")

Comparative Analysis of Monthly Reports on the Oil Market

Wednesday 15 April 2026

Summary

Force majeure and held up volumes in the Gulf increase uncertainty in global oil markets . Global oil demand and supply growth projections now vary more widely, with a spread of about 1.5 mb/d year-onyear across agencies for 2026 demand.

Demand

OPEC: OPEC maintains its projections for global oil demand growth at 1.4 mb/d in 2026 and 1.3 mb/d in 2027, unchanged from last month’s assessment. Demand growth is primarily driven by non-OECD countries, led by China, India and Other Asian countries. Across products, jet/kerosene consumption increases by 0.1 mb/d year-on-year in 2Q26, accelerating to 0.4 mb/d in 3Q26 and 0.5 mb/d in 4Q26. Gasoline and diesel demand also rise over the full year, by around 0.4 mb/d and 0.2 mb/d, respectively.

EIA: The US EIA revises its estimate of global oil demand growth for 2026 downward to around 0.6 mb/d year-on-year, approximately half of last month’s projection. The revision reflects a moderation in contributions from both OECD and non-OECD economies, with OECD demand contracting by about 0.3 mb/d and non-OECD growth reduced to around 0.9 mb/d y/y. Looking ahead, the EIA projects a stronger expansion in 2027, with global demand increasing by 1.6 mb/d to reach 106.2 mb/d, around 0.2 mb/d higher than previously assessed.

IEA: The IEA revises its 2026 global oil demand growth downward to a contraction of around 0.1 mb/d year-on-year, a significant decline from last month’s estimate of more than 0.7 mb/d. The downward revision reflects flight cancellations in the Middle East, parts of Asia and Europe, alongside disruptions to LPG supply. The IEA expects non-OECD demand to increase by around 0.2 mb/d year -on-year, while OECD demand contracts by about 0.2 mb/d.

