")

Comparative Analysis of Monthly Reports on the Oil Market

Friday 13 March 2026

Summary

Uncertainty continues to shape the global outlook for liquid supply and demand, amid tensions in the Middle East and releases from strategic reserves.

Demand

OPEC: OPEC leaves its global oil demand growth projections unchanged, at 1.4 mb/d year-on-year in 2026 and 1.3 mb/d in 2027, relative to last month’s estimate. Demand growth in OECD countries is led by the Americas and Europe, whereas non -OECD expansion is drive n primarily by India, China, and other Asian countries. Across regions, transportation fuels together with strong industrial, construction, and agricultural activity continue to support demand growth.

EIA: The US Energy Information Administration (EIA) maintains its projection of global liquid fuels consumption growth at around 1.2 mb/d year -on-year in 2026, rising further to approximately 1.4 mb/d in 2027, driven by demand growth in both OECD and non -OECD c ountries. Within the OECD, demand remains broadly flat in 2026 at approximately 45.9 mb/d, before increasing by about 0.2 mb/d year-ony-ear in 2027. By contrast, non -OECD demand accounts for the bulk of growth, expanding by around 1.2 mb/d in 2026 and a further ~1.3 mb/d in 2027.

IEA: The IEA estimates global oil demand growth at around 0.64 mb/d, revised downward by about 0.2 mb/d from last month’s outlook due to flight cancellations in the Middle East and disruptions to LPG supply. The projected increase is lower than last year’s grow th. Non-OECD countries account for all demand growth, led by China with approximately 0.2 mb/d year-on-year expansion.

Agency outlooks show a gap of about 0.8 mb/d year -on-year in global demand growth projections for 2026, while the difference between OPEC and EIA narrows to around 0.1 mb/d in 2027, no IEA projection is available for that year.

Supply

OPEC: Non-DoC liquids production is projected to increase by approximately 0.6 mb/d to reach 54.8 mb/d in 2026, with growth driven primarily by Brazil, Canada, the US, and Argentina. This growth trend is expected to continue into 2027, with non -DoC liquids productio n forecasted to grow by another 0.6 mb/d to average 55.4 mb/d, led by Brazil, Canada, Qatar, and Argentina.

EIA: The EIA sees non -OPEC supply and OPEC NGLs rising by 0.1 mb/d year-on-year in 2026 relative to last month’s assessment, bringing total growth to around 1.4 mb/d year-on-year. The EIA projects an additional 1.5 mb/d increase in 2027, representing an upward revision of 0.7 mb/d compared with last month’s estimates. The EIA keeps US crude oil production unchanged for 2026 at 13.6 mb/d, while revising its 2027 projection upward to 13.8 mb/d, 0.5 mb/d higher than last month’s estimate of 13.3 mb/d.

IEA: The IEA sees global oil supply rising by an average of around 1.1 mb/d in 2026. The IEA projects non-OPEC supply and OPEC NGLs to grow by about 1.1 mb/d year-on-year in 2026, 0.3 mb/d lower than last month’s estimate, reflecting large declines in the first two quarters of the year. Similarly, the IEA expects non-DoC supply and DoC NGLs to increase by around 1.2 mb/d year -on-year, 0.2 mb/d lower than last month’s outlook.

