")

Comparative Analysis of Monthly Reports on the Oil Market

Friday 13 February 2026

Summary

Demand

OPEC: Global oil demand increases by 1.4 mb/d year on year (y/y) in 2025, unchanged from last month's estimate. OECD demand grows by about 0.15 mb/d, led by the Americas and OECD Europe, while OPEC projections show non-OECD demand expanding by roughly 1.2 mb/d, driven by India, China and other Asian countries. Growth is supported by strong air travel, road mobility, industrial activity and capacity additions. In 2027, demand rises by a further 1.3 mb/d, with modest OECD growth (~0.1 mb/d) and continued expansion in non-OECD Asia (~1.2 mb/d).

EIA: Global liquid fuels consumption is projected to grow by approximately 1.2 mb/d in 2026 and by a further 1.3 mb/d in 2027 y/y, with the expansion driven predominantly by non-OECD countries. Non-OECD demand alone is expected to increase by about 1.1 mb/d in 2026 and 1.2 mb/d in 2027. EIA projections show most of this growth is concentrated in Asia, led by India, where consumption rises by roughly 0.3 mb/d in both years, and China, where demand increases by about 0.2 mb/d annually. The IEA also expects mo derate growth in OECD liquid fuel consumption in 2027.

IEA: IEA projects global oil demand to increase by approximately 0.85 mb/d, about 0.1 mb/d higher than last year's growth. The monthly update revises the growth estimate down by roughly 0.1 mb/d year on year compared with the previous assessment. IEA expects global demand growth this year to be driven entirely by non-OECD countries , led by China, with petrochemical feedstock accounting for more than half of the increase.

The divergence in global demand growth projections across agencies reaches approximately 0.6 mb/d y/y in 2026 and 0.2 mb/d y/y between OPEC and EIA in 2027; no IEA projection is available for 2027.

Supply

OPEC: Non-DoC liquids production is projected to increase by approximately 0.6 mb/d to reach an average of 54.8 mb/d in 2026, with Brazil, Canada, the US, and Argentina being the primary drivers of this growth. OPEC sees non-DoC liquids production growing by a s imilar 0.6 mb/d to average 55.4 mb/d in 2027, led by Brazil, Canada, Qatar, and Argentina. OPEC expects non-DoC supply and Doc NGLs to grow by 0.8 mb/d y/y in 2026 and by a further 0.7 mb/d in 2027.

EIA: Global liquid fuels production is projected to increase by approximately 1.6 mb/d year on year in 2026 and by 0.9 mb/d in 2027, both below the stronger growth observed in 2025 (3.0 mb/d). EIA projections show that the 2026 increase is led by supply growth from countries outside OPEC+, primarily in Latin America, including Argentina, Brazil and Guyana. The same pattern holds in 2027, with most additional supply expected to originate from non-OP EC+ producers.

IEA: Global oil supply rises by around 2.4 mb/d in 2026 to reach approximately 108.6 mb/d. The increase is distributed broadly evenly between OPEC+ and non-OPEC+ producers, in contrast to EIA projections, which place most supply growth outside OPEC+. IEA projec ts non-DoC supply and DoC NGLs to grow by about 1.4 mb/d y/y in 2026, representing a downward revision of roughly 0.1 mb/d from last month's estimate.