Supply

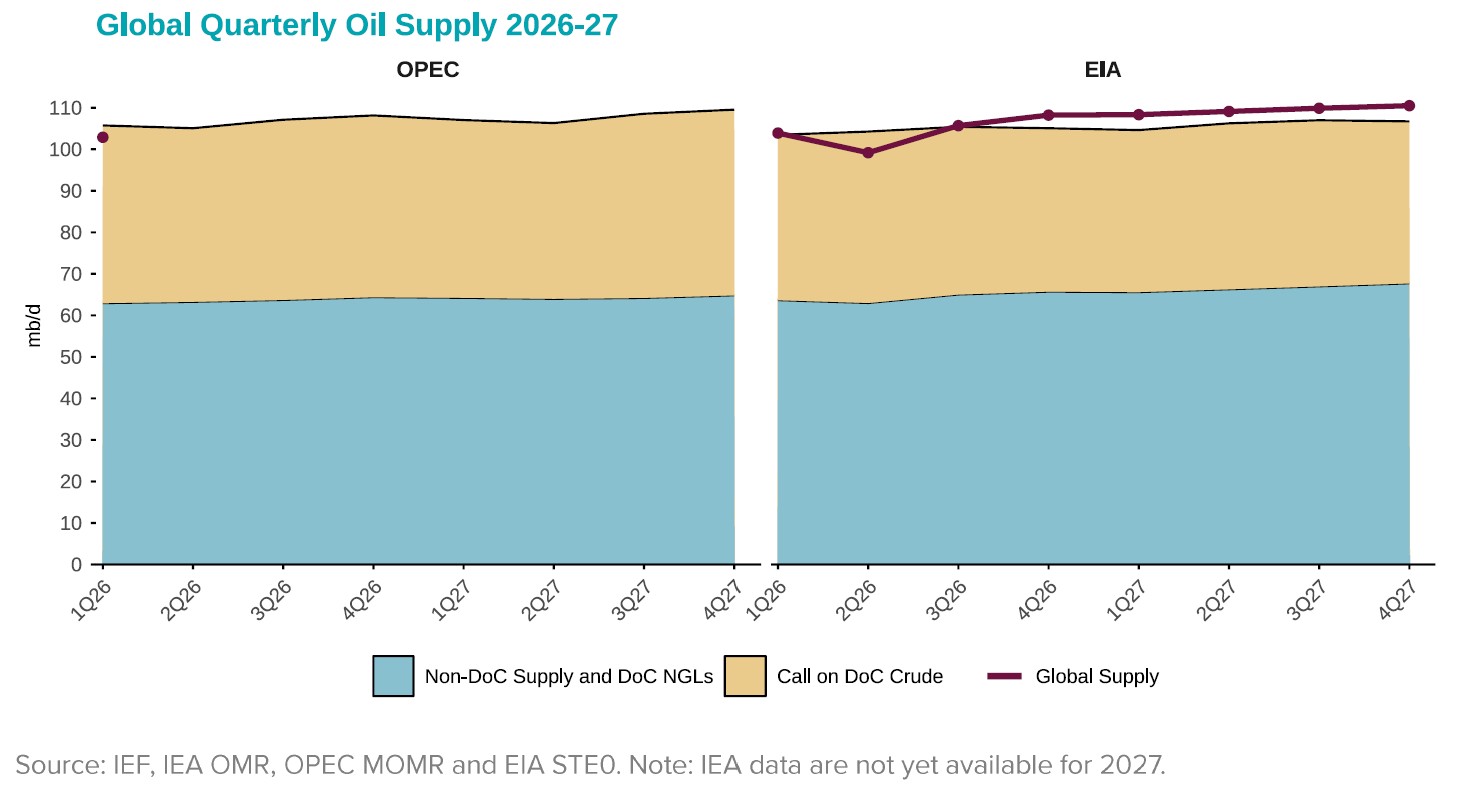

OPEC: OPEC projects non-DoC liquids supply and DoC NGLs to increase by around 0.8 mb/d, reaching 63.6 mb/d, with growth led by the United States, Canada, Brazil, and Argentina. This expansion continues into 2027, with supply rising by a further 0.7 mb/d to reach 64.3 mb/d, supported by Qatar, Canada, Brazil, and Argentina.

EIA: The EIA revises its estimate of non-DoC supply and DoC NGLs growth downward to around 0.3 mb/d year-on-year in 2026, compared with approximately 1.4 mb/d in last month’s assessment. For 2027, it projects a stronger increase of about 2.3 mb/d, representing an upward revision of 0.9 mb/d. The EIA also slightly lowers its projection for US crude oil production by 0.1 mb/d to 13.5 mb/d, while maintaining its 2027 forecast at 13.8 mb/d.

IEA: The IEA revises its estimate of non-DoC supply and DoC NGL growth to around 0.3 mb/d, a downward adjustment of about 0.9 mb/d from last month’s estimate, to reach 63.6 mb/d. The IEA reports that global oil supply declines sharply by 10.1 mb/d to 97 mb/d in March 2026, primarily driven by developments in the Middle East. At the same time, it projects non-OPEC supply and OPEC NGLs to increase by around 0.1 mb/d, representing a decline of more than 1 mb/d relative to last month’s outlook.

