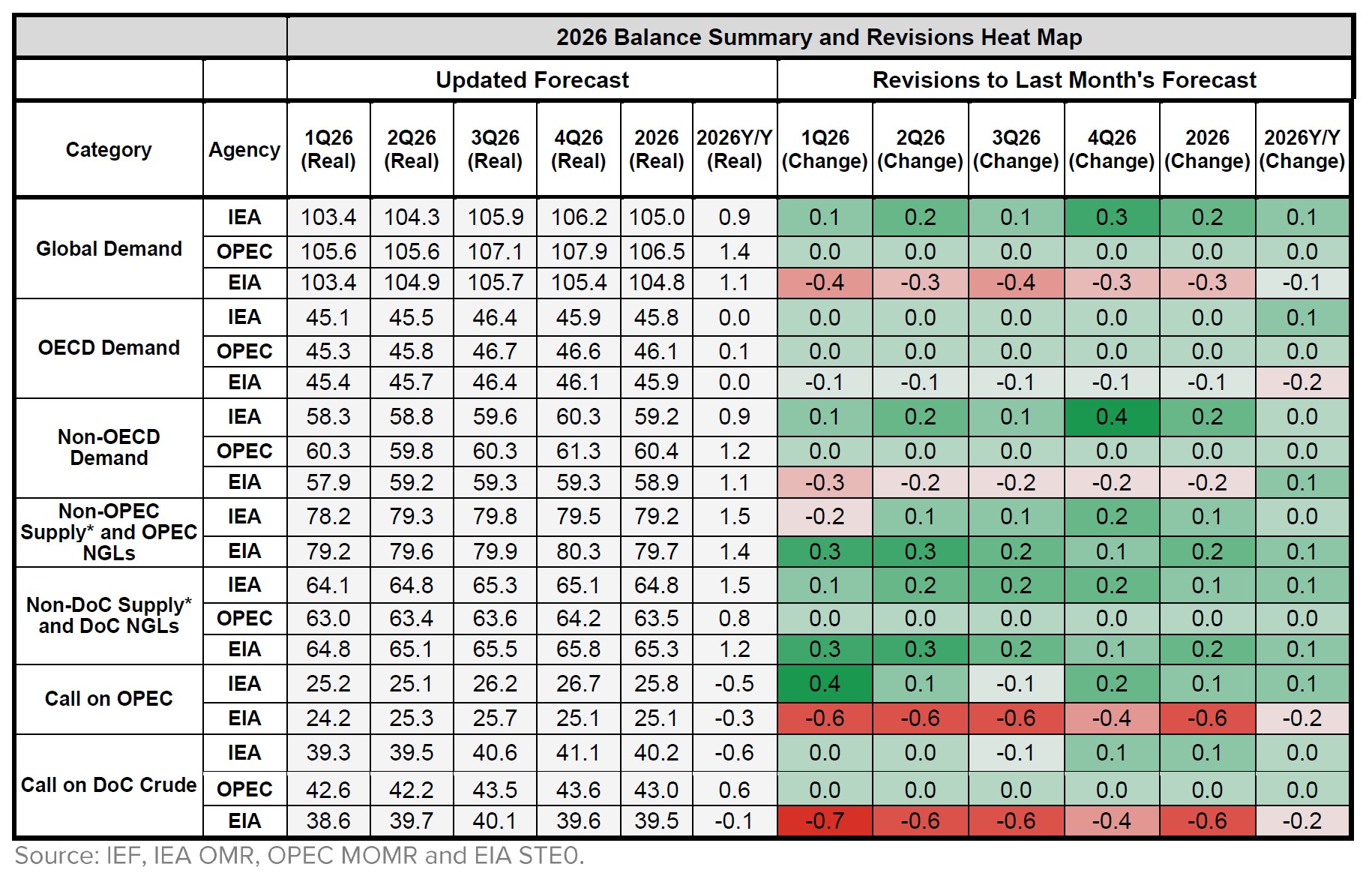

Global oil demand estimates for 2026 vary among the agencies, with OPEC projecting the highest at 106.5 mb/d, followed closely by IEA at 105 mb/d and EIA at 104.8 mb/d. For OECD demand, OPEC again leads with 46.1 mb/d, while EIA and IEA report lower figures of 45.9 mb/d and 45.8 mb/d, respectively. In the non-OECD category, OPEC's estimate of 60.4 mb/d surpasses both EIA's 58.9 mb/d and IEA's 59.2 mb/d. By 2027, OPEC continues to predict higher demand across all categories, notably at 107.9 mb/d for global demand. Regarding supply, the call on DoC crude is projected at 43 mb/d by OPEC, compared to 40.2 mb/d from IEA and 39.5 mb/d from EIA. For 2027, OPEC maintains its higher call at 43.6 mb/d, while EIA's estimate is lower at 40.3 mb/d.

