")

Comparative Analysis of Monthly Reports on the Oil Market

Thursday 14 May 2026

Summary

The outlook for global liquid fuel supply and demand remains subject to growing uncertainty, shaped by the closure of the Strait of Hormuz, and varying policy response and market conditions across regions. In this month's assessments, projections for 2026 global oil demand growth diverge across agencies by approximately 1.6 mb/d year-on-year.

Demand

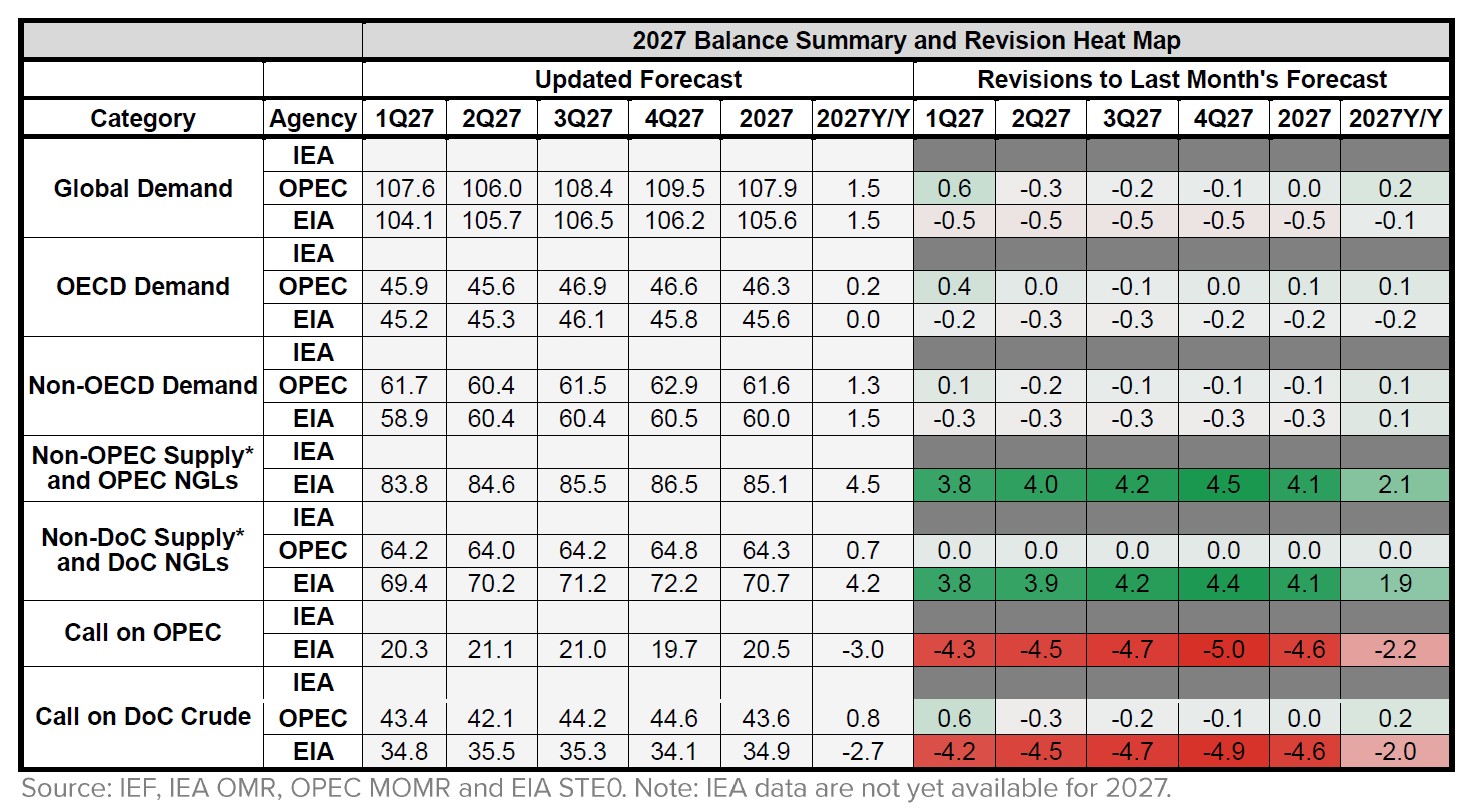

OPEC: OPEC expects global oil demand to grow by ~1.2 mb/d year-on-year in 2026, comprising growth of ~0.1 mb/d in OECD economies and ~1.1 mb/d in non-OECD economies. For 2027, OPEC sees demand growth of ~1.5 mb/d year-on-year, representing an upward revision of ~0.2 mb/d from last month's assessment. This is driven by growth of ~0.2 mb/d in OECD economies and ~1.3 mb/d in non-OECD economies.

EIA: EIA lowers its estimate of global oil demand growth in 2026 to ~0.2 mb/d year-on-year, down from 0.6 mb/d in the previous month and 1.2 mb/d in February. The downward revision primarily reflects weaker expected demand growth across Asia. The EIA projects OECD demand to contract by ~0.3 mb/d, while non-OECD demand rises by ~0.5 mb/d. For 2027, the EIA projects a rebound in demand growth to ~1.5 mb/d, lifting global oil demand to ~105.6 mb/d.