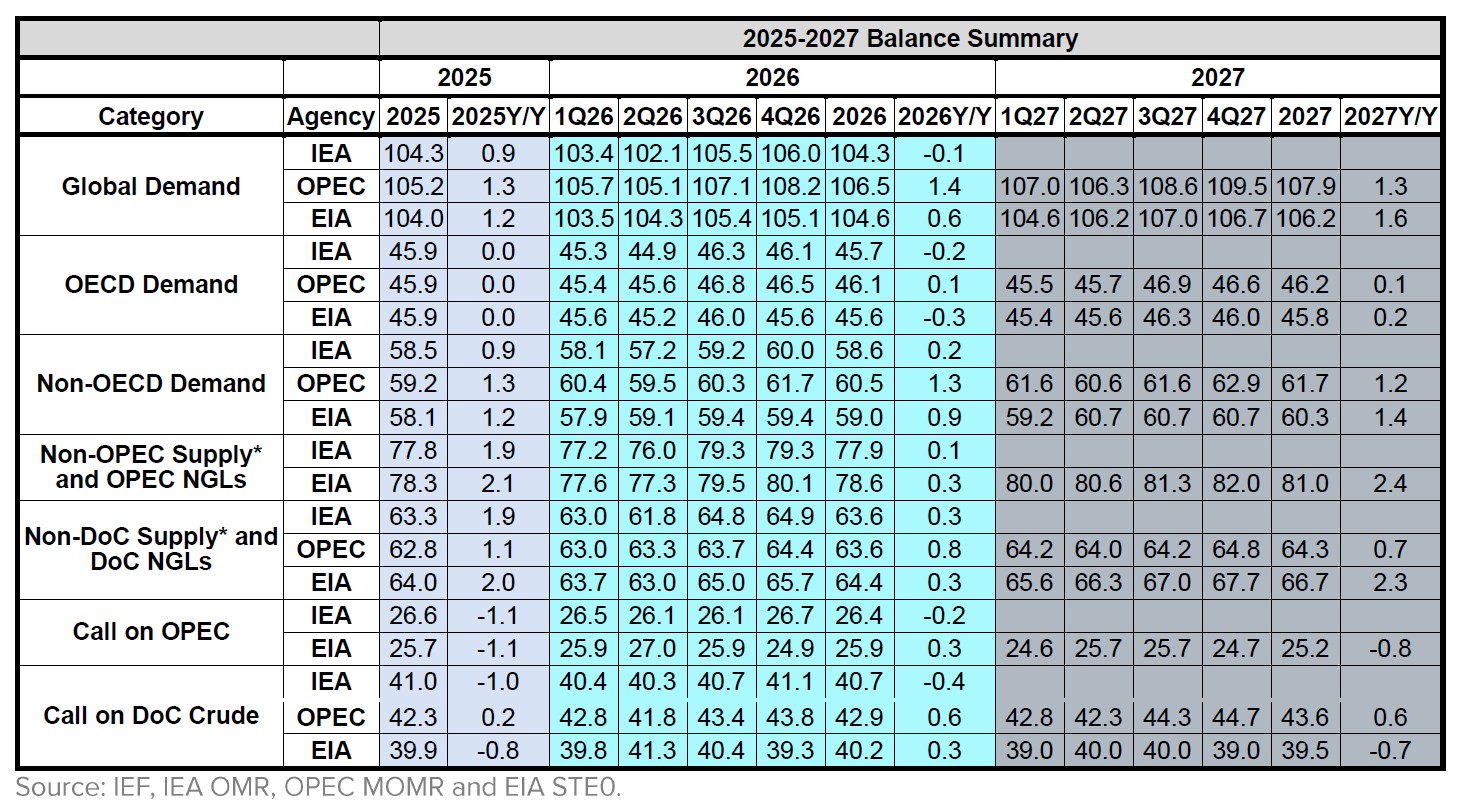

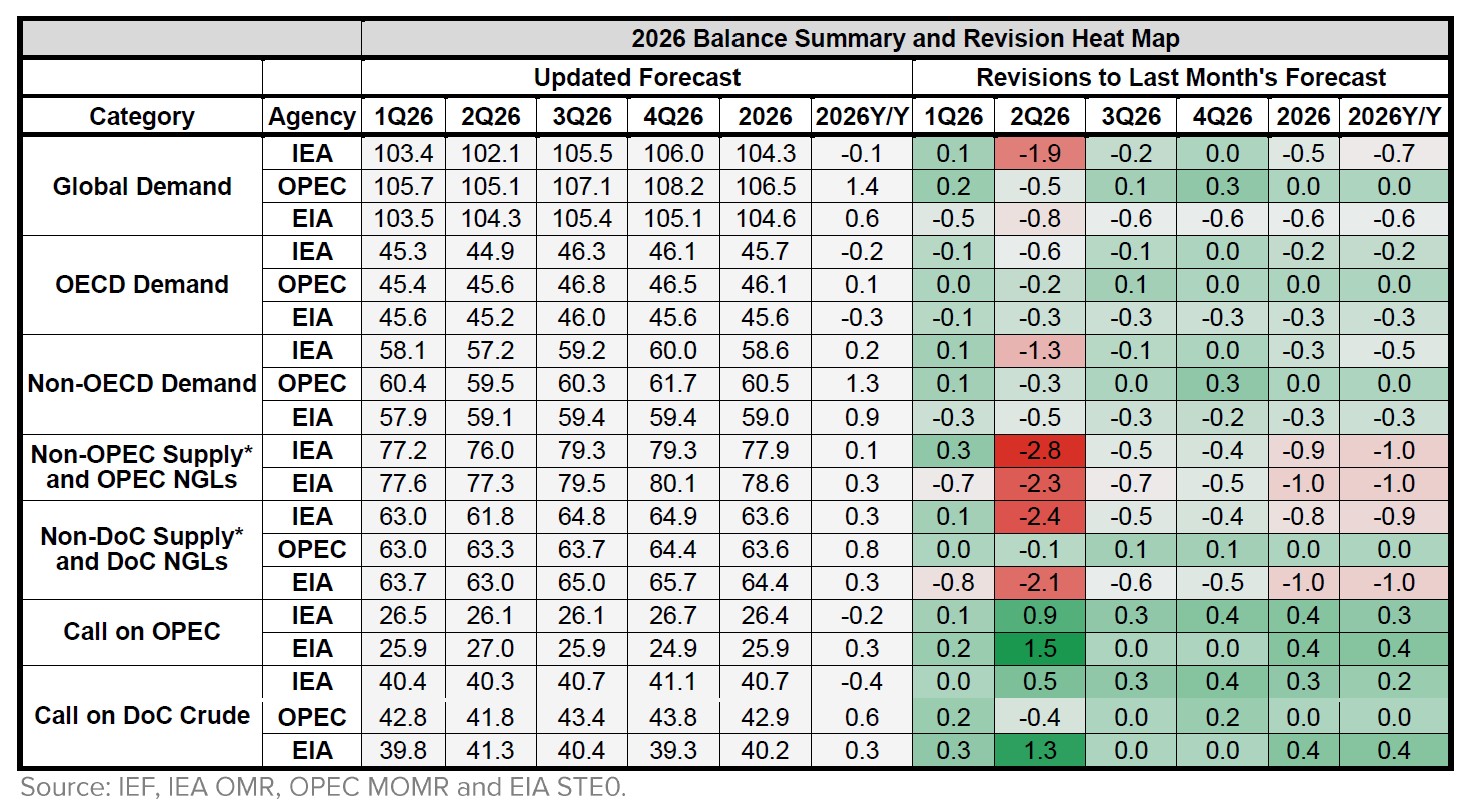

2025-2027 Balance Summary

In 2026, global demand estimates for oil show a range of 104.3 mb/d from the IEA, 104.6 mb/d from the EIA, and 106.5 mb/d from OPEC, indicating a spread of 2.2 mb/d between the lowest and highest projections. On the supply side, OPEC projects non-DoC supply and DoC NGLs to grow by around 0.8 mb/d year-on-year, approximately 0.5 mb/d higher than EIA and IEA estimates.

Quarterly global oil demand growth remains generally highest in OPEC’s projections over 1Q26–4Q26, while the EIA expects a stronger growth profile across 1Q27–4Q27. The IEA projects negative average growth in 2026, driven by declines in OECD and Middle Eas t demand, whereas the EIA expects Middle East demand to grow markedly in 2027.