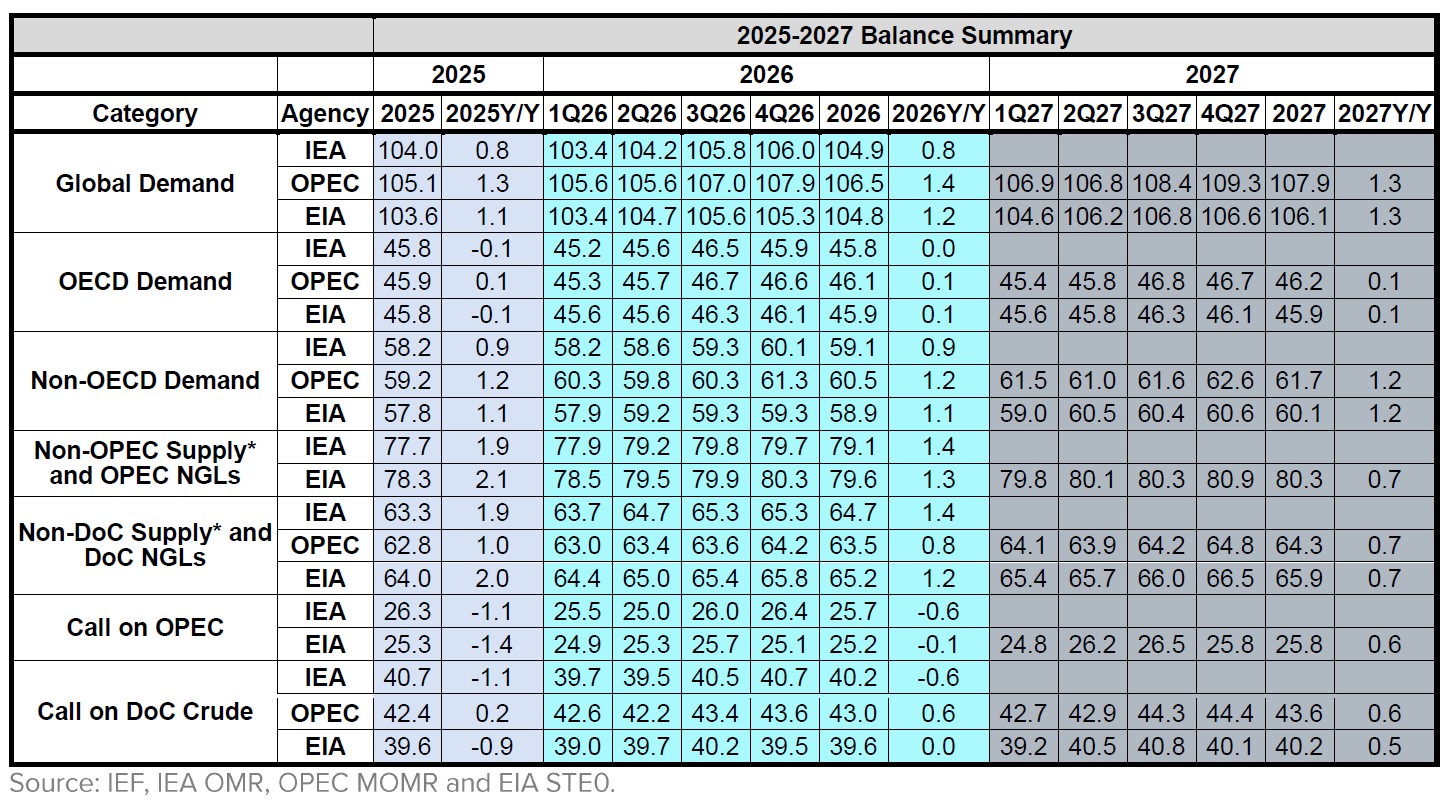

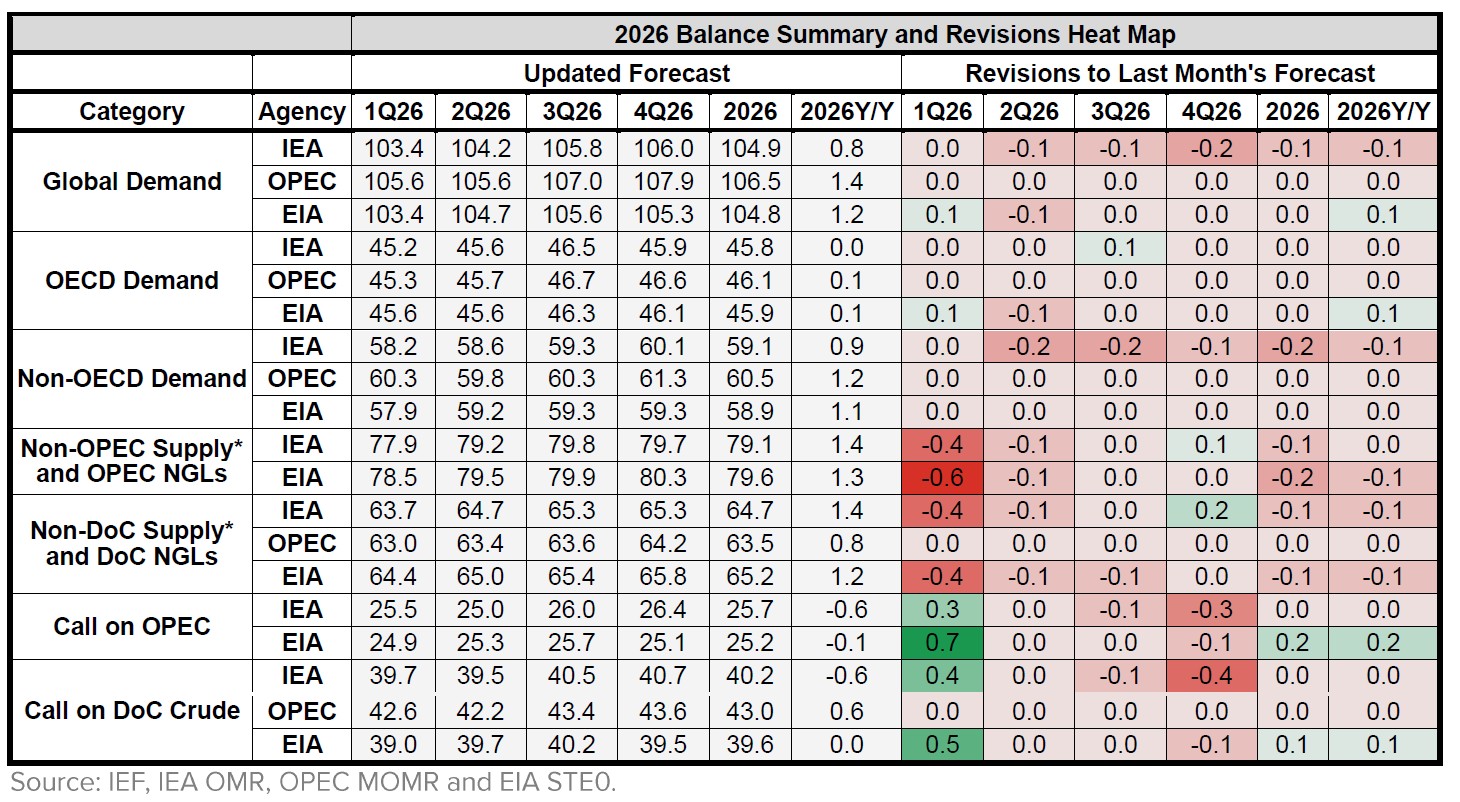

2025-2027 Balance Summary

In 2026, global demand projections show a range from 104.8 mb/d by EIA to 106.5 mb/d by OPEC, indicating a spread of 1.7 mb/d. OECD demand estimates are closely aligned across agencies, with EIA at 45.9 mb/d, IEA at 45.8 mb/d, and OPEC at 46.1 mb/d. Non-OECD demand show s a wider spread, with OPEC highest at 60.5 mb/d, compared with 58.9 mb/d (EIA) and 59.1 mb/d (IEA). By 2027, global demand increases across agencies, with OPEC highest