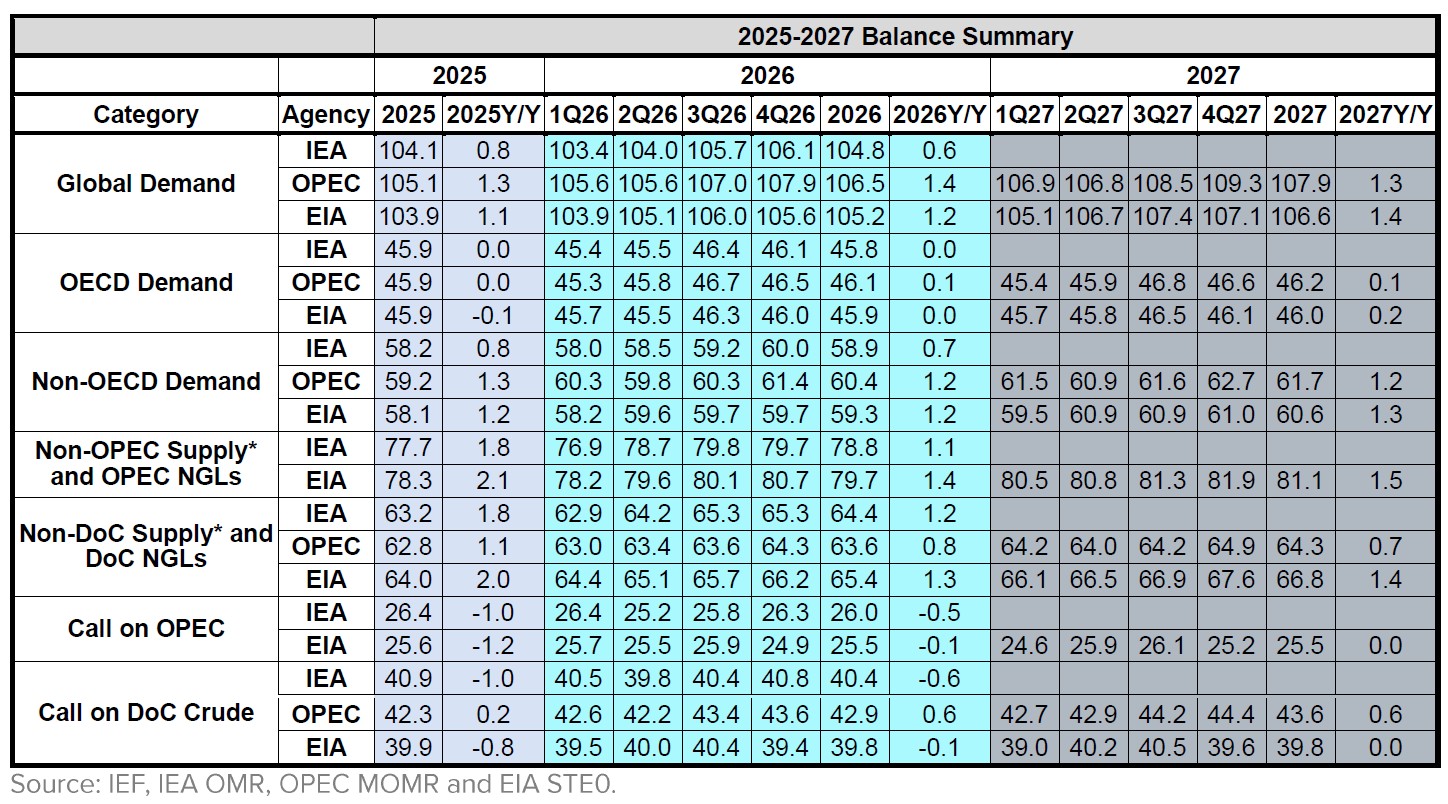

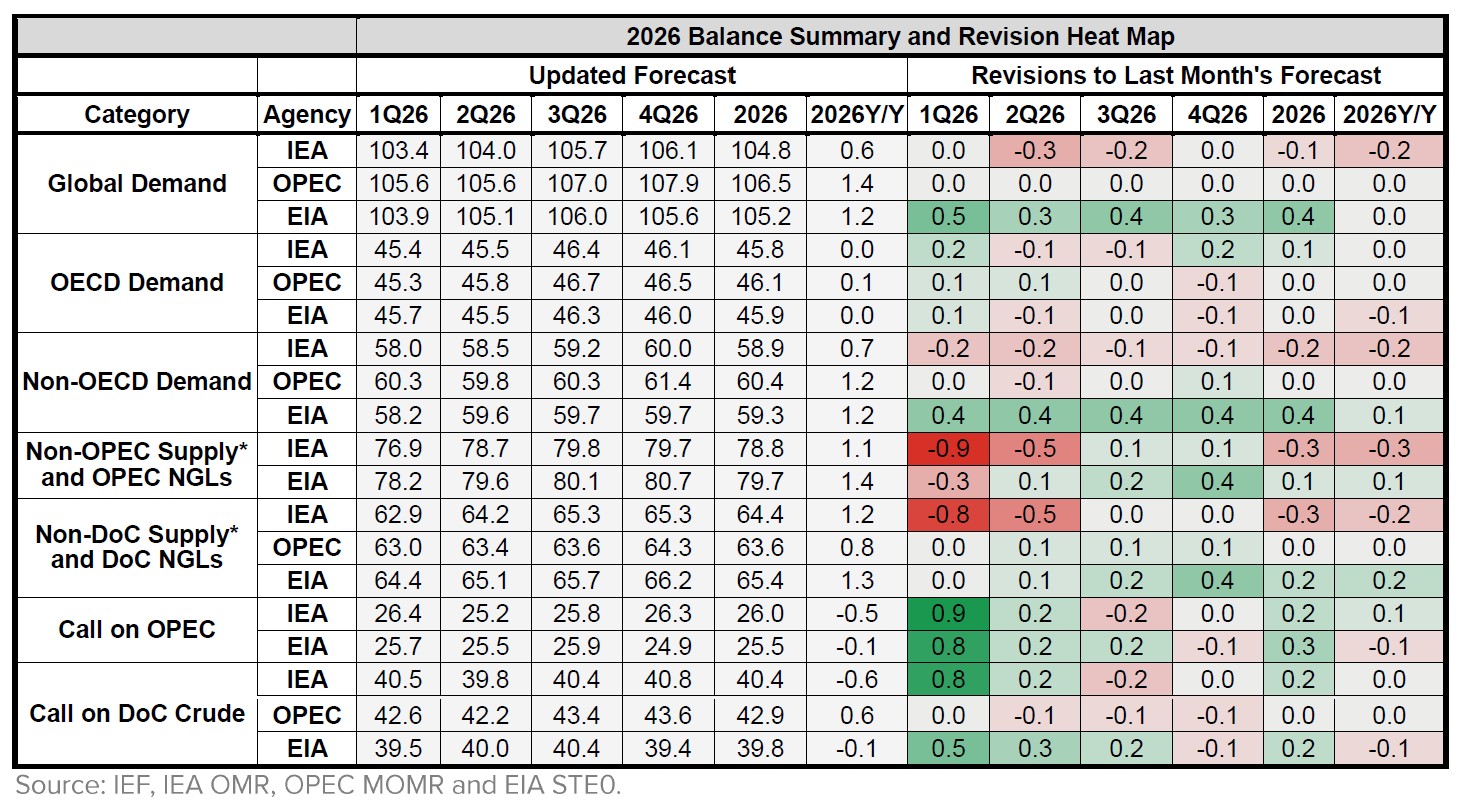

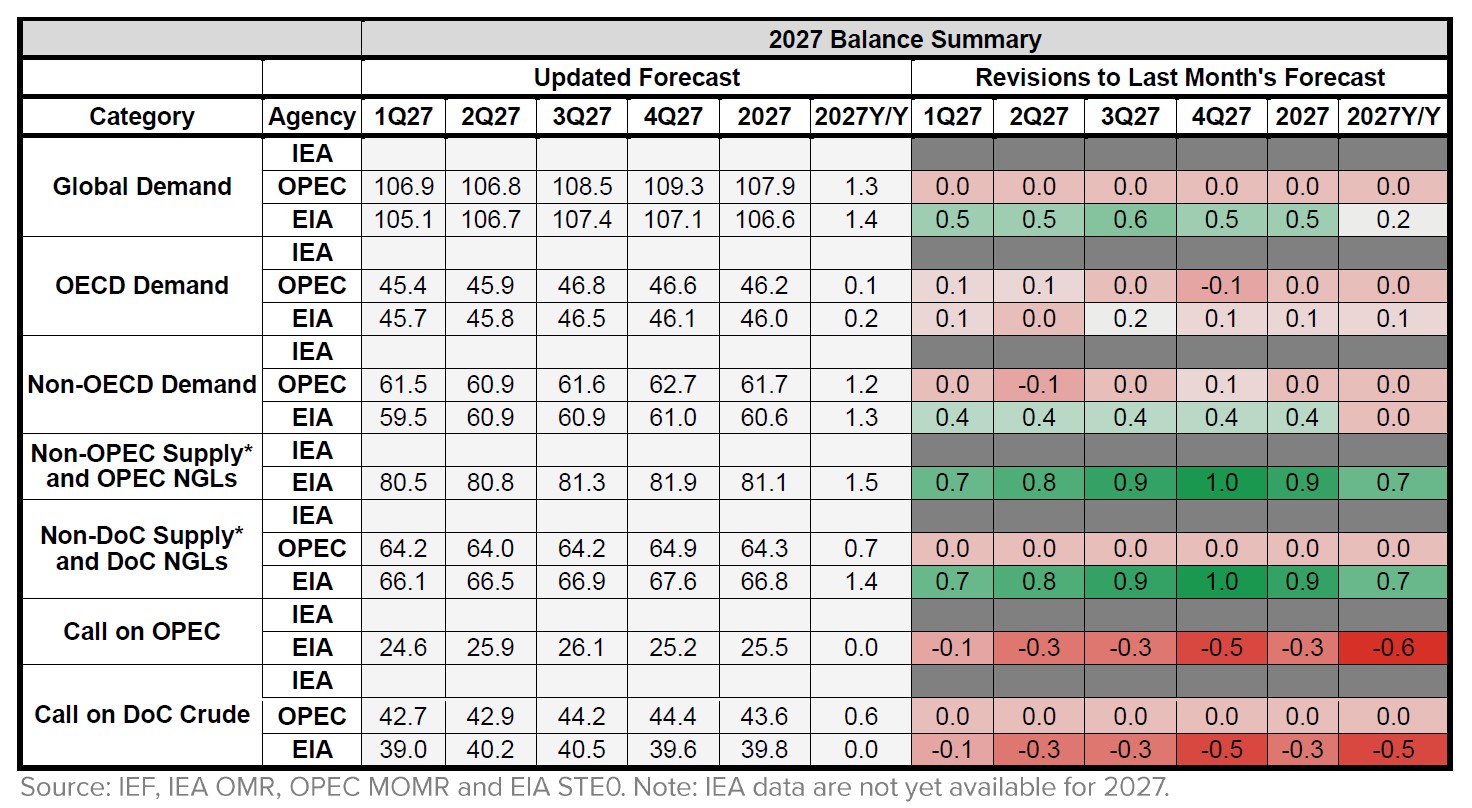

2025-2027 Balance Summary

Global oil demand estimates for 2026 range from 104.8 mb/d (IEA) to 106.5 mb/d (OPEC), with EIA at 105.2 mb/d, implying a 1.7 mb/d gap between OPEC and IEA. OECD demand growth remains broadly aligned across agencies, while non-OECD demand growth is consistently higher in the OPEC and EIA outlooks. On the supply side, the EIA and IEA project stronger growth in non -DoC supply and DoC NGLs than OPEC, with estimates of about 1.3 mb/d, 1.2 mb/d, and 0.8 mb/d, respectively.