The average level of non-DoC supply and DoC NGLs across the two agencies shows modest variation, with the EIA reporting 64.4 mb/d in 2026, compared with 63.6 mb/d in OPEC’s projections. This pattern persists in 2027, with the EIA projecting an increase to 66.7 mb/d, while OPEC estimates a lower level of 64.3 mb/d.

2026 Outlook Comparison

Global oil demand projections for 2026 diverge markedly across agencies. OPEC maintains its growth estimate at 1.4 mb/d year-on-year, while the EIA projects growth of around 0.6 mb/d year-on-year, roughly half of last month’s estimate, and the IEA projects a contraction. The spread in growth estimates across agencies exceeds 1.5 mb/d.

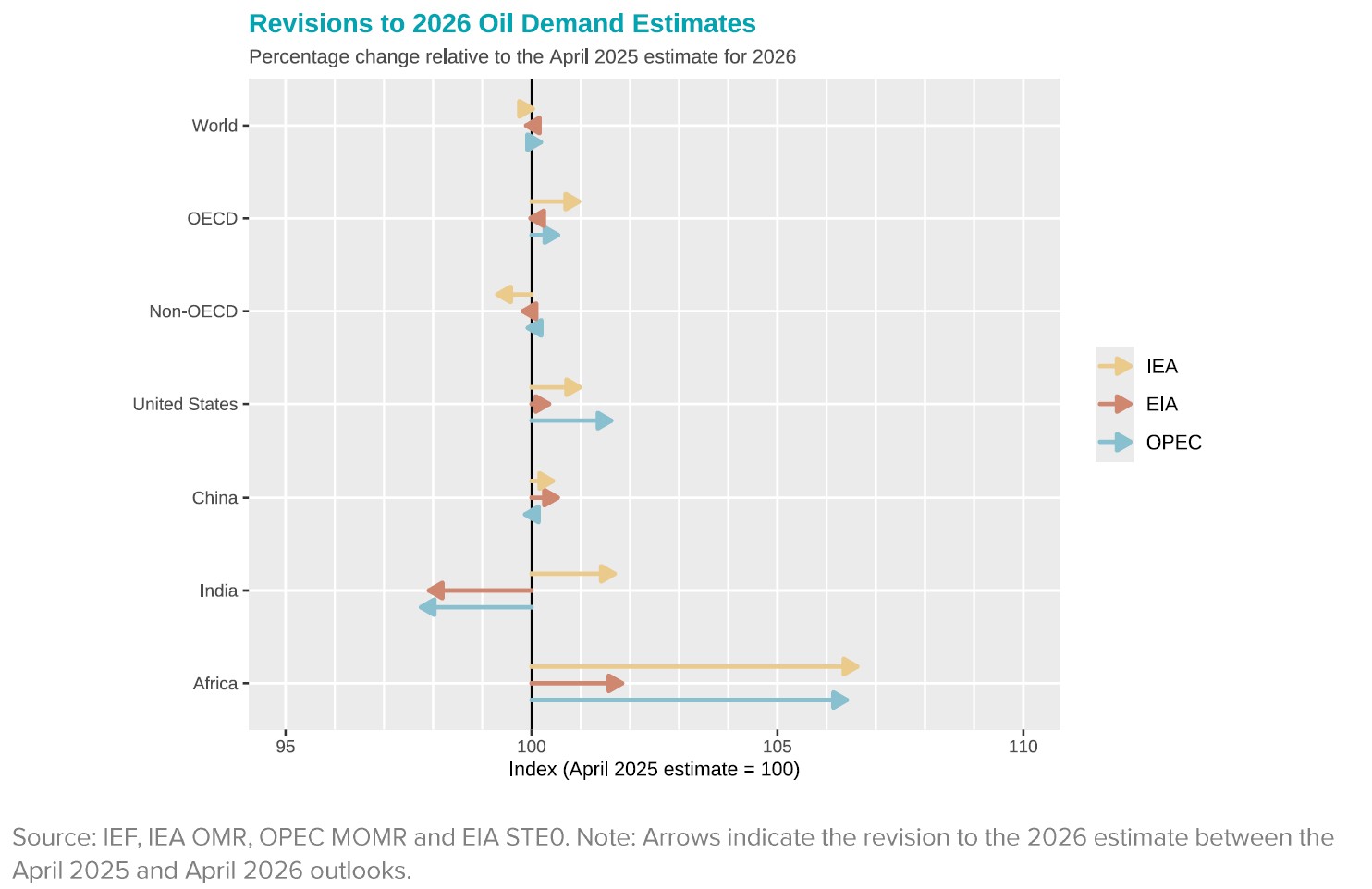

The latest revisions to 2026 oil demand estimates remain limited at the global level, with the world aggregate staying close to the April 2025 baseline across all three agencies. OECD and non-OECD revisions are also relatively modest, although the IEA rais es its OECD estimate and lowers its non-OECD projection more visibly than the EIA and OPEC. Changes become more evident at the regional level. Africa records the largest upward revision across all agencies, with the strongest increase in the IEA and OPEC outlooks (6% higher than its April 2025 projection). The United States is also revised upward in all three outlooks, particularly in OPEC’s projection. In Asia, revisions are mixed: China remains close to the baseline, with only minor upward adjustments in the IEA and EIA forecasts and a slight downward revision in OPEC assessments, while India shows the clearest divergence, with the IEA revising demand upward and both the EIA and OPEC lowering their estimates below the baseline.