at 107.9 mb/d. On the supply side, both EIA and OPEC project growth of ab out 0.7 mb/d y/y in non-DoC supply and DoC NGLs.

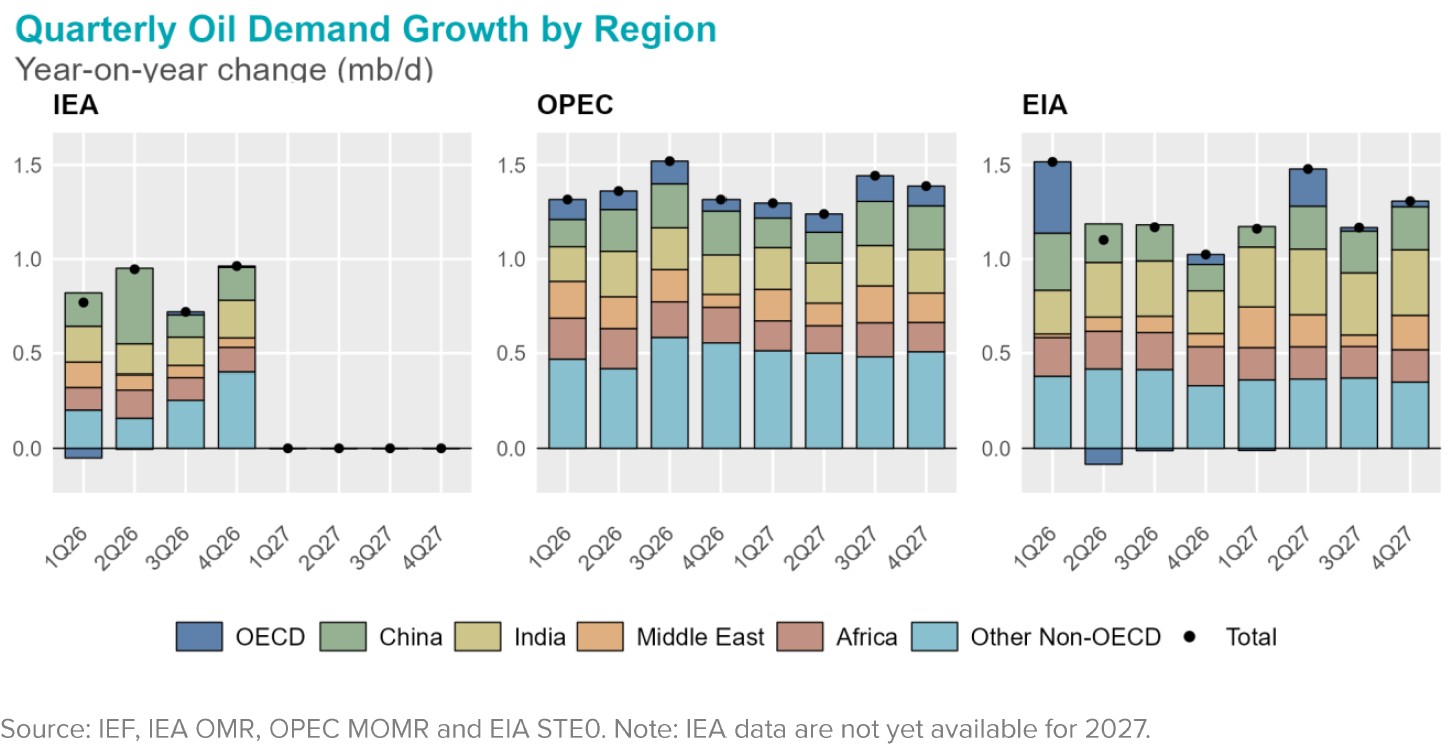

From 1Q26 to 4Q27, OPEC's quarterly estimates of global oil demand growth are the highest in most quarters. EIA demand growth totals fluctuate, peaking at 1.516 mb/d in 1Q26 and falling to 1.023 mb/d in 4Q26, while IEA estimates are generally lower on aver age. Agency projections are more consistent for Africa, whereas EIA projects stronger growth in India than the other agencies.