IEA: IEA revises its 2026 global oil demand growth estimate further downward to a contraction of ~0.4 mb/d year-on-year, around 0.3 mb/d lower than the previous month's projection. The IEA sees the petrochemical and aviation sectors as the most immediately expo sed, but continued volatility in energy prices, lower economic activity, and declining purchasing power are expected to increasingly constrain fuel consumption across sectors. The agency projects non-OECD demand to contract by ~0.1 mb/d year-on-year, while OECD demand declines by ~0.3 mb/d.

Supply

OPEC: OPEC maintains its estimate of non-DoC liquids supply and DoC NGLs growth at ~0.8 mb/d in 2026, unchanged from last month's assessment, bringing total supply to ~63.6 mb/d. Growth is led by the United States, Canada, Brazil, and Argentina. This expansion is expected to continue into 2027, with supply rising by a further ~0.7 mb/d, also unchanged from the previous month's estimate, reaching ~64.3 mb/d, supported by additional growth from Qatar, Canada, Brazil, and Argentina.

EIA: EIA revises its estimate of non-DoC supply and DoC NGLs growth sharply downward to a contraction of ~0.9 mb/d year-on-year in 2026, compared with growth of ~0.3 mb/d in last month's assessment. For 2027, the EIA projects a stronger recovery of ~4.2 mb/d, marking an upward revision of ~1.9 mb/d. The agency raises its outlook for US crude oil production by ~0.1 mb/d to ~13.6 mb/d in 2026, and by ~0.3 mb/d to ~14.1 mb/d in 2027 relative to the previous month's estimate.

IEA: IEA revises its estimate of non-DoC supply and DoC NGLs growth to broadly flat year-on-year in 2026, representing a downward adjustment of ~0.3 mb/d from last month's assessment, with output reaching ~63.2 mb/d. The IEA also projects global oil supply to d ecline by ~1.8 mb/d to ~95.1 mb/d in April 2026, while average global supply is expected to reach ~102.2 mb/d over the year .