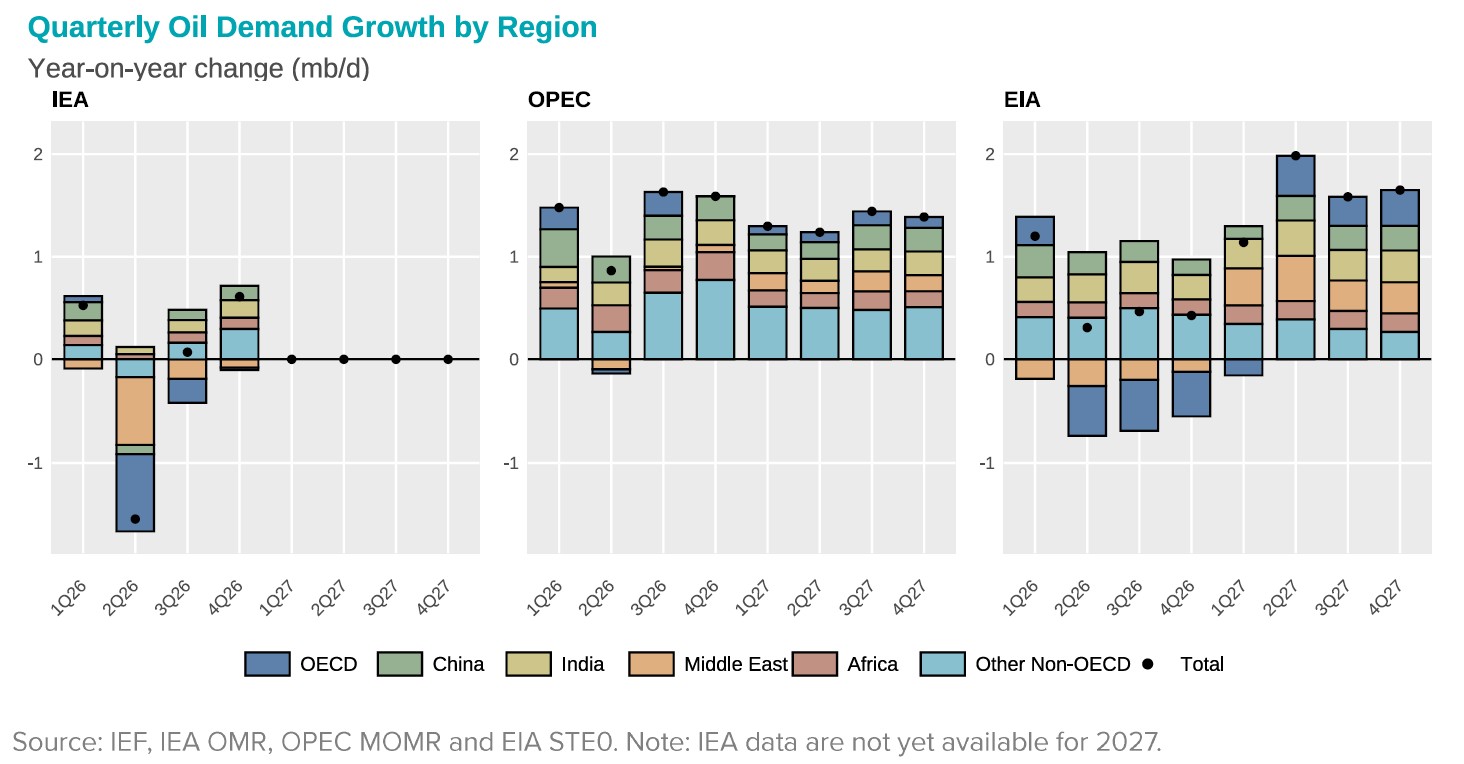

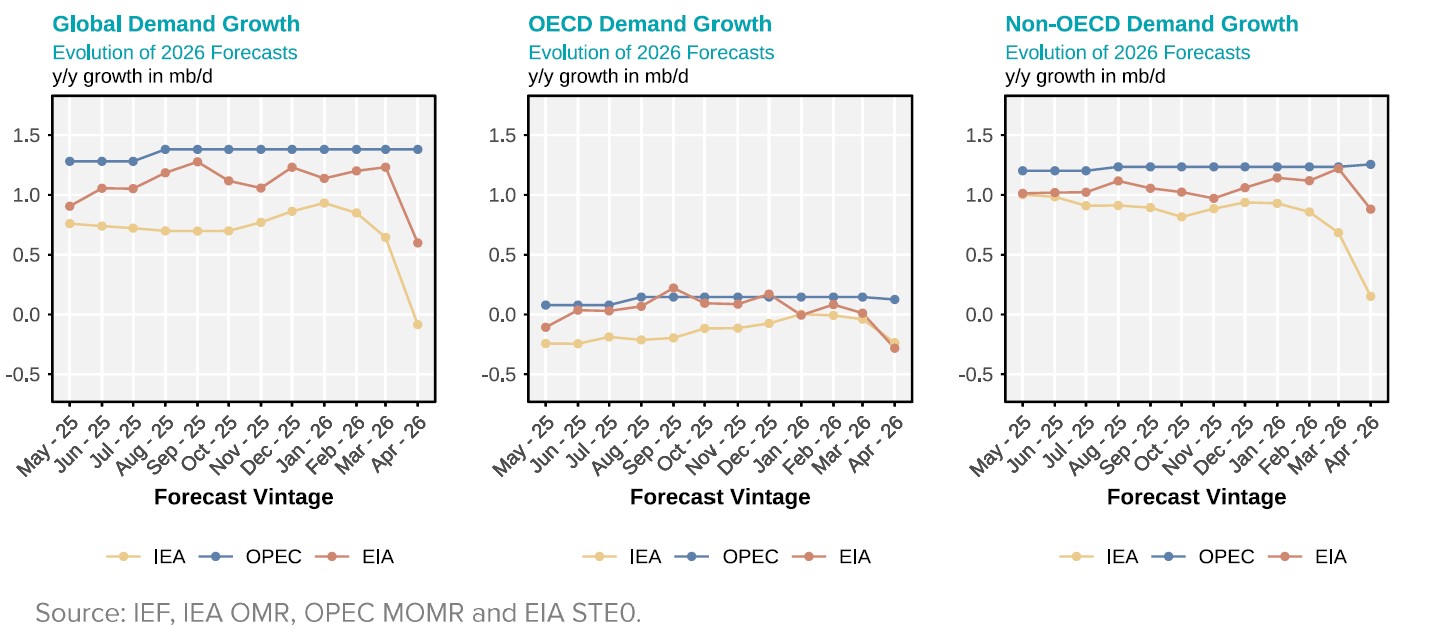

Evolution of 2026 Annual Demand-Supply Growth Forecasts

Global demand projections for 2026 have continued to widen over the past two outlooks, with the largest gap observed this month at more than 1.5 mb/d across agencies. In both the IEA and EIA outlooks, demand in OECD and non-OECD economies declines, with the contraction more significant in non-OECD regions.