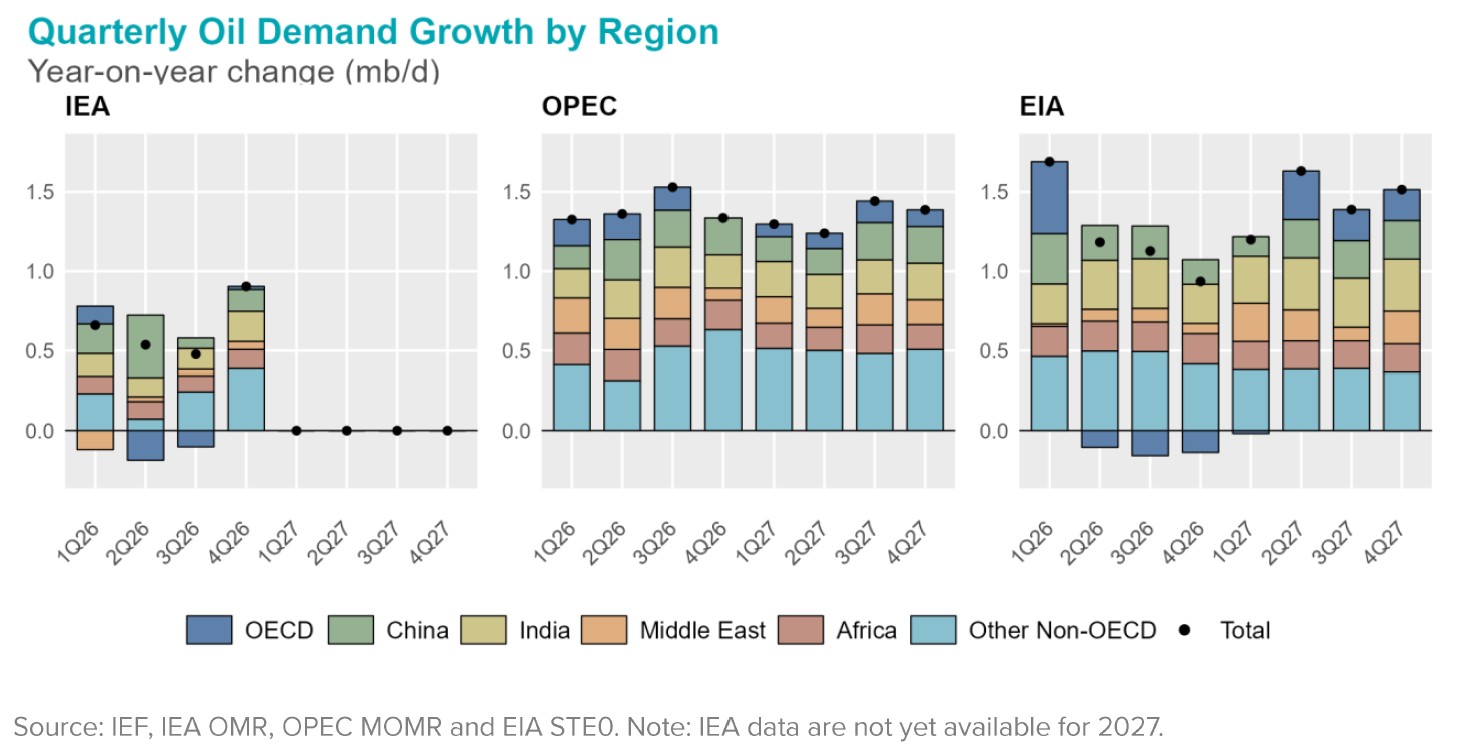

Across 1Q26–4Q26, OPEC generally reports the highest quarterly global oil demand growth estimates, while EIA projections indicate stronger growth during 1Q27 –4Q27. On average, OPEC projects higher oil demand growth in the Middle East in 2026, whereas the E IA projects stronger demand growth in India and the Middle East than OPEC in 2027.