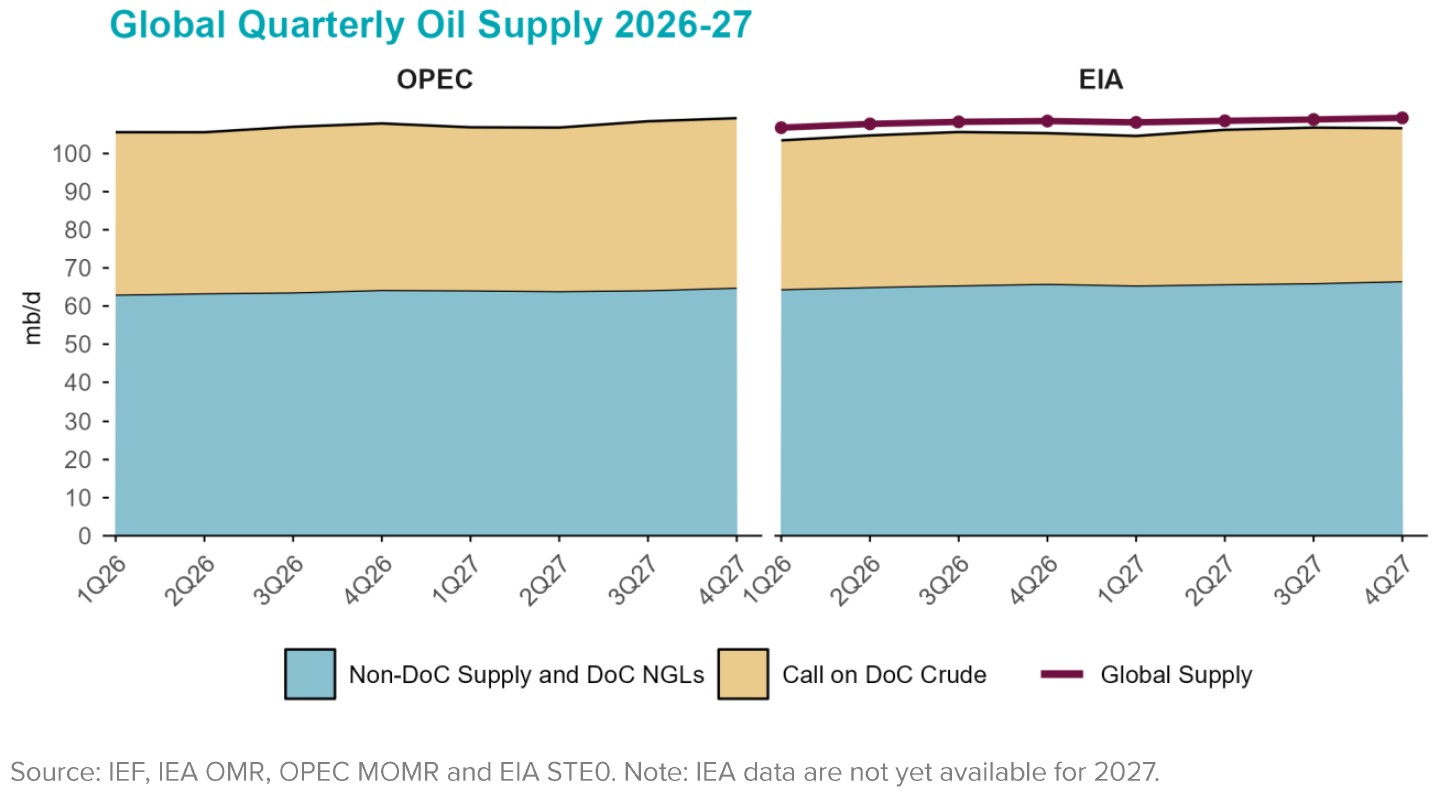

In the first quarter of 2026, EIA projects non-DoC supply and DoC NGLs at 64.4 mb/d, exceeding OPEC's estimate of 63 mb/d. This pattern persists in subsequent quarters, with EIA consistently reporting higher values, reaching 66.5 mb/d in 4Q27 compared with 64.8 mb/d in OPEC's projections. For the call on DoC crude, OPEC estimates 42.6 mb/d in 1Q26 and remains above EIA projections throughout the analysed period.

2026 Outlook Comparison

Differences across agencies in global demand projections show a gap of around 0.6 mb/d year on year. OECD demand estimates from IEA and OPEC remain unchanged from last month's assessment, while EIA revises its latest monthly estimate up by about 0.1 mb/d. Non-OECD demand shows a wider divergence of roughly 0.3 mb/d. On the supply side, both IEA and EIA revise down their 1Q26 estimates for non-OPEC supply and OPEC NGLs by an average of about 0.5 mb/d.