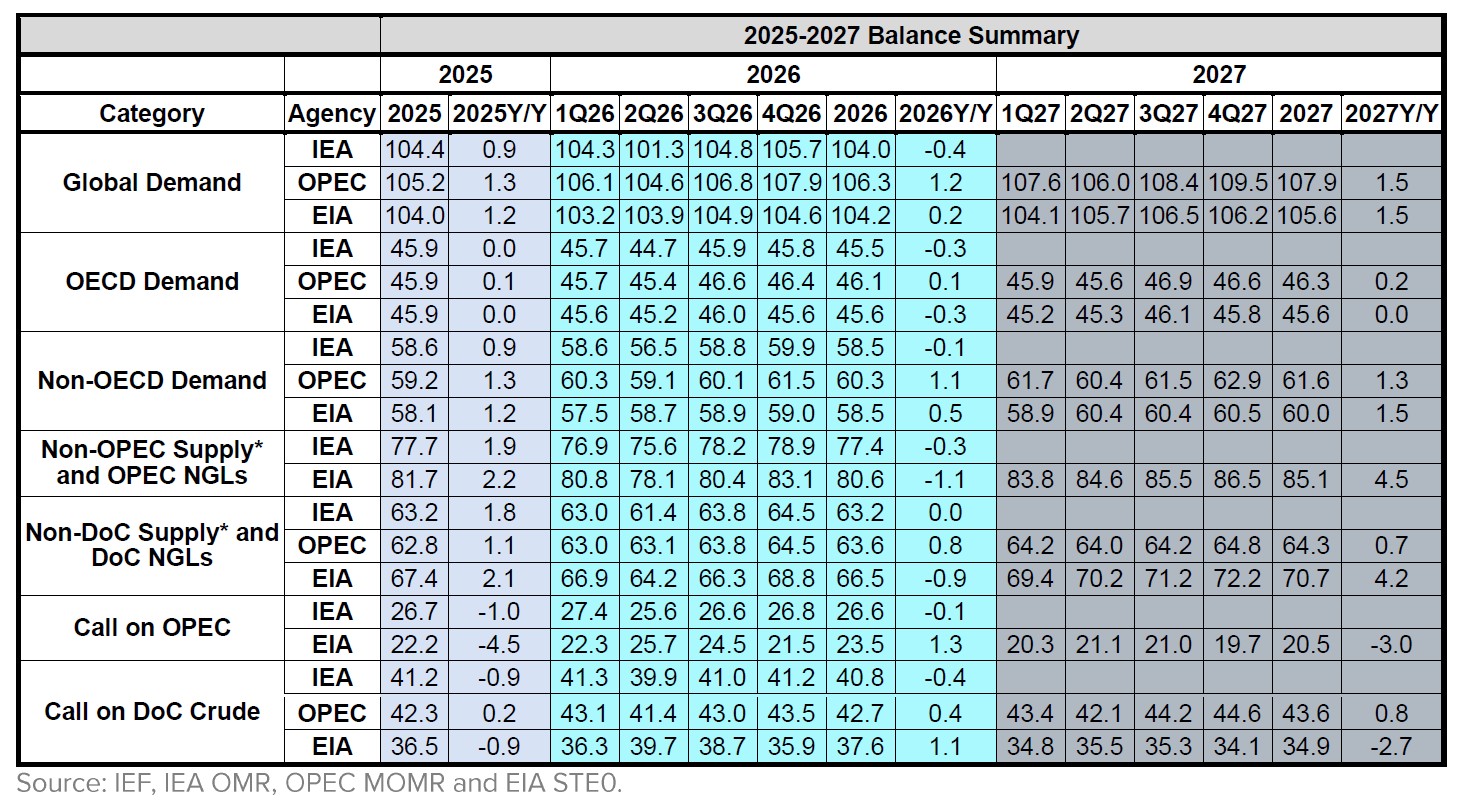

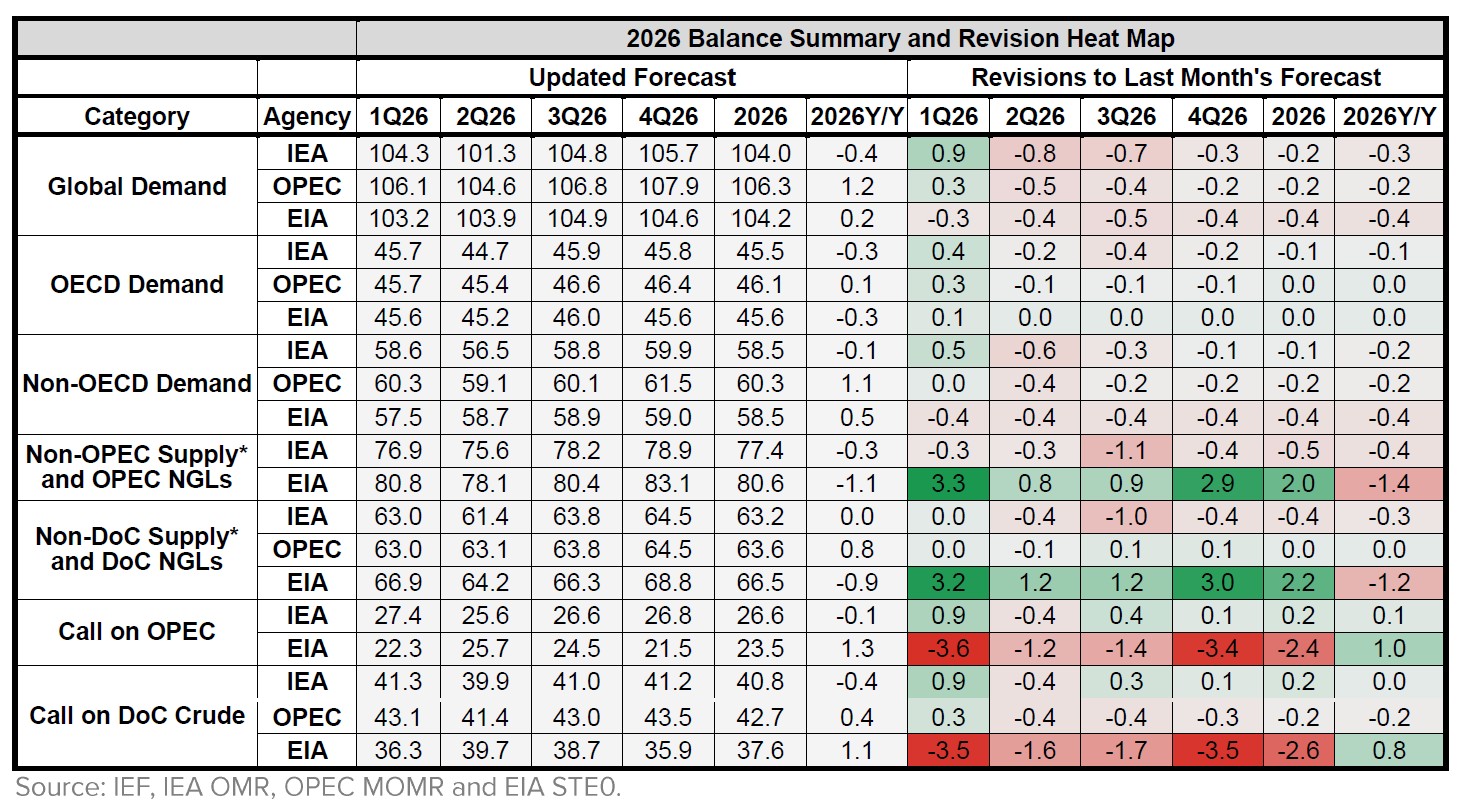

2025-2027 Balance Summary

In 2026, global oil demand projections continue to show notable divergence, with OPEC forecasting demand at ~106.3 mb/d, above estimates from the EIA at ~104.2 mb/d and the IEA at ~104.0 mb/d. By 2027, OPEC continues to project the highest demand level at ~107.9 mb/d, while the EIA places demand at ~105.6 mb/d. On the supply side, the IEA projects non-OPEC supply and OPEC NGLs to contract by ~0.3 mb/d year-on-year, compared with ~1.1 mb/d in the EIA's assessment.