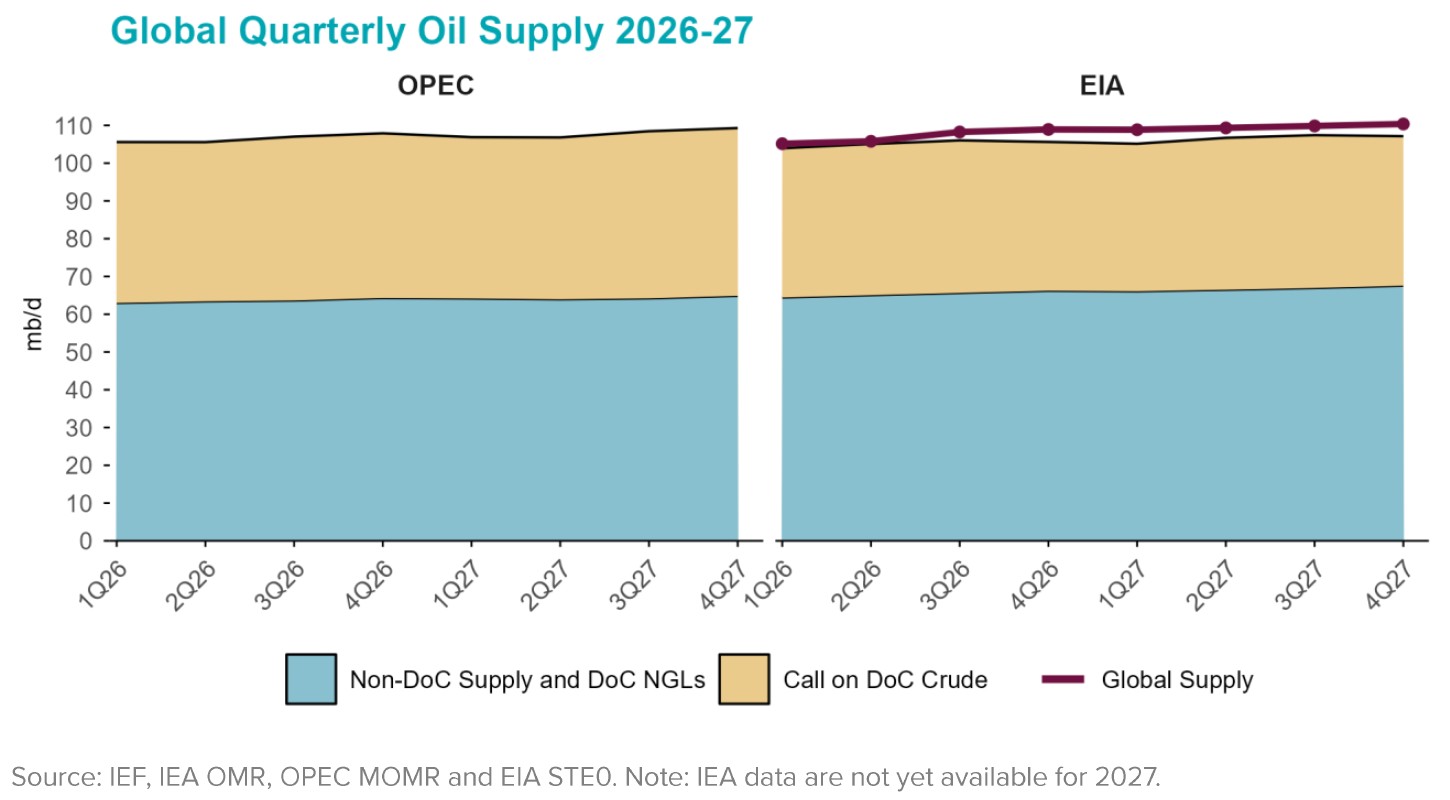

In 1Q26, the EIA projects non-DoC supply and DoC NGLs at 64.4 mb/d, compared with 63 mb/d in OPEC’s estimate, and this gap persists throughout the forecast horizon, reaching 67.6 mb/d in 4Q27 versus 64.9 mb/d in OPEC’s outlook.

2026 Outlook Comparison

Global demand projections for 2026 diverge across agencies, with the EIA forecasting growth of about 1.2 mb/d year-on-year, roughly double the IEA projection of 0.6 mb/d, while OPEC projects even stronger growth at 1.4 mb/d. OECD demand remains broadly sta ble across outlooks, while differences are largely driven by non-OECD estimates, where EIA and OPEC project similar growth of around 1.2 mb/d, about 0.5 mb/d higher than the IEA estimate.