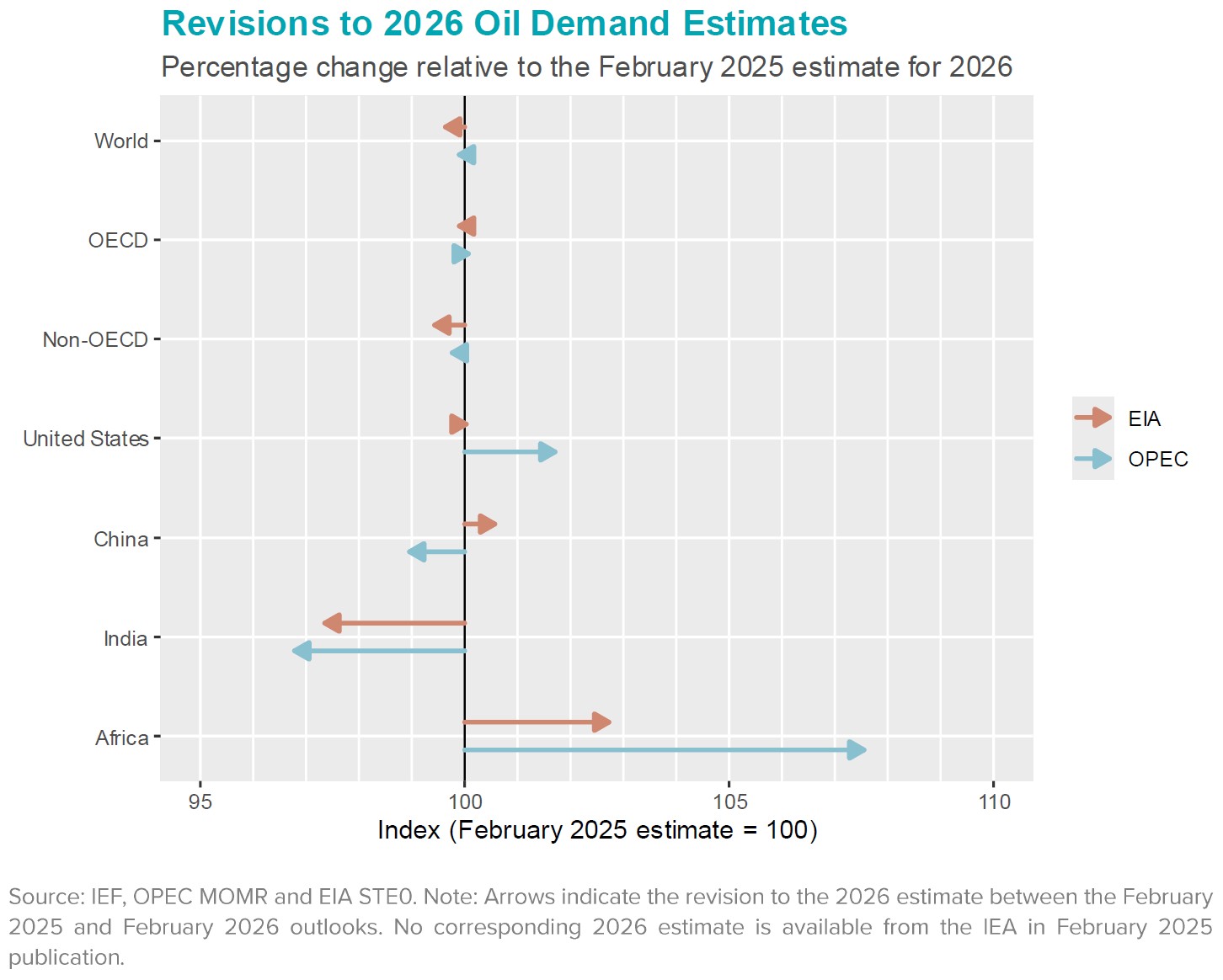

Recent outlook releases show modest adjustments to 2026 oil demand at the global aggregate level. Total world demand, as well as OECD and non-OECD aggregates, remain broadly in line with earlier projections. Differences become more visible on the country and regional scale. Both agencies raise their 2026 demand estimates for Africa, with larger upward adjustments in OPEC's latest outlook than in the EIA update. In OPEC's case, the revised 2026 African demand level stands more than 7% above its January 2025 projection, while the EIA revision is approximately 3% higher.

Revisions for major Asian consumers move in different directions across agencies. OPEC lowers its 2026 demand projections for both China and India relative to its previous outlook, whereas the EIA revises its estimates upward for China but downward for Ind ia over the same comparison period. The EIA also raises its 2026 demand estimate for the United States by roughly 2%.