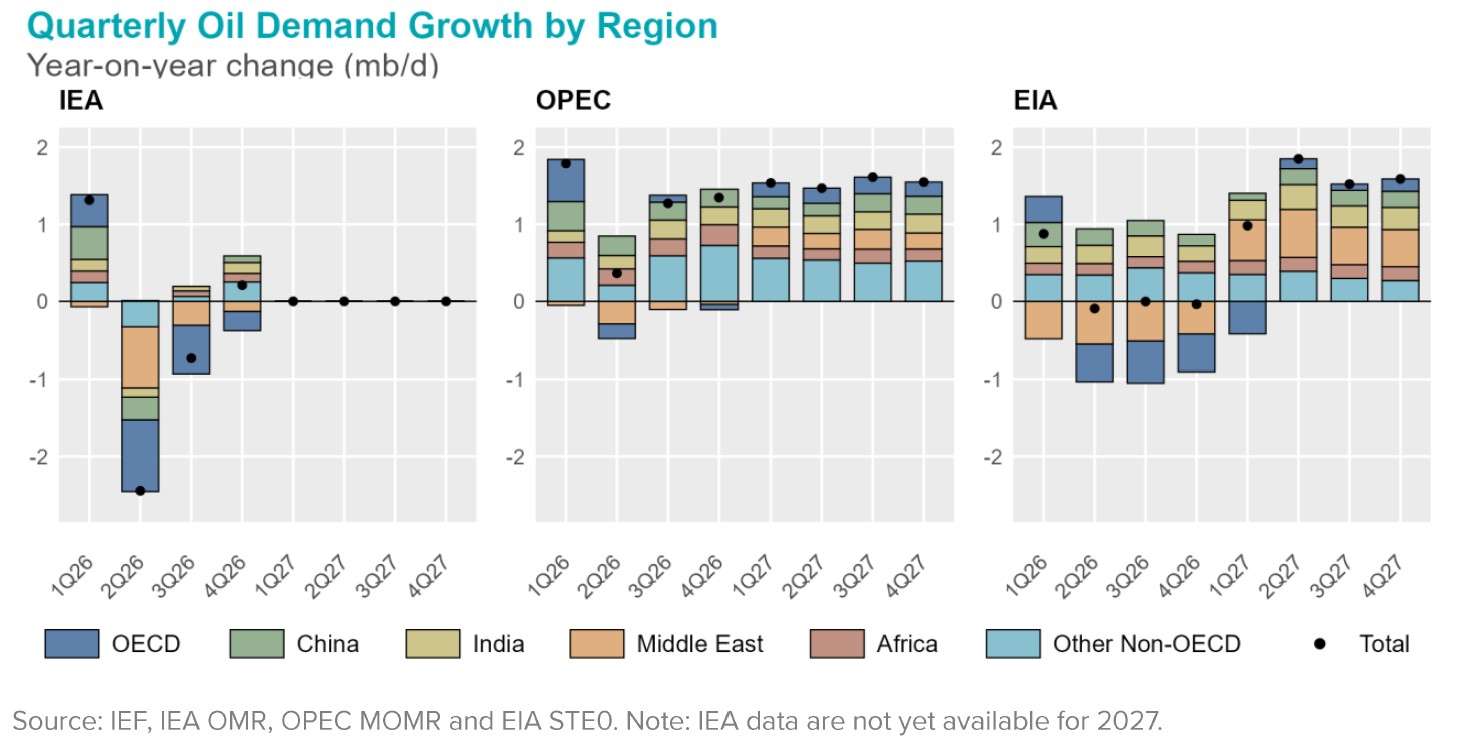

The IEA projects a marked decline in oil demand across all regions in 2Q26, with demand falling by ~2.45 mb/d. This widens the gap with OPEC to ~3 mb/d during the quarter. By 2027, both the EIA and OPEC project average demand growth of ~1.5 mb/d, despite modest differences in quarterly profiles.