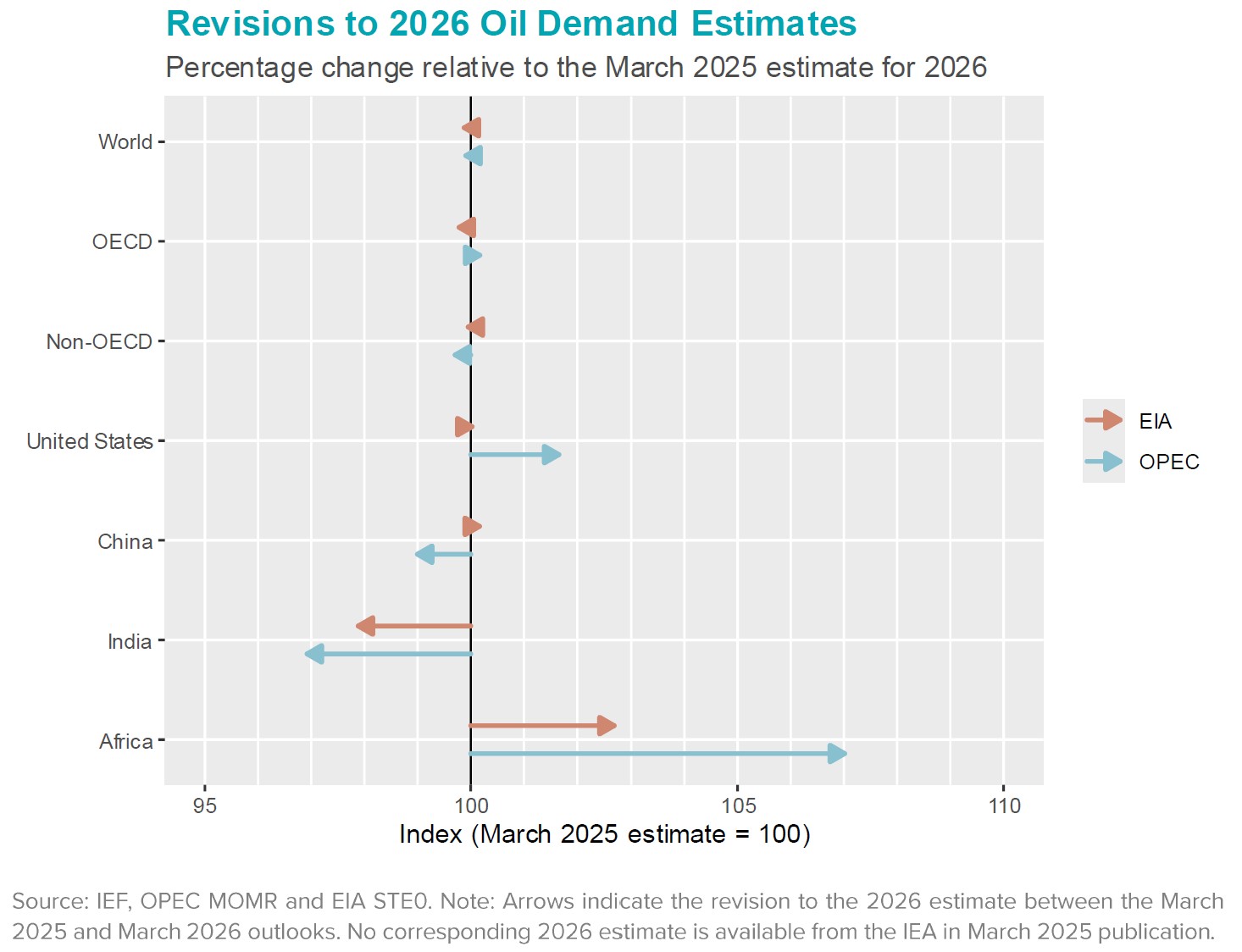

Recent outlook updates show only modest changes to global oil demand in 2026, with world, OECD, and non -OECD aggregates remaining broadly consistent with earlier projections. Revisions are more evident at the regional level, particularly for Africa, where both agencies raise their 2026 demand estimates, although OPEC introduces the larger adjustment. In OPEC’s outlook, African demand is about 7% higher than its March 2025 projection, compared with around 3% in the EIA revision.

For major Asian consumers, revisions move in different directions: OPEC lowers its 2026 demand projections for China and India, while the EIA maintains its estimate for China but reduces its projection for India. The EIA also raises its 2026 demand estimat e for the United States by about 2%.