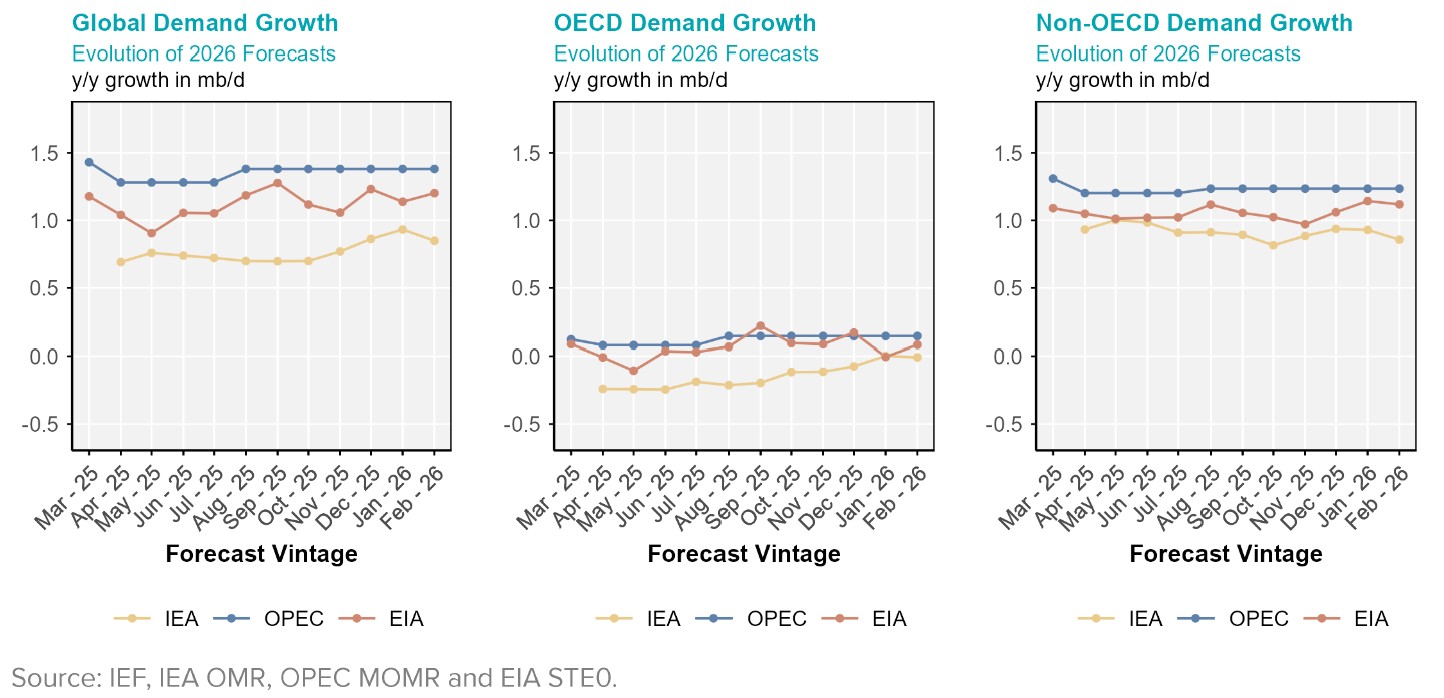

Evolution of 2026 Annual Demand-Supply Growth Forecasts

Global demand projections show notable differences across IEA, OPEC and EIA outlooks over the past year. The IEA projects year-on-year growth of about 0.8 mb/d, compared with 1.4 mb/d in OPEC's outlook and 1.2 mb/d in the EIA assessment. For OECD demand, the IEA shows no year-on-year change, while both OPEC and EIA indicate a modest increase of around 0.1 mb/d. Non-OECD demand displays a wider spread, at roughly 0.9 mb/d (IEA), 1.2 mb/d (OPEC) and 1.1 mb/d (EIA).

Non-OECD economies account for most of the projected demand growth. Within this group, China's demand increases by about 0.2 mb/d y/y across agency outlooks. India records larger gains, at roughly 0.3 mb/d in EIA projections and around 0.17 mb/d in the IEA outlook. African demand also rises, with increases of about 0.2 mb/d in EIA estimates, 0.16 mb/d in OPEC projections and roughly 0.13 mb/d in IEA figures.