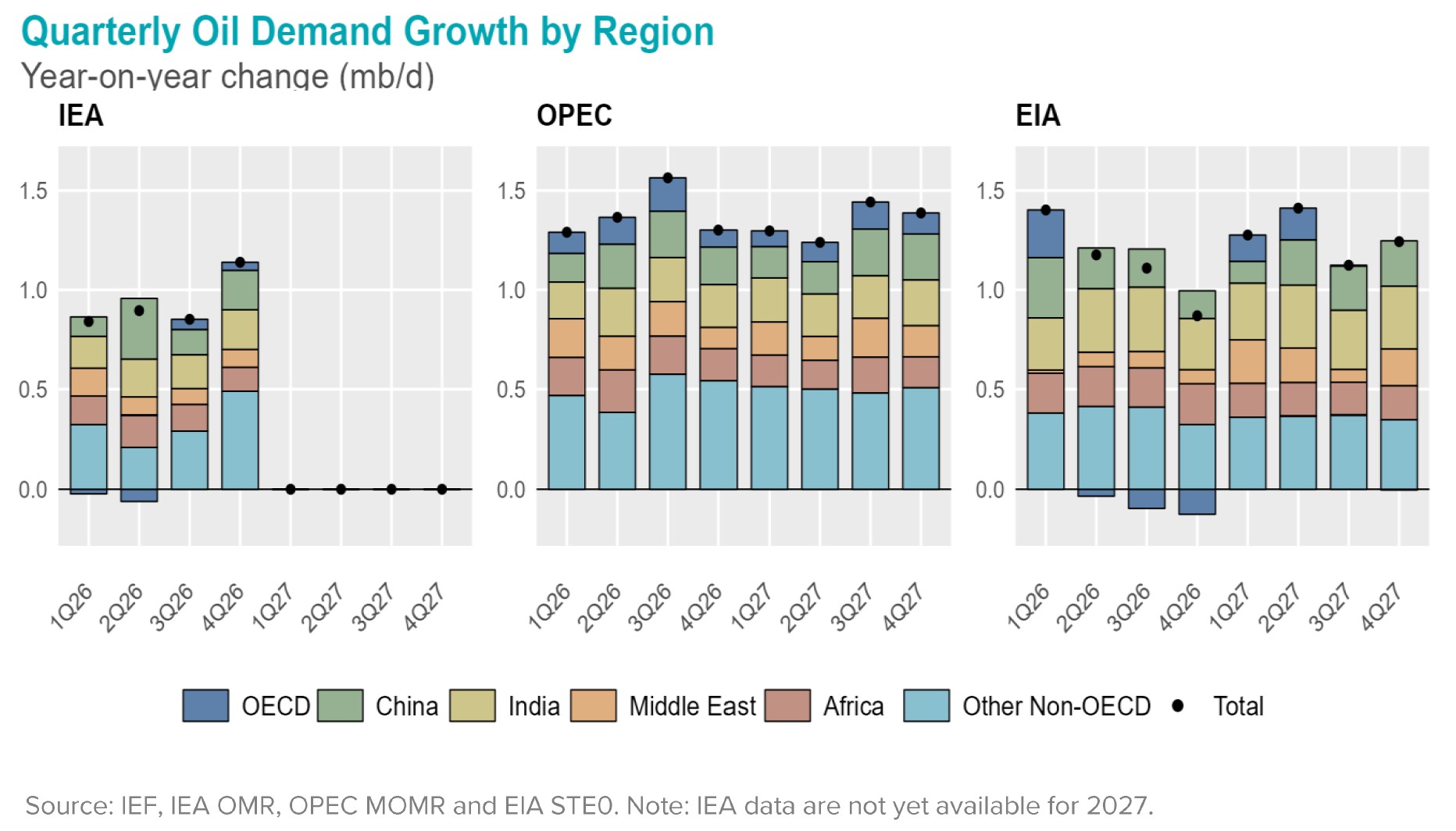

From 1Q26 to 4Q27, OPEC consistently reported the highest oil demand totals across all periods, with values ranging from 1.3 mb/d in 1Q26 to 1.4 mb/d in 4Q27. The EIA projects demand growth to peak at around 1.4 mb/d in the second quarter of 2027, while the IEA maintains an average growth rate of about 0.9 mb/d over 2026.