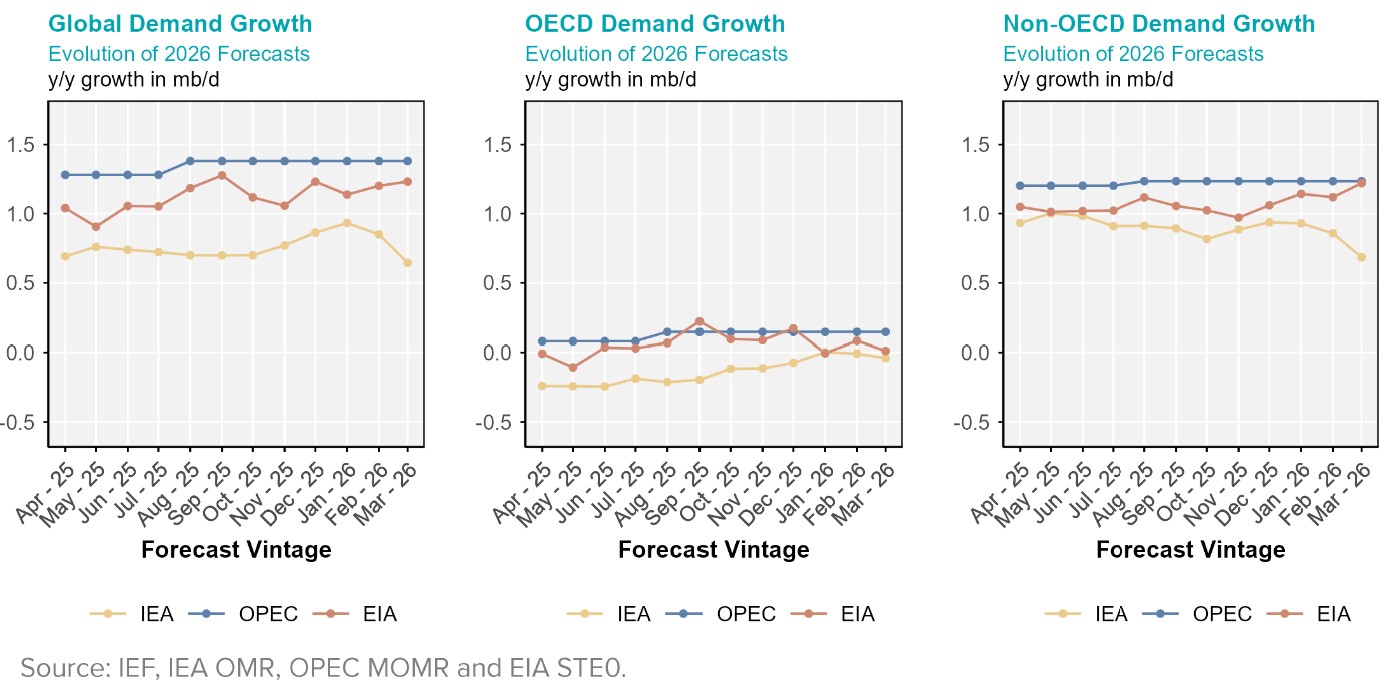

Evolution of 2026 Annual Demand-Supply Growth Forecasts

Global demand projections for 2026 have evolved differently across agencies over the past year. The IEA’s latest estimate remains broadly similar to its projection a year ago, at around 0.6 mb/d year-onyear, despite downward revisions over the past two mo nths, while the EIA and OPEC have gradually revised their projections upward compared with last year’s estimates

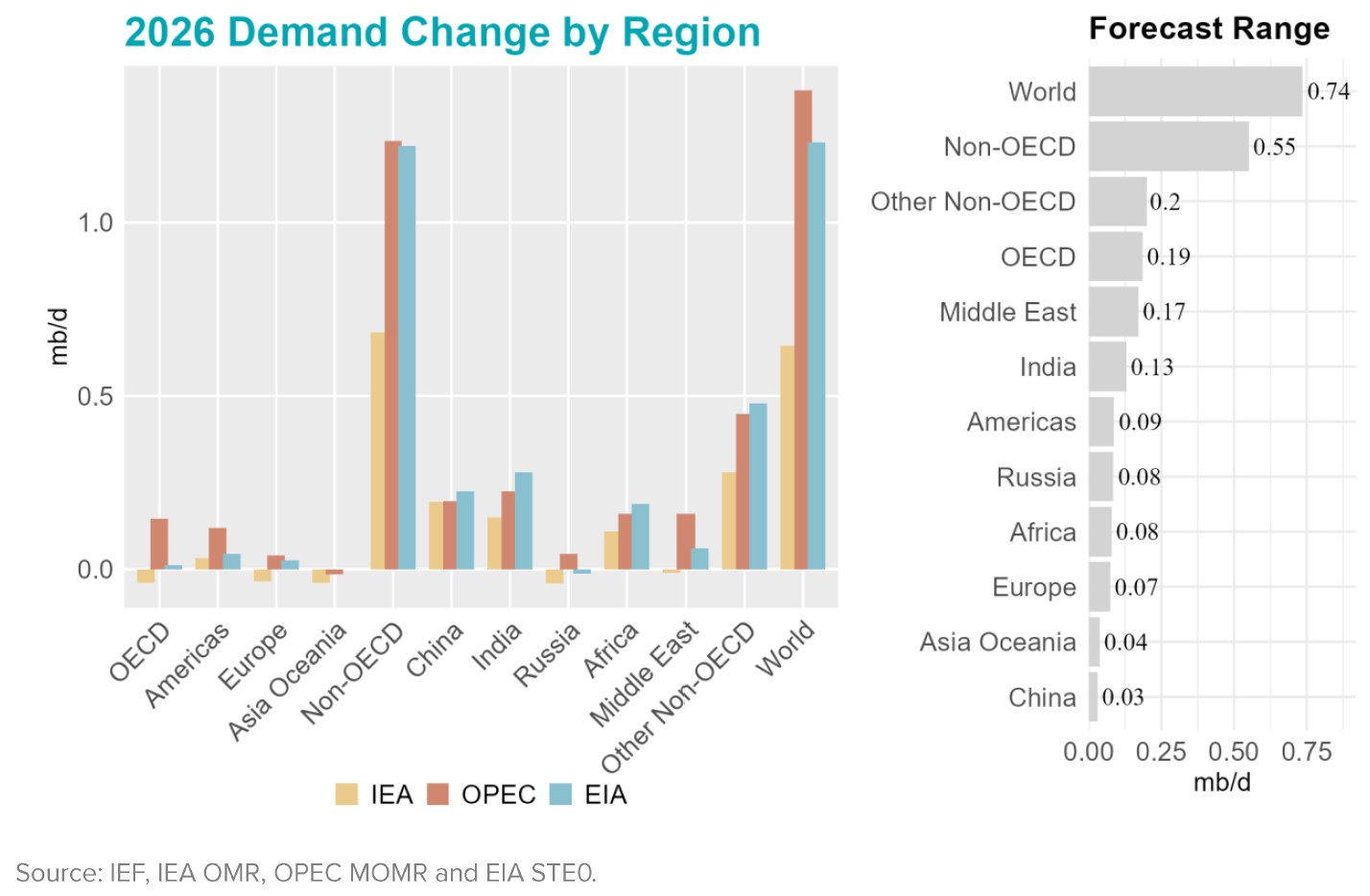

Global oil demand is projected to increase in 2026, with EIA forecasting growth of 1.23 mb/d, OPEC 1.38 mb/d, and IEA 0.64 mb/d. Growth is driven mainly by non -OECD demand, rising by 1.22 mb/d in the EIA outlook, 1.24 mb/d in OPEC’s projection, and 0.68 mb /d in the IEA estimate. China, India, and Africa account for much of this increase, while OECD demand remains broadly flat across outlooks , with only modest growth projected by OPEC.