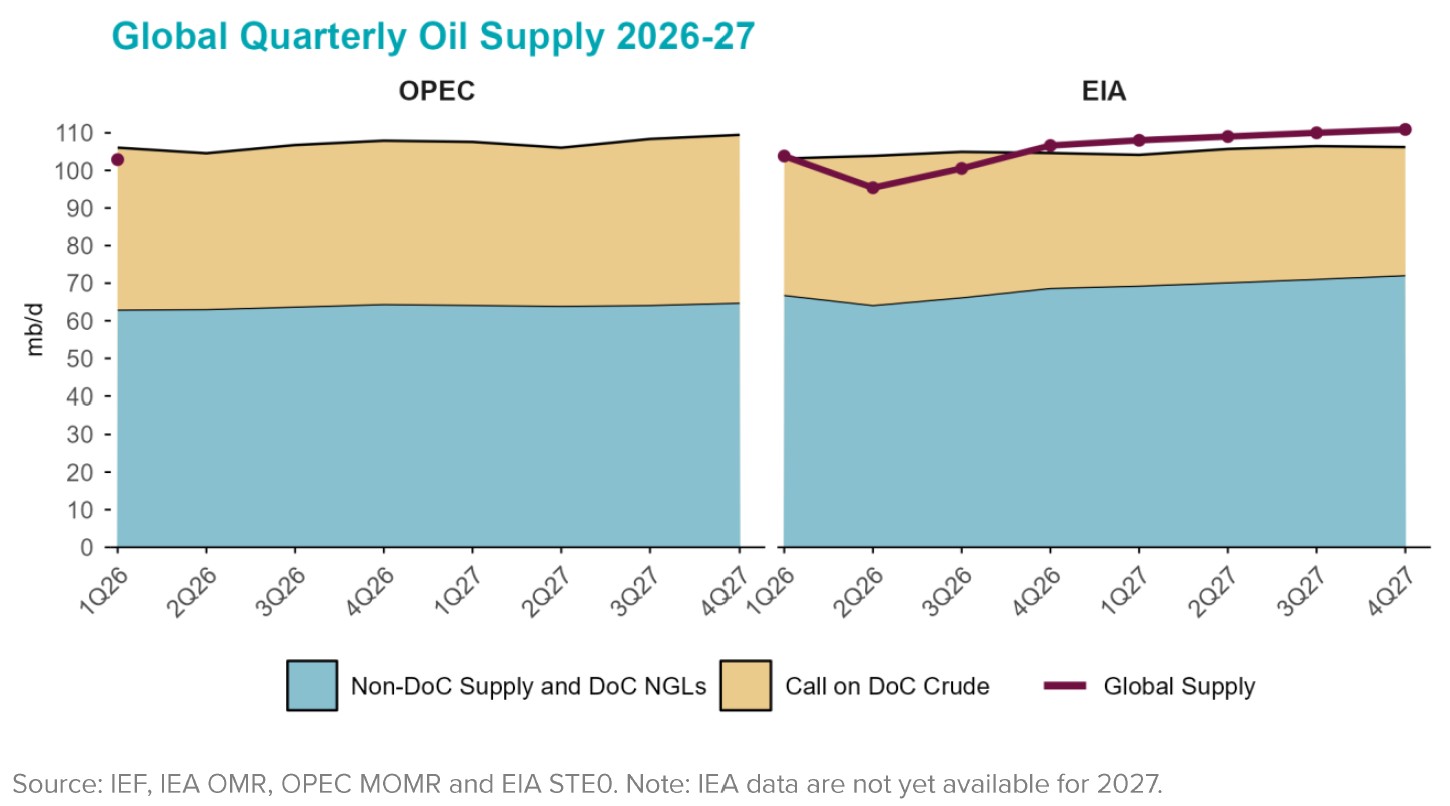

In the first quarter of 2026, the EIA projects non-DoC supply and DoC NGLs at ~66.9 mb/d, around ~3.9 mb/d above OPEC's estimate of ~63.0 mb/d. This divergence persists through subsequent quarters, with the EIA consistently projecting higher non-DoC supply levels, reaching ~72.2 mb/d in 4Q27 compared with OPEC's ~64.8 mb/d.

2026 Outlook Comparison

Global oil demand projections for 2026 continue to diverge across major forecasting agencies, with the spread in demand growth estimates reaching ~1.6 mb/d year-on-year. In this month's assessments, all three agencies revise their demand outlooks downward relative to the previous month, with adjustments ranging from ~0.2 to ~0.4 mb/d year-on-year.