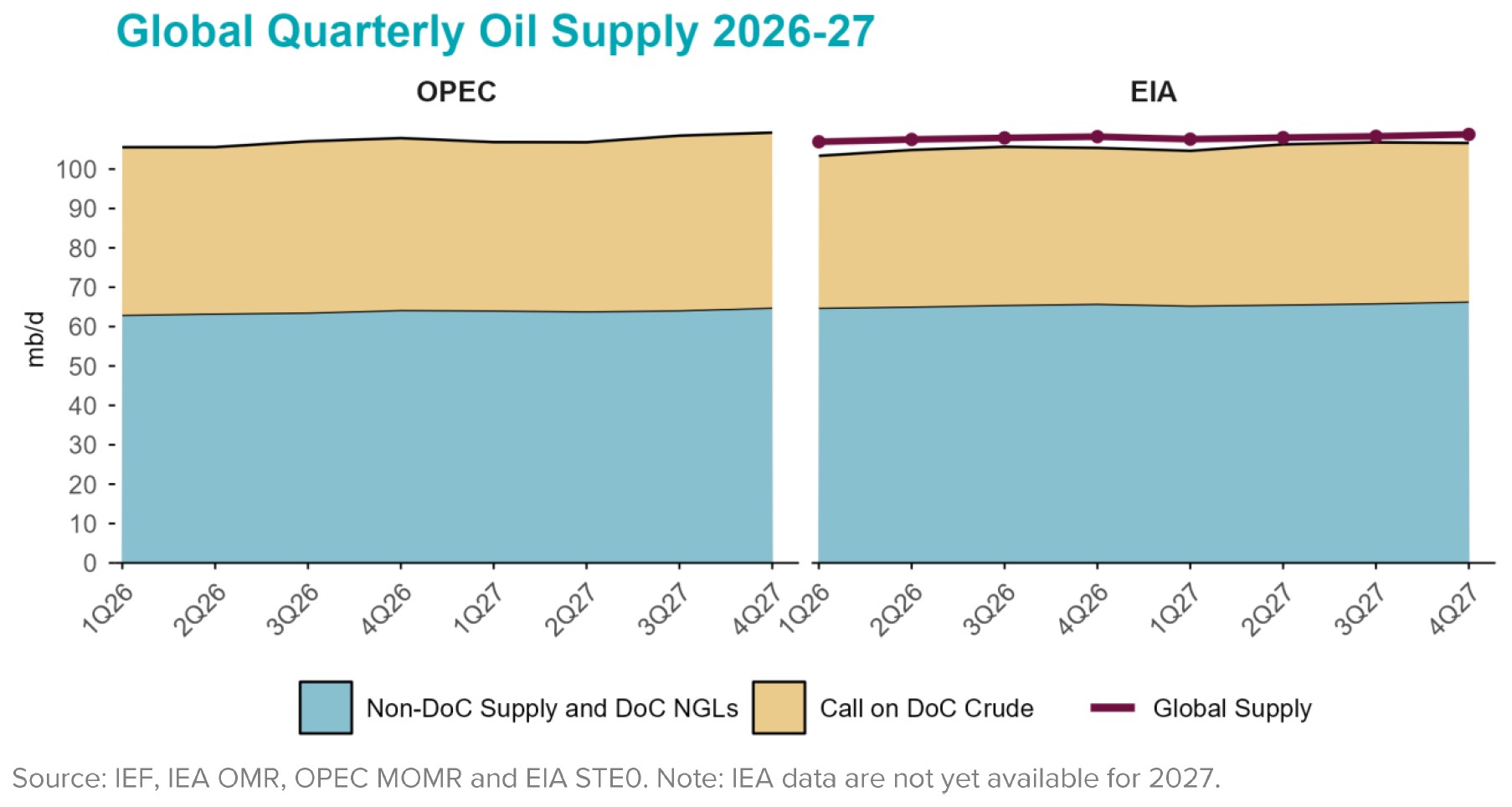

In the first quarter of 2026, Non-DoC supply estimates show EIA at 64.8 mb/d, slightly higher than IEA's 64.1 mb/d and OPEC's 63 mb/d. This trend continues into subsequent quarters, with EIA consistently reporting higher figures, reaching 65.8 mb/d in the fourth quarter of 2026, compared to IEA's 65.1 mb/d and OPEC's 64.2 mb/d. By 2027, EIA projects an increase to 66.4 mb/d in the fourth quarter, while OPEC anticipates 64.8 mb/d, indicating a growing divergence in supply forecasts among the agencies.