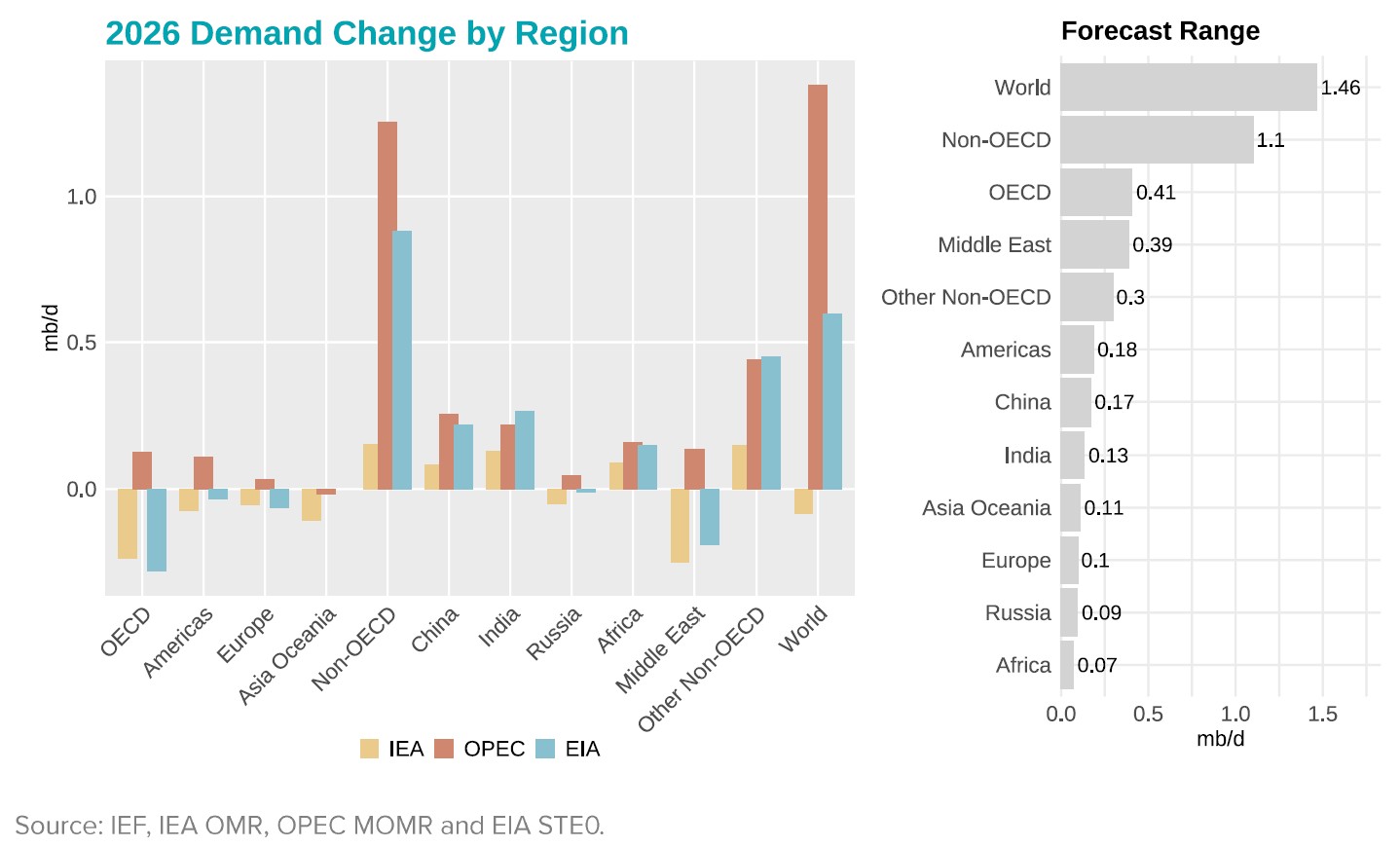

Across regions, global oil demand shows divergent trends in 2026. Non-OECD demand continues to expand, with the EIA estimating growth of 0.9 mb/d, the IEA around 0.2 mb/d, and OPEC about 1.3 mb/d. In contrast, OECD demand declines, with the EIA projecting a reduction of 0.3 mb/d, the IEA around 0.2 mb/d, and OPEC indicating marginal growth of about 0.1 mb/d. The EIA expects demand in India to rise by around 0.3 mb/d and in China by approximately 0.2 mb/d. Africa also contributes to growth, with an increase of about 0.15 mb/d in both the EIA and OPEC outlooks.