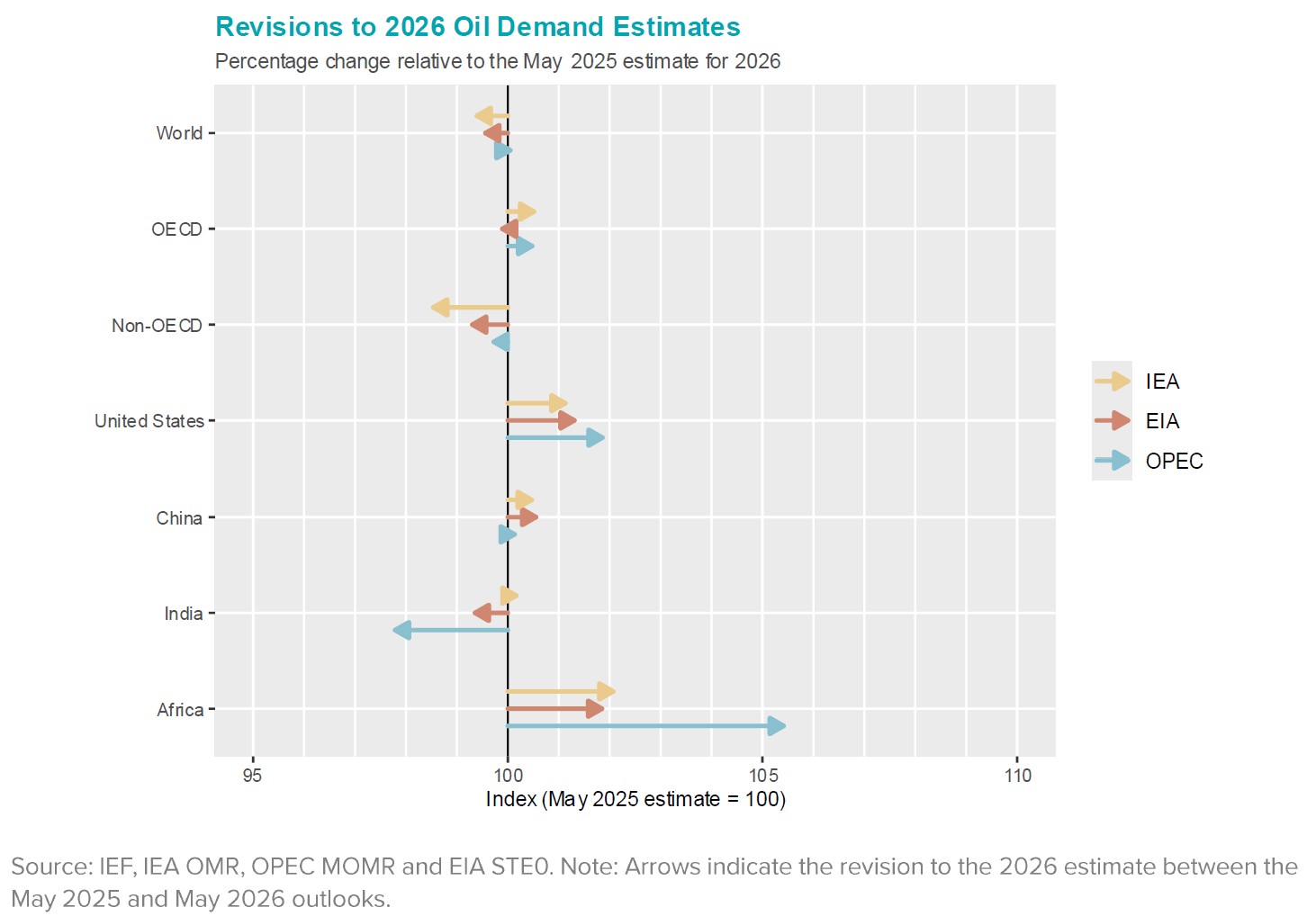

Recent adjustments to 2026 oil demand estimates remain modest at the global level, with all three agencies maintaining their world demand projections broadly in line with the May 2025 baseline. Revisions across the OECD are also modest, with IEA and OPEC showing slight upward adjustments, while EIA remains broadly unchanged. In contrast, non-OECD demand is revised downward across all agencies, with the IEA showing the largest reduction. More visible changes emerge at the regional level. Africa records the strongest upward revisions, led by OPEC, which raises its outlook by more than 5% relative to the May 2025 baseline, followed by more moderate increases from the IEA and EIA. The United States is also revised upward across all three outlooks, with the largest increase in OPEC's assessment. India shows the clearest divergence, with the IEA maintaining a near-baseline outlook, the EIA revising demand slightly downward, and OPEC making a more visible downward adjustment.