2026 Outlook Comparison

Divergence in global demand growth across agencies reaches around 0.5 mb/d year-on-year. OPEC maintains its projections relative to last month's assessment, while the EIA revises its outlook down by a quarterly average of about 0.35 mb/d. The IEA, by contrast, raises its estimate of global demand growth by around 0.1 mb/d compared with its previous month's outlook, bringing growth to about 0.9 mb/d year-on-year in 2026. A gap of roughly 0.3 mb/d is observed in non-OECD demand growth between OPEC and the IEA.

On the supply side, a wider divergence is seen in non-DoC liquids and DoC NGLs, with a difference of around 0.7 mb/d. The IEA projects growth of about 1.5 mb/d year-on-year, while OPEC estimates an increase of around 0.8 mb/d.

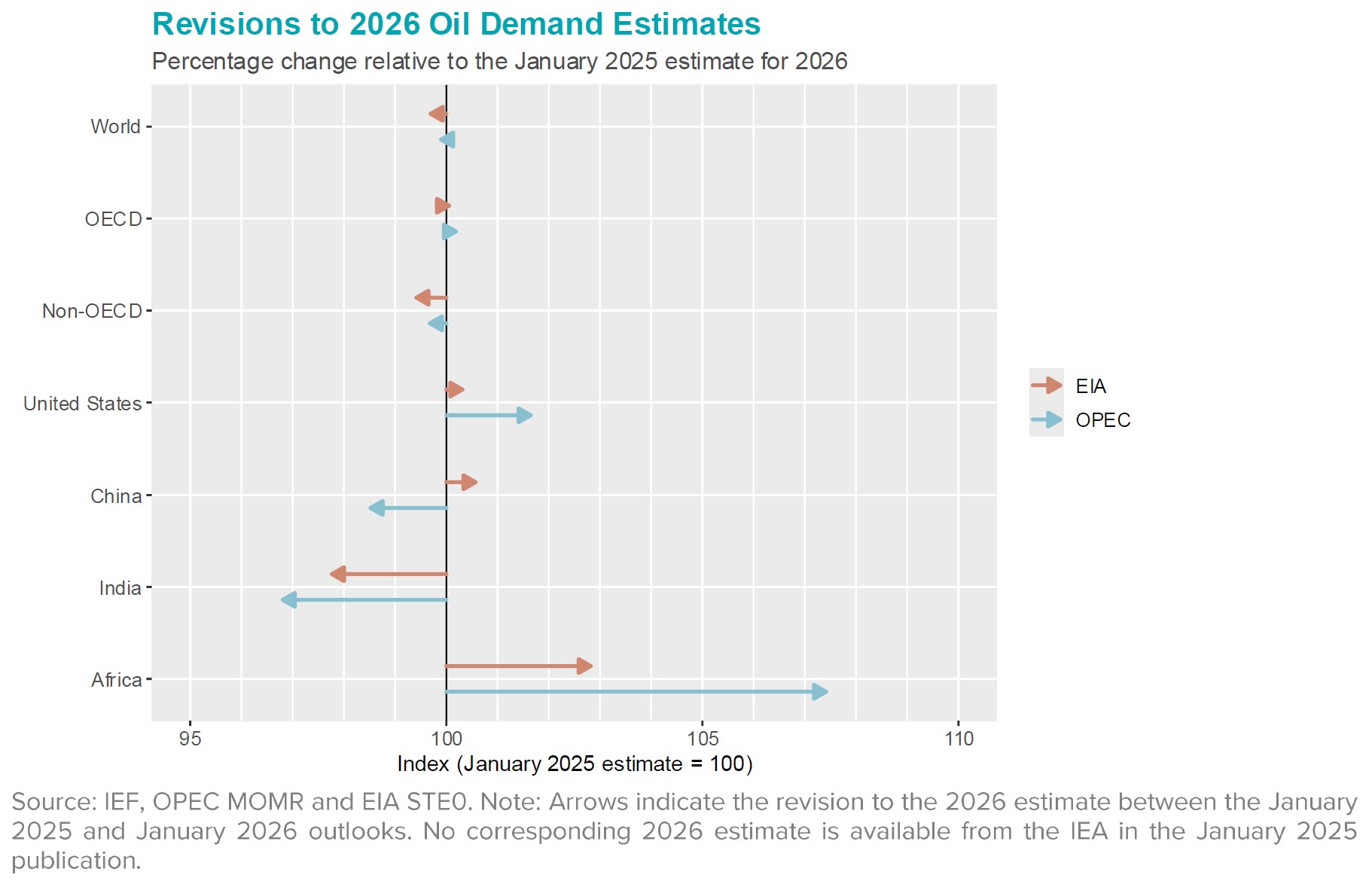

Revisions to 2026 oil demand between January 2025 and January 2026 outlooks are limited at the global and aggregate levels, with world, OECD and non-OECD totals remaining close to their earlier estimates. At the regional level, Africa and the United States record upward revisions in both agencies’ assessments, with larger increases in OPEC’s January 2026 estimate than in the EIA’s, relative to their respective January 2025 outlooks. OPEC revises its estimate for African demand in 2026 upward by around 7% compared with its January 2025 projection.