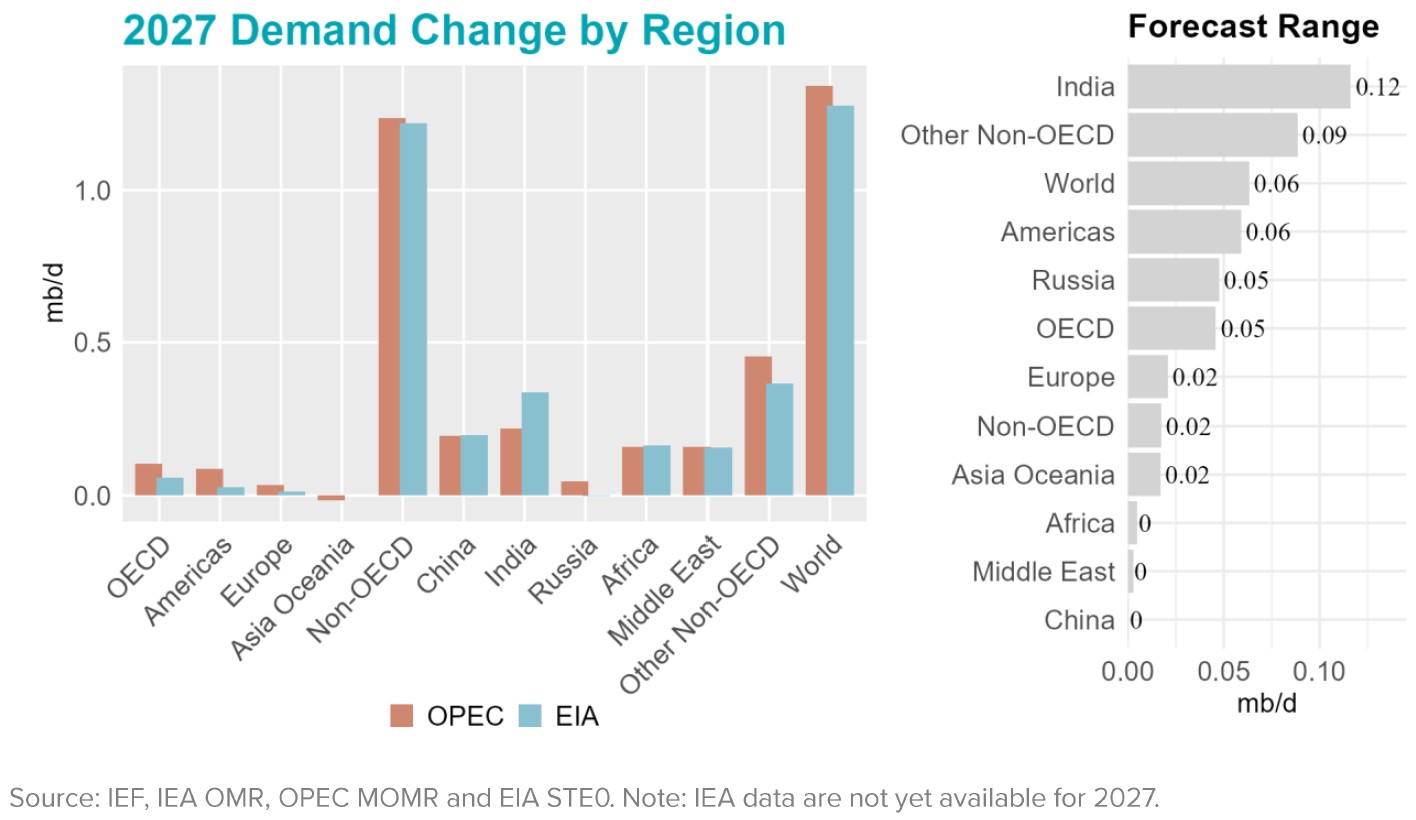

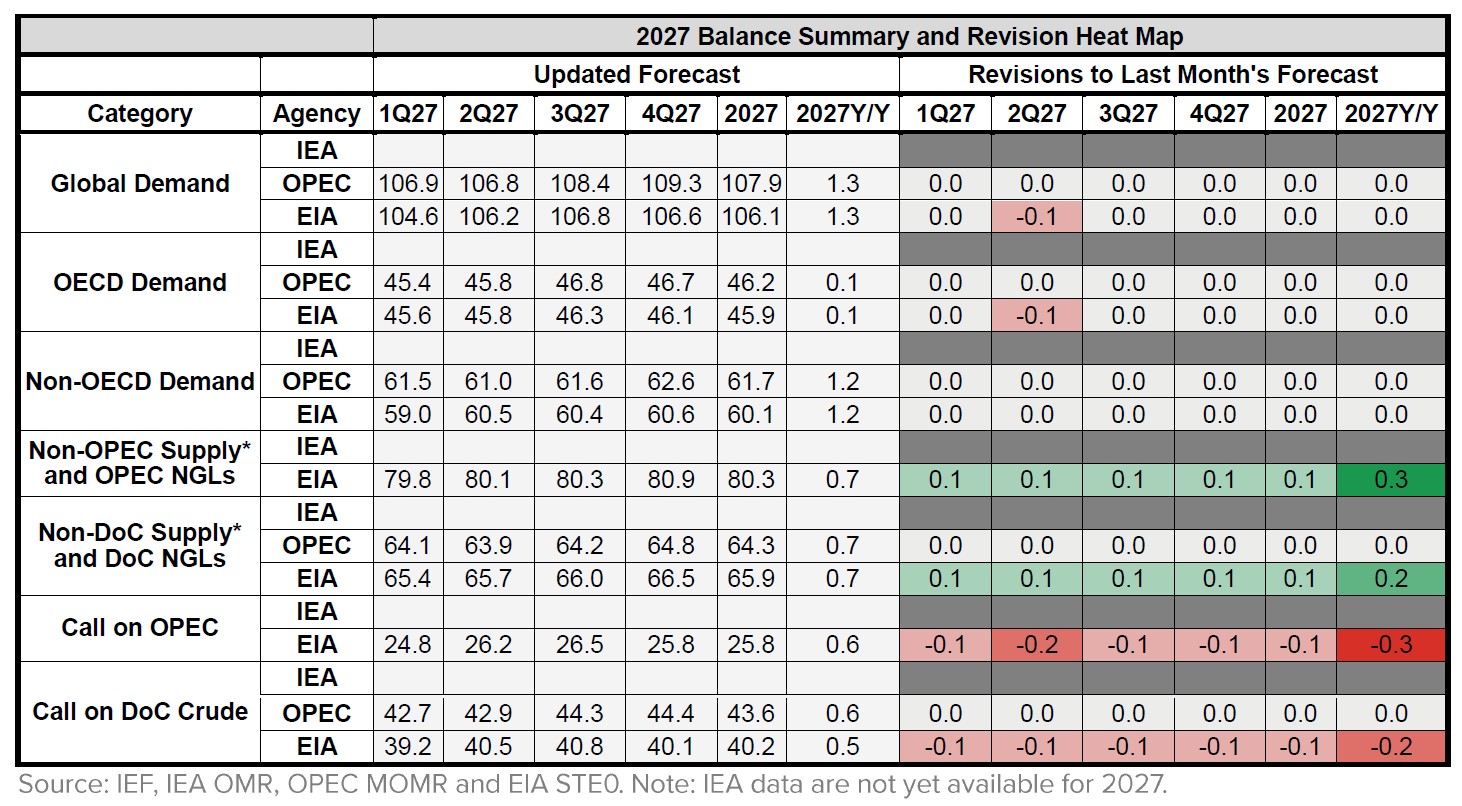

2027 Outlook Comparison

Outlook comparisons for 2027 indicate similar global oil demand growth rates across agencies. Both OPEC and EIA project year-on-year demand growth of about 1.3 mb/d, even though their total demand estimates differ by more than 1 mb/d. The regional breakdow n shows a similar pattern: non-OECD demand increases by roughly 1.2 mb/d in both outlooks, whereas OECD demand expands by around 0.1 mb/d.