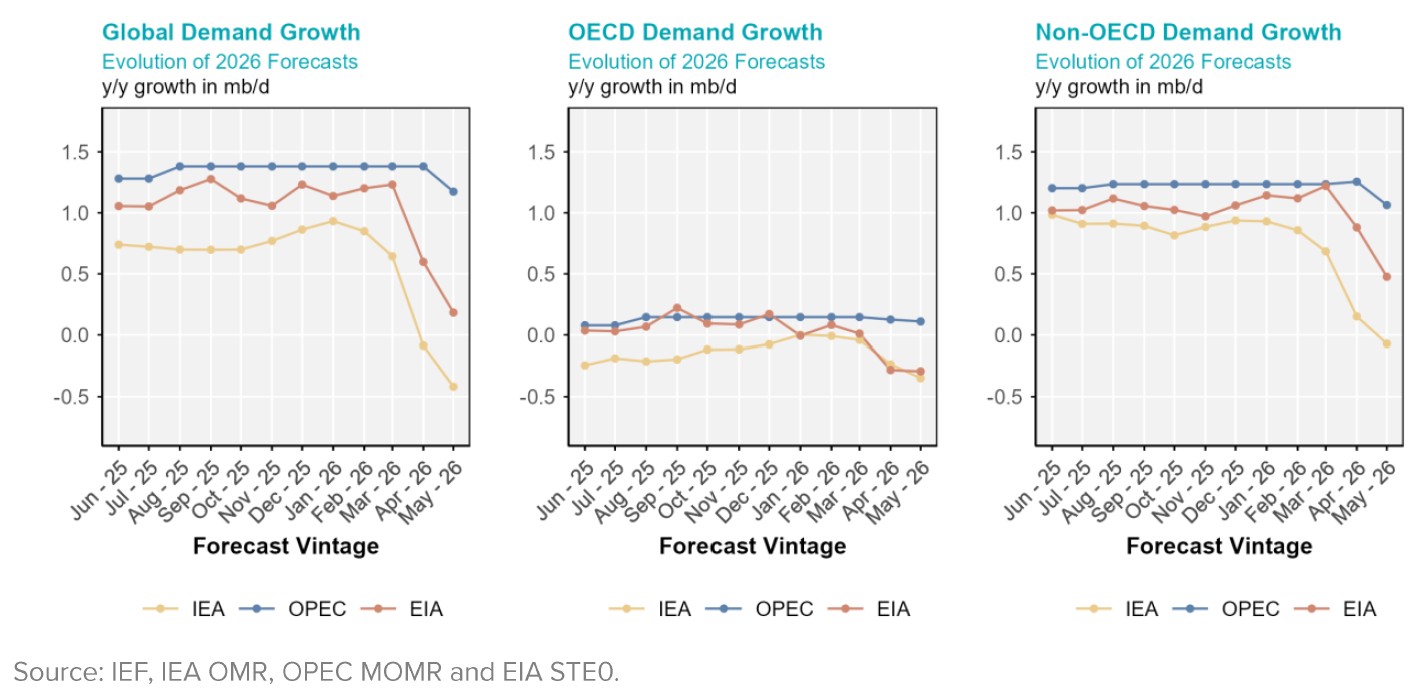

Evolution of 2026 Annual Demand Growth Forecasts

Global oil demand growth projections across agencies show a spread of ~1.6 mb/d, with much of the divergence driven by differences in non-OECD demand estimates. EIA and IEA show relatively close alignment in their OECD demand projections, although both remain around ~0.4 mb/d below OPEC's estimates.

OECD oil demand projections differ across agencies in 2026, with the EIA and IEA projecting declines of ~0.3 mb/d and ~0.35 mb/d, respectively, while OPEC projects modest growth of ~0.1 mb/d. Non-OECD demand presents a more positive outlook, with OPEC projecting growth of ~1.1 mb/d and the EIA estimating an increase of ~0.48 mb/d, while the IEA projecting a slight decline of ~0.1 mb/d. In China and India, all three agencies project demand growth, with both the EIA and OPEC forecasting increases of more than ~0.2 mb/d in each country in 2026.

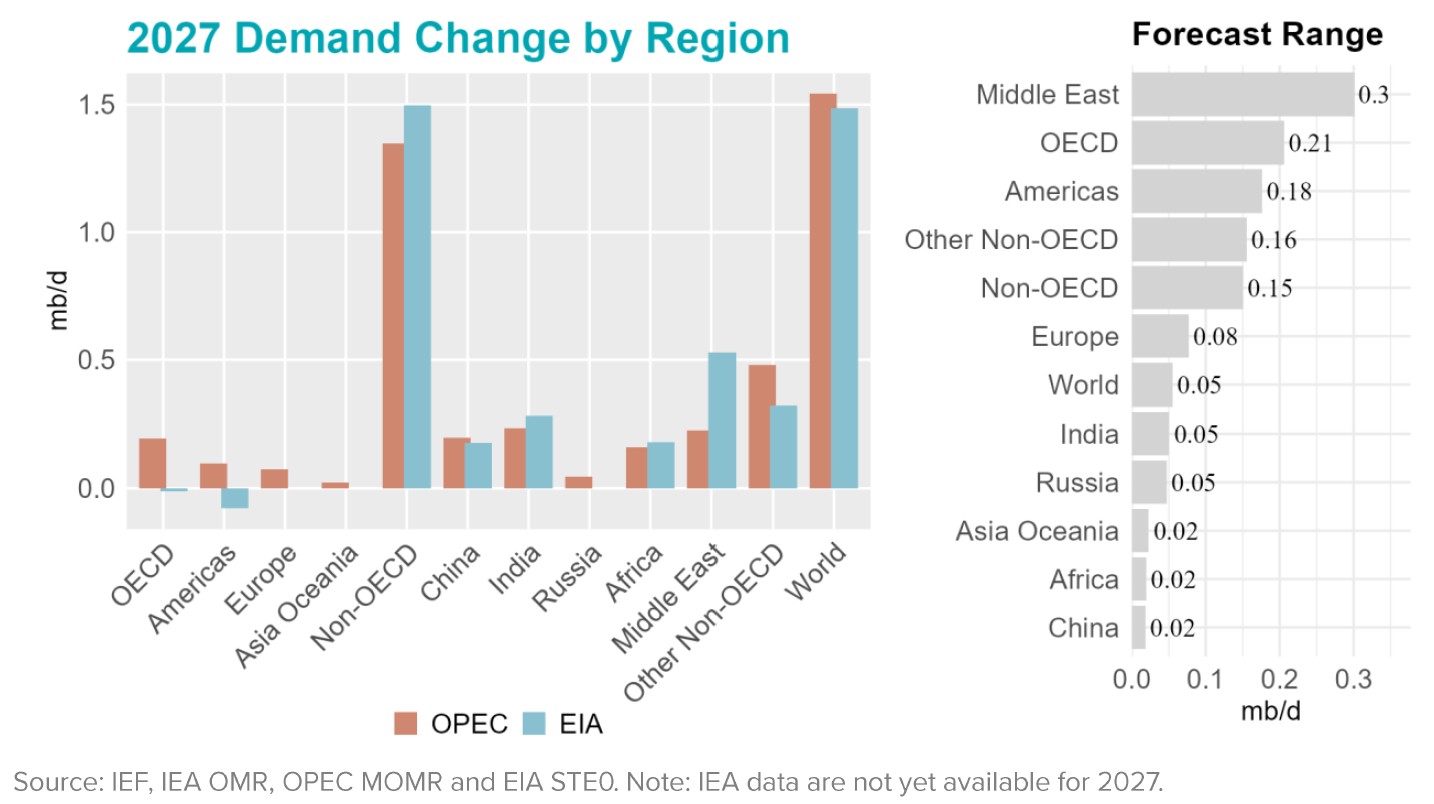

2027 Outlook Comparison

In 2027, following a downward revision of ~0.1 mb/d in the EIA demand outlook and an upward revision of ~0.2 mb/d in OPEC's estimate relative to last month's assessment, both agencies now show close alignment in their 2027 global oil demand projections. Each forecasts a rebound in global demand growth of ~1.5 mb/d year-on-year.