By contrast, China and India show downward revisions in OPEC’s January 2026 outlook relative to January 2025, while the EIA revises its 2026 demand estimate upward for China and downward for India over the same period.

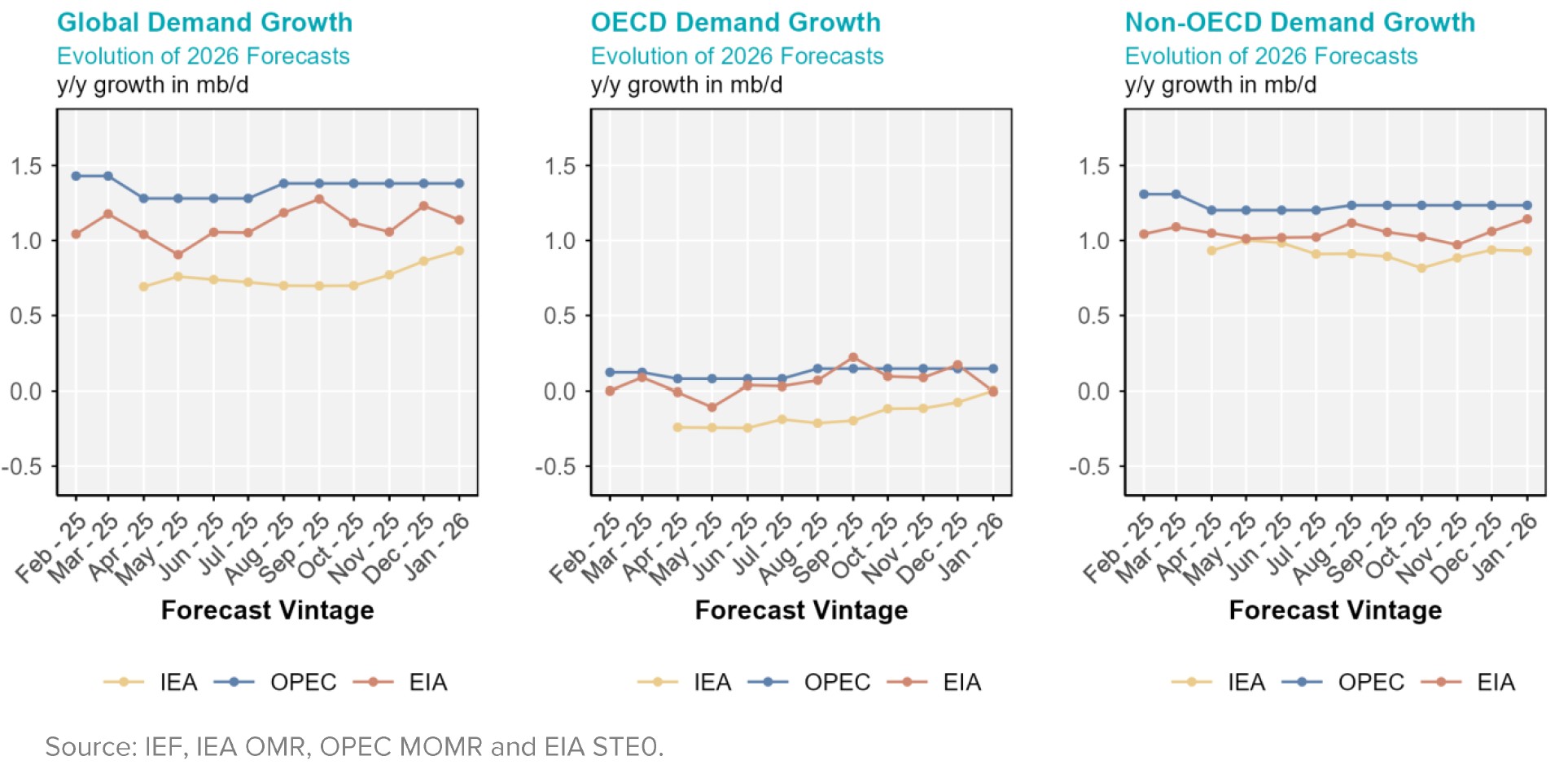

Evolution of 2026 Annual Demand-Supply Growth Forecasts

OPEC maintains its demand growth projection, consistently indicating global demand growth of around 1.4 mb/d with relatively limited revisions. The EIA reports slightly lower demand growth, in the range of roughly 0.9–1.3 mb/d, while the IEA shows the lowest demand trajectory at about 0.7–0.9 mb/d. Across all outlooks, demand growth in non-OECD regions accounts for the bulk of the increase, contributing around 1.1–1.3 mb/d, compared with much smaller gains in the OECD of roughly 0.0–0.15 mb/d over the short-term.