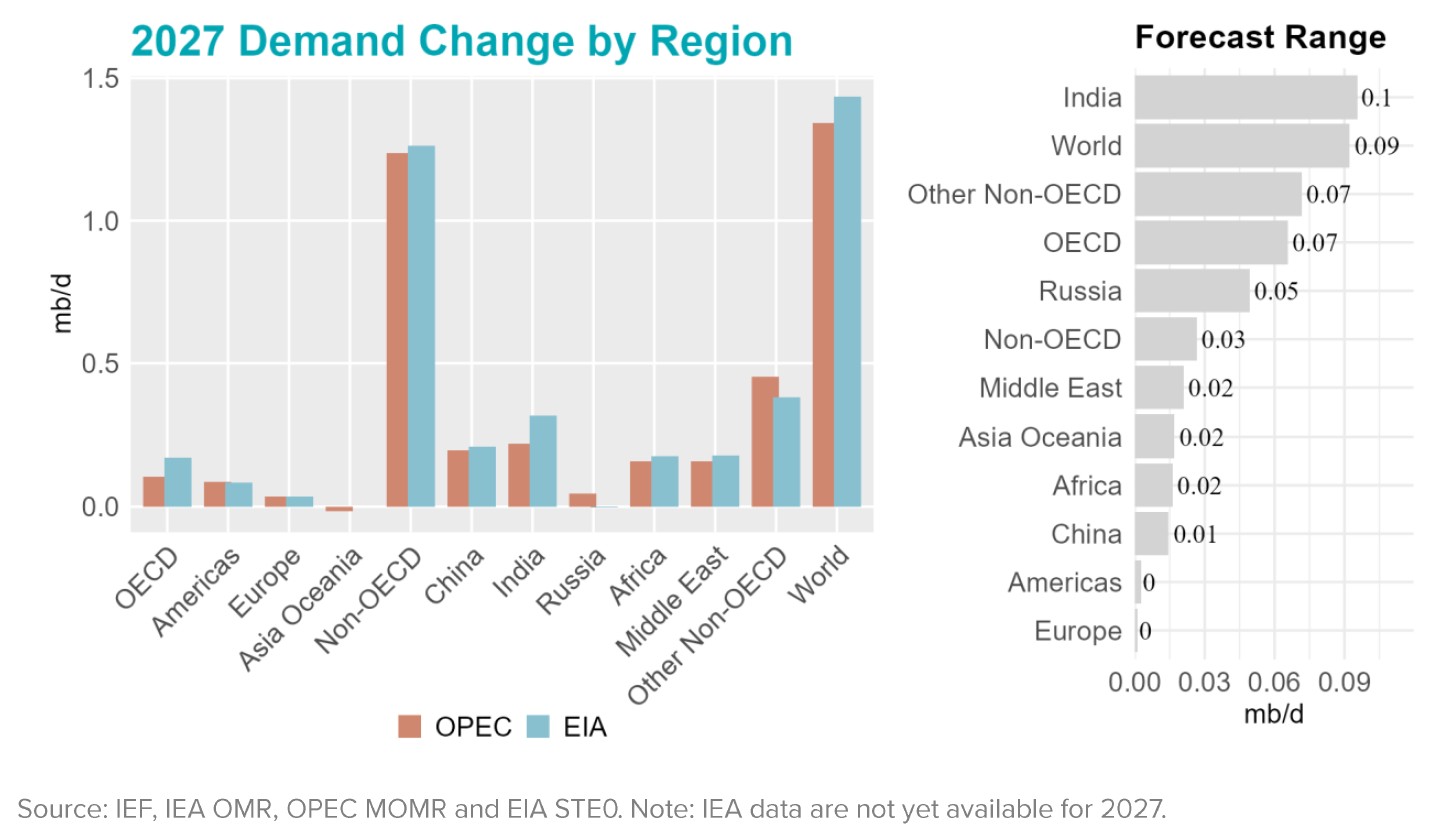

2027 Outlook Comparison

Projections for 2027 indicate greater convergence in global oil demand growth across agencies. The EIA projects year-on-year demand growth of around 1.4 mb/d, compared with about 1.3 mb/d in OPEC’s outlook. Regional demand patterns are also similar, with n on-OECD demand rising by roughly 1.2 mb/d, while the EIA places OECD demand slightly higher than OPEC by around 0.1 mb/d.

On the supply side, the EIA projects almost double the growth estimated by OPEC for non-DoC supply and DoC NGLs in 2027, with EIA estimating 1.4 mb/d year-on-year compared with OPEC’s projection of 0.7 mb/d.

Regional projections highlight India as a major contributor to global oil demand growth, with increases of about 0.32 mb/d year-on-year in the EIA outlook and 0.22 mb/d in OPEC’s projection. China’s demand growth remains steady at around 0.2 mb/d in both o utlooks, while Africa also contributes to the expansion, with both agencies projecting gains close to 0.2 mb/d. By contrast, OECD demand shows only modest increases, with EIA projecting growth of around 0.2 mb/d and OPEC about 0.1 mb/d.