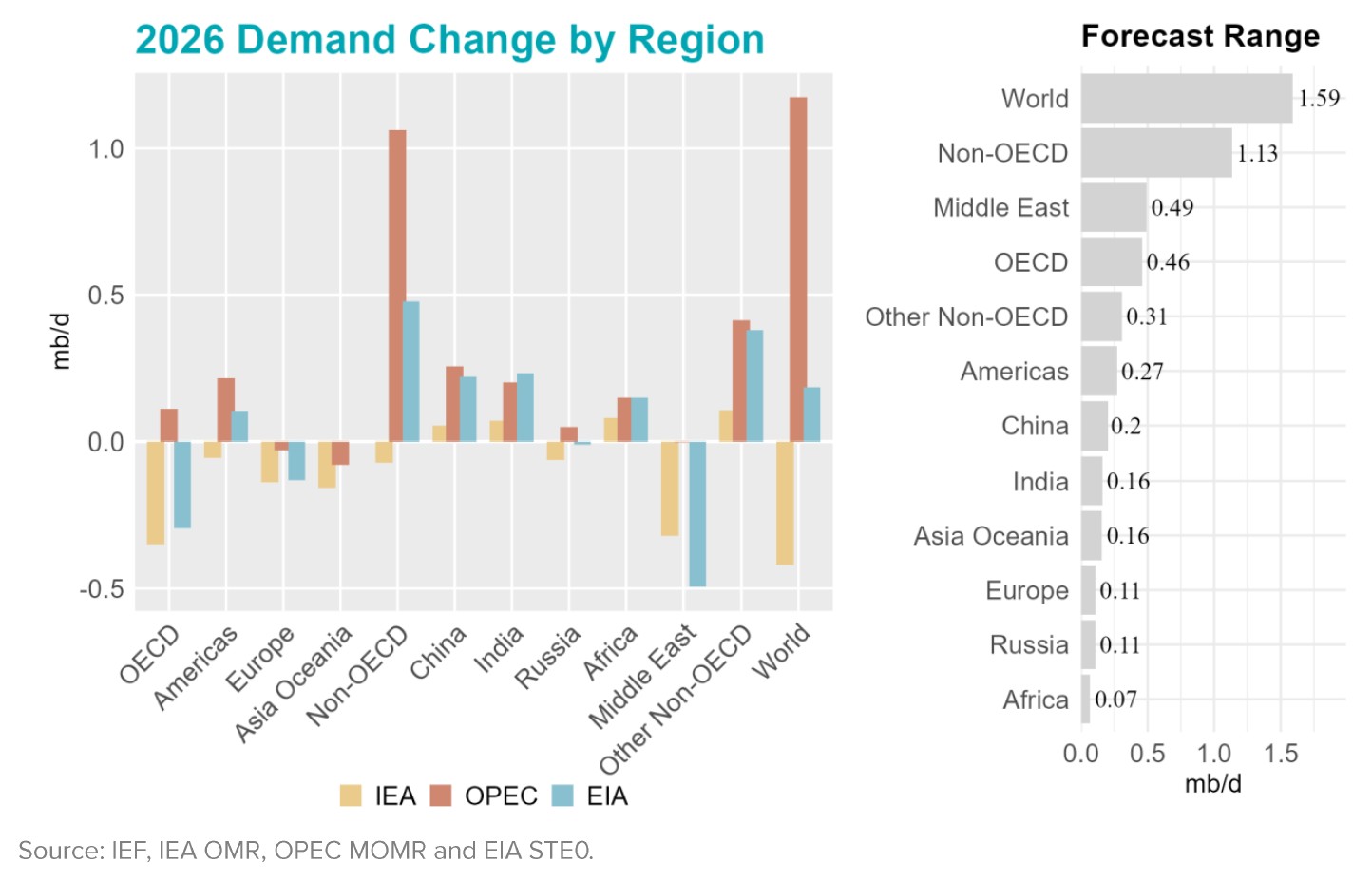

Regional demand projections continue to highlight China and India as major contributors to global oil demand growth in 2027. India leads demand growth, with the EIA forecasting an increase of ~0.3 mb/d and OPEC estimating ~0.24 mb/d. In China, the EIA and OPEC project demand growth of ~0.18 mb/d and ~0.2 mb/d, respectively. Across Africa, both agencies project more moderate growth, with the EIA at ~0.18 mb/d and OPEC at ~0.16 mb/d. In contrast, OECD demand remains relatively flat, with the EIA projecting broadly unchanged demand, while OPEC anticipates modest growth of ~0.2 mb/d.