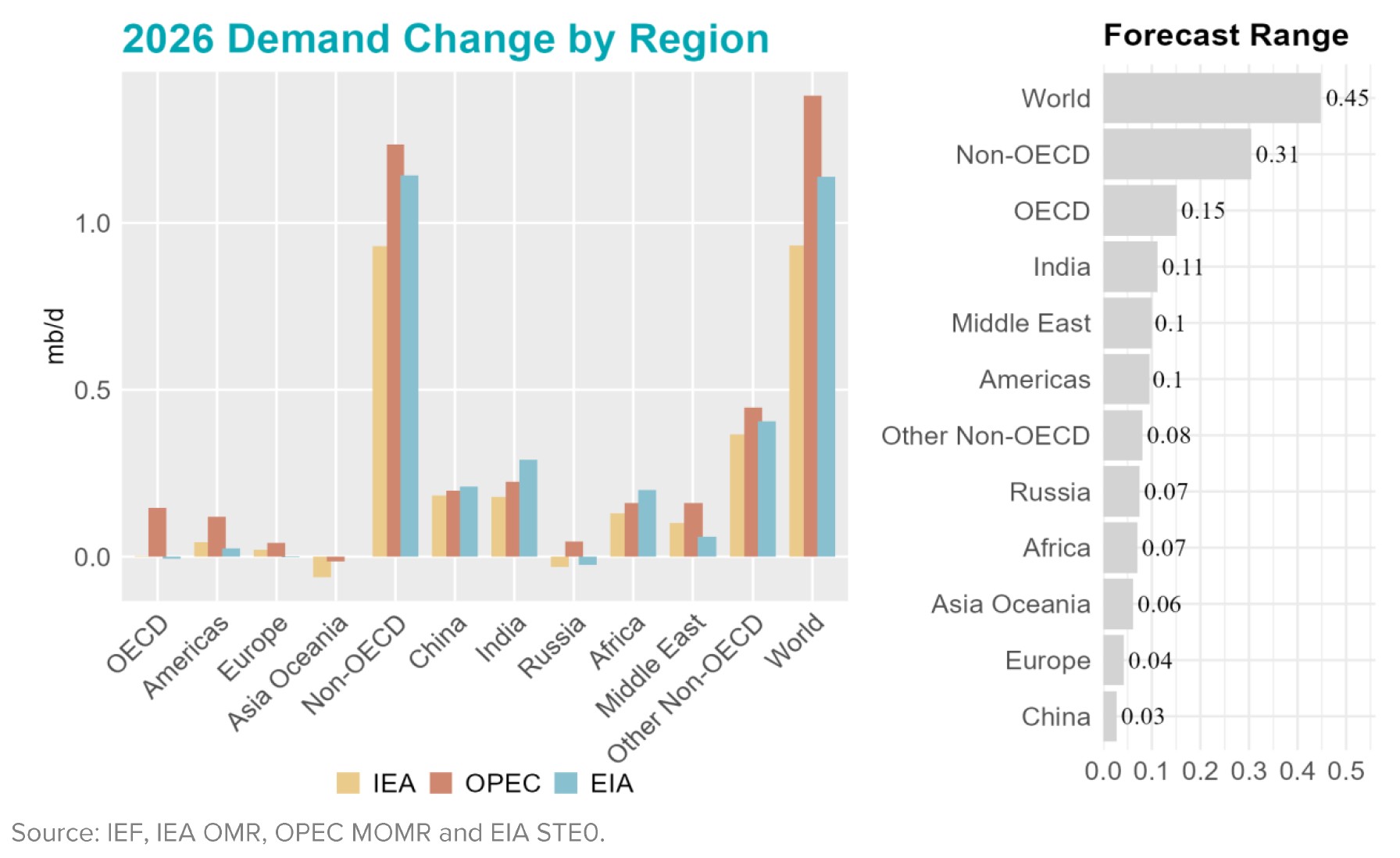

India’s oil demand growth is expected to rise by around 0.3 mb/d year-on-year this year. Growth in China is slightly slower, averaging about 0.2 mb/d, while Africa also records an increase of around 0.2 mb/d, driven mainly by expanding consumption in sub-Saharan Africa.