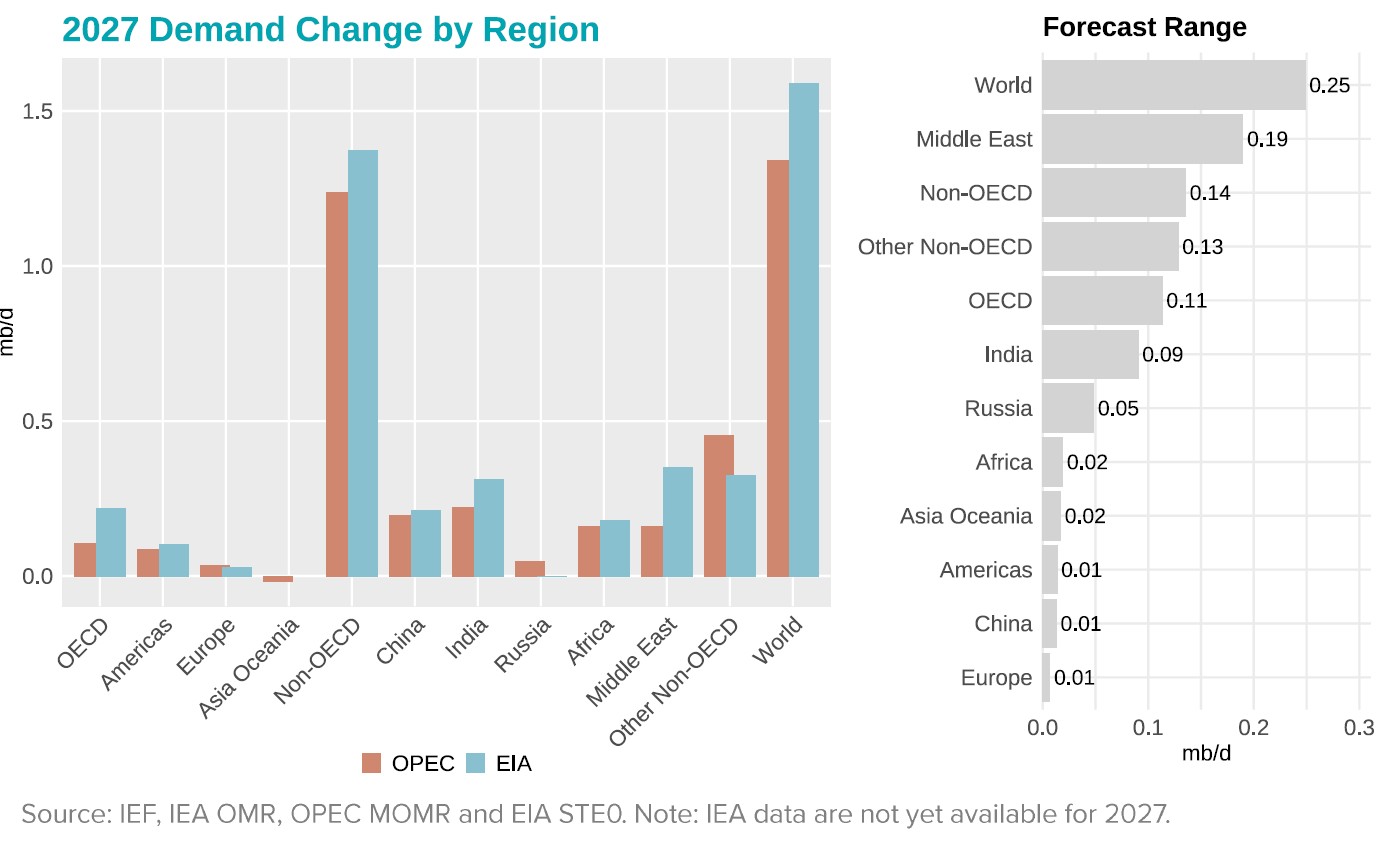

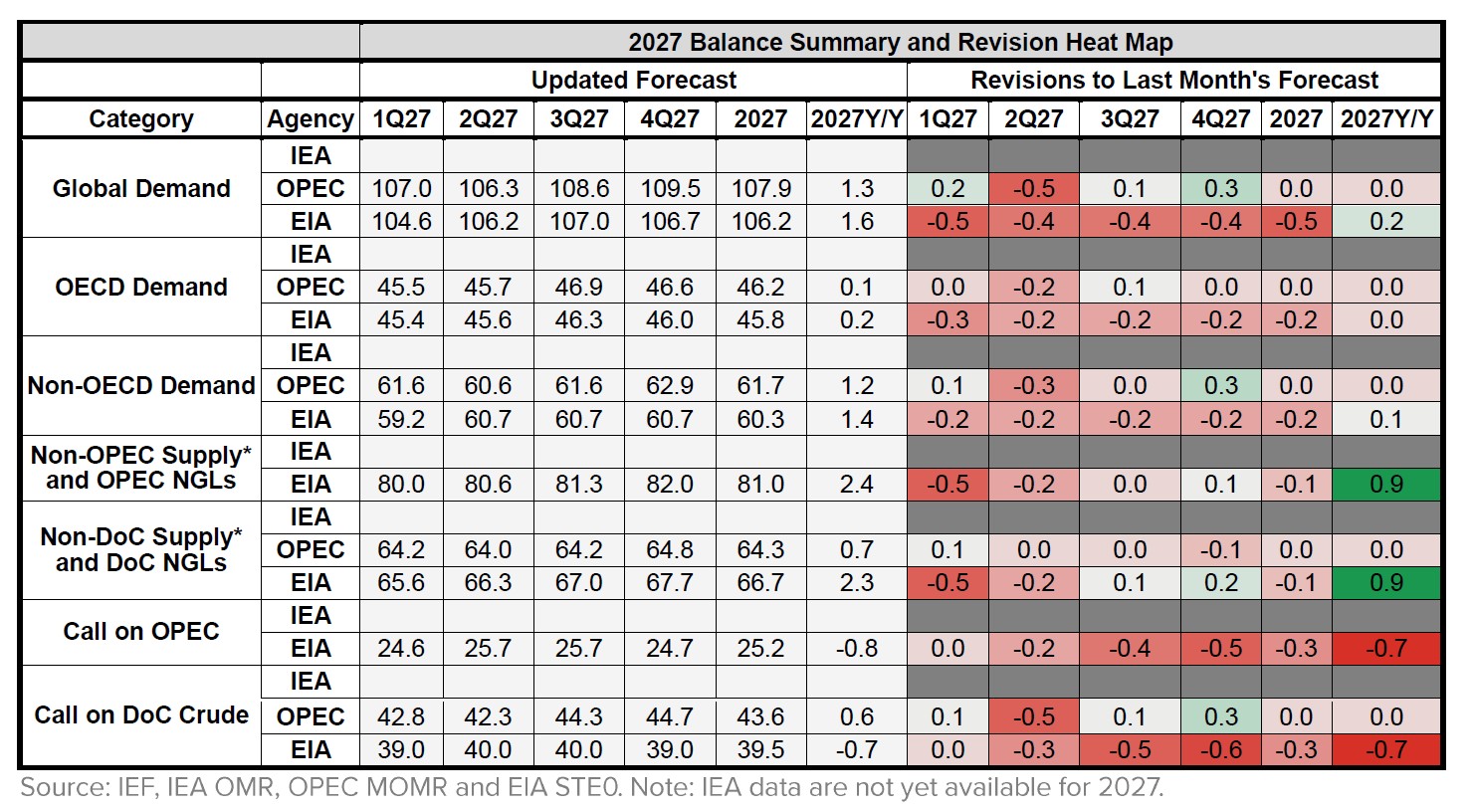

2027 Outlook Comparison

Agencies project a strengthening in global oil demand growth in 2027, with the EIA estimating year-on-year growth of around 1.6 mb/d, compared to about 1.3 mb/d in OPEC’s outlook. Growth remains largely driven by non-OECD economies. Despite the stronger growth in the EIA projection, its average demand level remains more than 1 mb/d below OPEC’s estimate.

Regional projections indicate that China and India remain key contributors to demand growth. The EIA projects increase of around 0.2 mb/d in China and 0.3 mb/d in India. OPEC’s estimates are broadly aligned for China, while slightly lower for India at around 0.2 mb/d. Africa also contributes to growth, with the EIA projecting an increase of about 0.2 mb/d, compared with around 0.16 mb/d in OPEC’s outlook.