Supply projections are also broadly aligned. OPEC and EIA each project non-DoC liquids supply and DoC NGLs to increase by approximately 0.7 mb/d in 2027, reaching averages of about 64.3 mb/d and 65.9 mb/d, respectively.

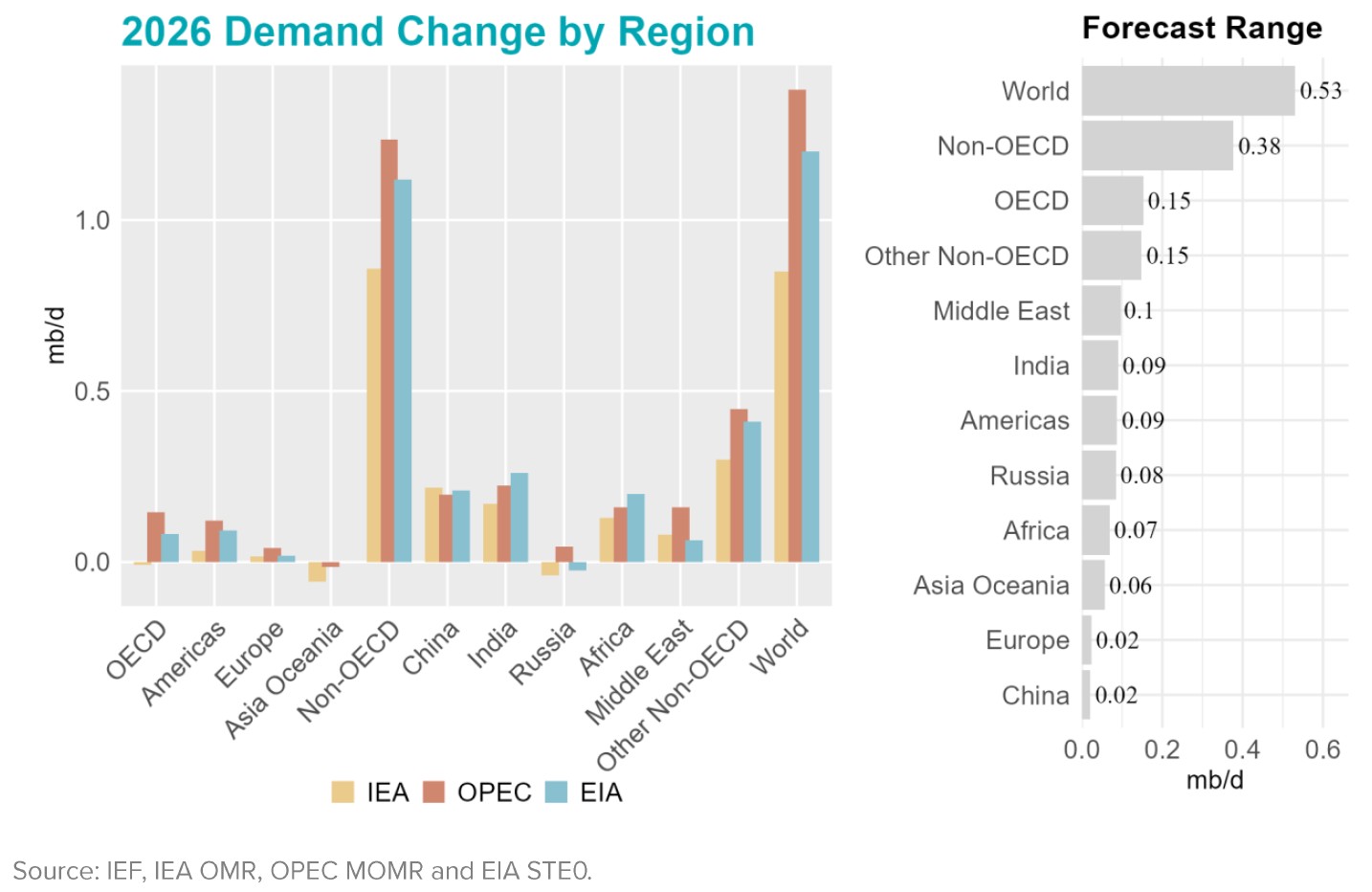

Country and regional analysis identifies India as a key driver of demand growth, with increases of about 0.3 mb/d y/y in EIA estimates and 0.2 mb/d in OPEC projections. China's demand growth is more moderate, at roughly 0.2 mb/d in both outlooks. Africa also contributes to the increase, with EIA and OPEC each projecting gains of around 0.16 mb/d. By contrast, OECD demand expands only marginally, by approximately 0.1 mb/d.