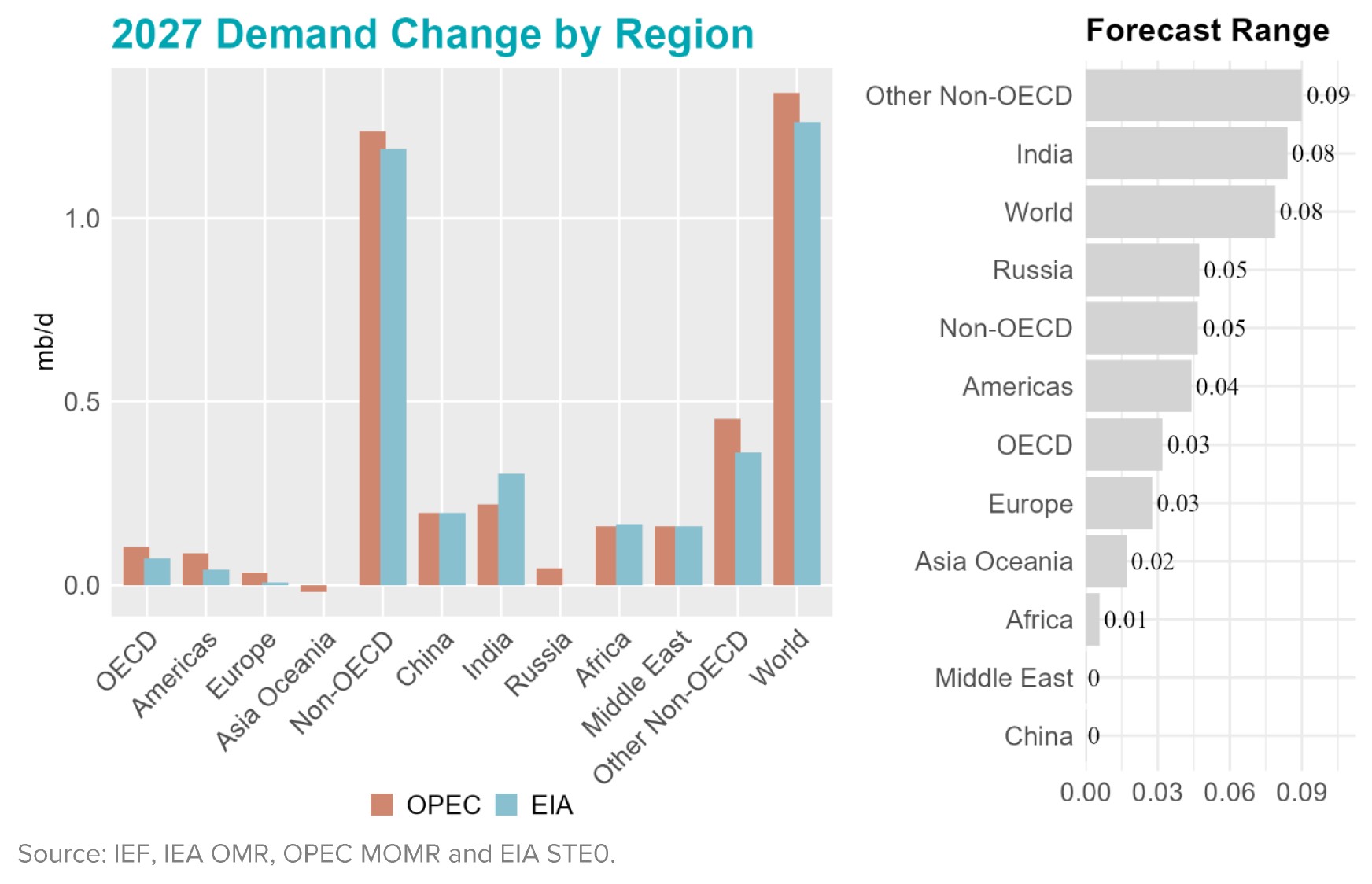

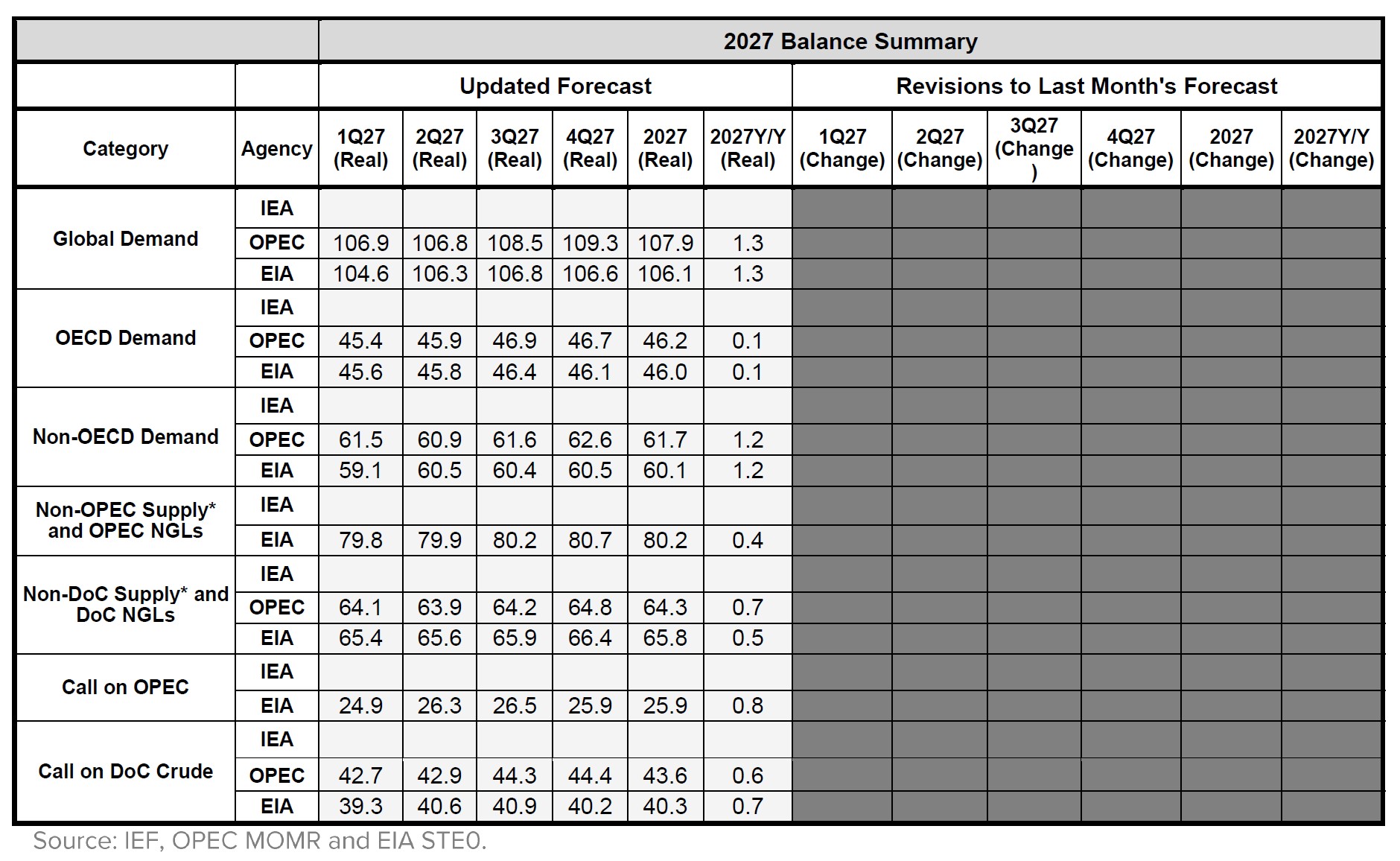

2027 Outlook Comparison

Global demand growth in 2027 is broadly aligned across outlooks, with both OPEC and the EIA projecting an increase of around 1.3 mb/d year-on-year, despite differences of more than 1 mb/d in their absolute demand levels. A similar pattern is observed in the non-OECD region, where OPEC and EIA show demand rising by about 1.2 mb/d, while both indicate a more modest increase of around 0.1 mb/d year-on-year for OECD.

On the supply side, OPEC projects non-DoC liquids supply and DoC NGLs to expand by around 0.7 mb/d in 2027, reaching an average of about 64.3 mb/d, while the EIA expects supply growth of roughly 0.5 mb/d. These divergences in demand and supply assessments highlight the differing views on market dynamics as the global oil market moves into 2027.

On a regional basis, India shows a notable rise, with the EIA indicating an increase of around 0.30 mb/d and OPEC reporting growth of about 0.22 mb/d. China also contributes significantly, with both agencies showing an increase of roughly 0.2 mb/d. African demand continues to expand, with the EIA projecting growth of about 0.17 mb/d and OPEC estimating around 0.16 mb/d.

By contrast, OECD demand growth remains relatively modes. The EIA indicates an increase of around 0.07 mb/d, while OPEC reports about 0.11 mb/d.